The future of digital advertising might just revolve around the matter of trust. But before publishers take on that question, they should consider this one: Why is Big Tech working so hard to build trust in their respective walled gardens?

Take Amazon (please!). They’re rumored to be creating a universal identifier restricted to their ecosystem. Google’s proposed FLoC targeting, presented as the evolution of 3rd party cookies, might be reimagined before it even launches over privacy concerns. But surely whatever takes its place will only serve to strengthen its monopolistic hold on advertising. Apple is pushing to present their core OS’s as privacy-focused — all while maintaining their typical “advantageous” relationships with the app developers that build and support large parts of their ecosystem. All are effectively fortifying the garden walls while working to convince the public of their respective trustworthiness.

This new-found obsession should come as no surprise to publishers: Trust is a key ingredient in the secret sauce of ad revenue growth.

Anecdotally, we know this to be true, and the numbers don’t lie. Privacy is the #1 driver of influence and engagement on social media platforms. Brands and agencies are cutting advertising budgets due to trust issues: Of those who decreased ad spend on one or more major ad platforms, 35% cited concerns over ethical handling of user data.

A shining opportunity for publishers

In a new trust-based world of content and advertising, publishers start with a few crucial advantages.

First, publishers enjoy implicit goodwill from their audiences, which converts to business. More than two-thirds of consumers are more likely to engage with an ad in the context of a publisher they know and trust. Second, publishers have the advantage of knowing the types of content readers want to engage with. Most notably, publishers own the new “oil” of advertising: 1st party data.

What is the opportunity for publishers? It’s a chance to differentiate themselves from Big Tech as the embodiment of stewardship with regards to consumer data. In short, publishers must buck the status quo and adopt a strategy where the audience is no longer for sale. Sell the site and sell the content. Maybe even leverage audiences on the backend to improve content experiences or implement new rate types. But no matter what, protect audience’s trust in publishers audiences by implementing a privacy-first approach.

Capitalize with balance and control

Successfully seizing this opportunity will take balance and control.

Balance subscription and ad-supported strategy.

A paywall that is too high limits exposure and hamstrings new audience gains. However, too much advertising hurts a brand’s value and, most of all, the audience’s trust (that they won’t be constantly blasted with ads).

Control the quality of the user experience

Ad clutter diminishes trust by reneging on the promise of a good user experience. But control also means an increased cognizance of demand sources. Due to its inherent reliance on 3rd party cookies, programmatic demand should be a last resort. And these demand sources should provide the tools necessary to preserve brand-safe environments.

Trust is the answer (and the question)

How does the industry enable publishers to build and maintain trust? The simplest solution may be to step aside and let publishers create quality content. The role of industry tech platforms, in turn, is to support publishers without adding complexity. All the while, brand safety is table stakes: Any digital distributor should guarantee it (full stop).

Of course, tech platforms must enable publishers to meet their business objectives. They should support multiple pricing models and offer broad customization options for demand sources. Again, this is because publishers know best in a new world of 1st party data and heightened demand for sophisticated content. (Read: the opposite of standard display).

The guiding principle? Trust. The differentiator from Big Tech? Trust. Our final thought? Trust us on this one.

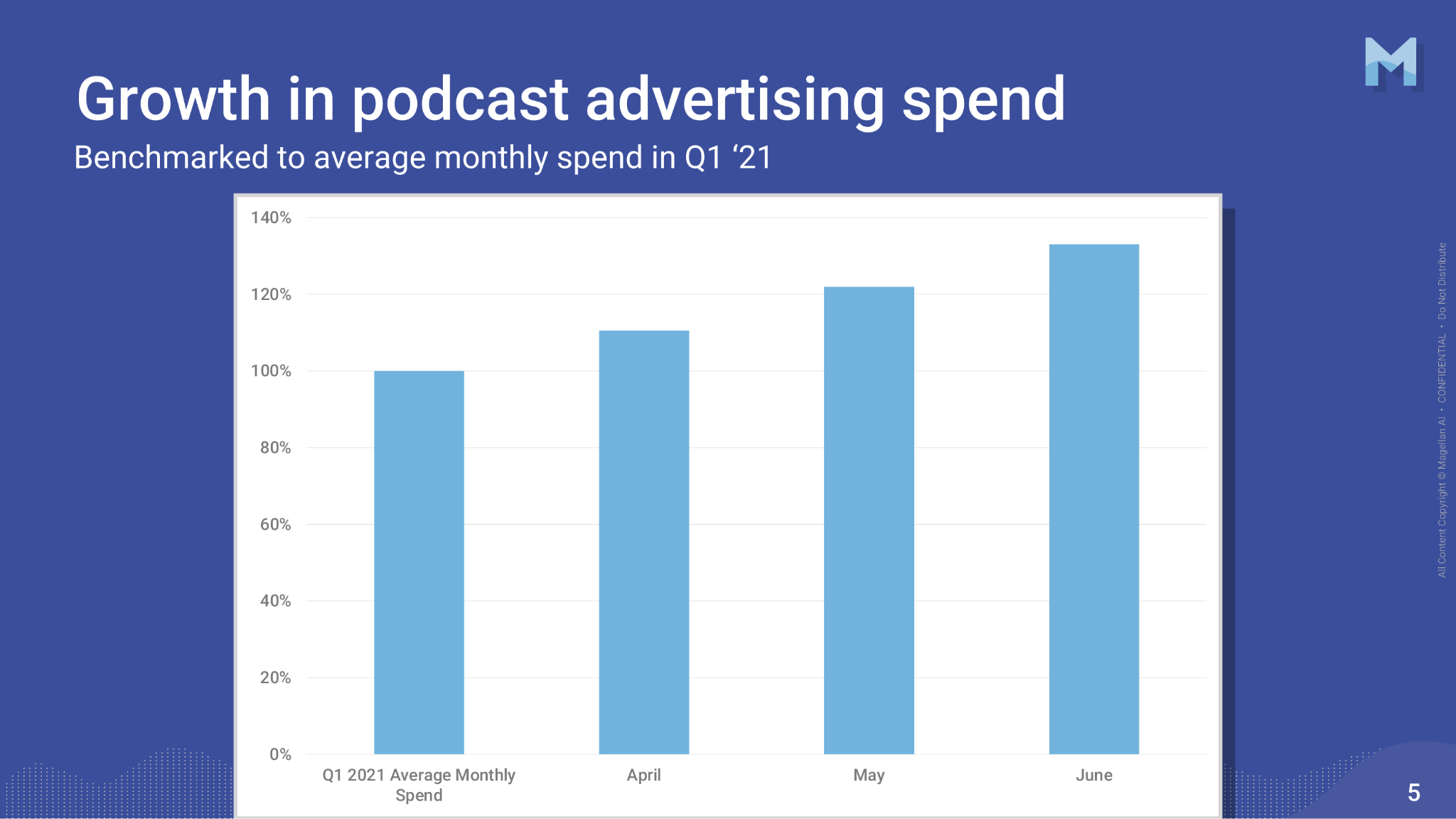

Although the pandemic has revolutionized many of our media consumption habits over the past 18 months, one thing has become increasingly clear: podcasts are not going anywhere. Even as new work-from-home regimes supplanted daily commutes at the height of the pandemic, audio programming continued to find its way into the ears of its consumers.

According to The Infinite Dial, an annual report released by Edison Research and Triton Digital earlier this year, over eighty million Americans ages 12 and up (roughly 28% of the U.S. population) are weekly podcast listeners. That’s a 17% increase in listenership, which is sizable compared to the 9% increase recorded from 2019 to 2020.

Source: Edison Research/Triton Digital

“Let me be the first to admit — the increase from 24% to 28% year-over-year did surprise me,” said Tom Webster, SVP of Edison Research and co-author of the report. “In a year in which absolutely nothing was normal, podcasting grew even more than it had the year before.”

Once society enters a truly post-pandemic era, Edison Research’s Webster is confident that listenership will remain loyal, particularly with the resurgence of the daily commute. “Habits are habits. And when people go back to the office, we’re going to see a lot of these habits stick.”

A formidable playing field for ad spending

Advertisers are banking on this habit retention and focused audience attention. The podcast advertising market continues to rise steadily, quarter after quarter. By next year, the global podcasting industry is anticipated to reach $1.6 billion.

Source: Magellan AI

While leading podcast providers like Spotify have reported less users than they projected for the second quarter of 2021, their advertising sales are up 110% from last year. Congruently, their ad revenue has jumped from 10% to 12% in the past 12 months.

“It’s clear to me that the days of our ad business accounting for less than 10% of our total revenue are behind us. I expect ads to grow to be a substantial part of our revenue mix,” Spotify CEO Dan Ek told investors in a conference call last month.

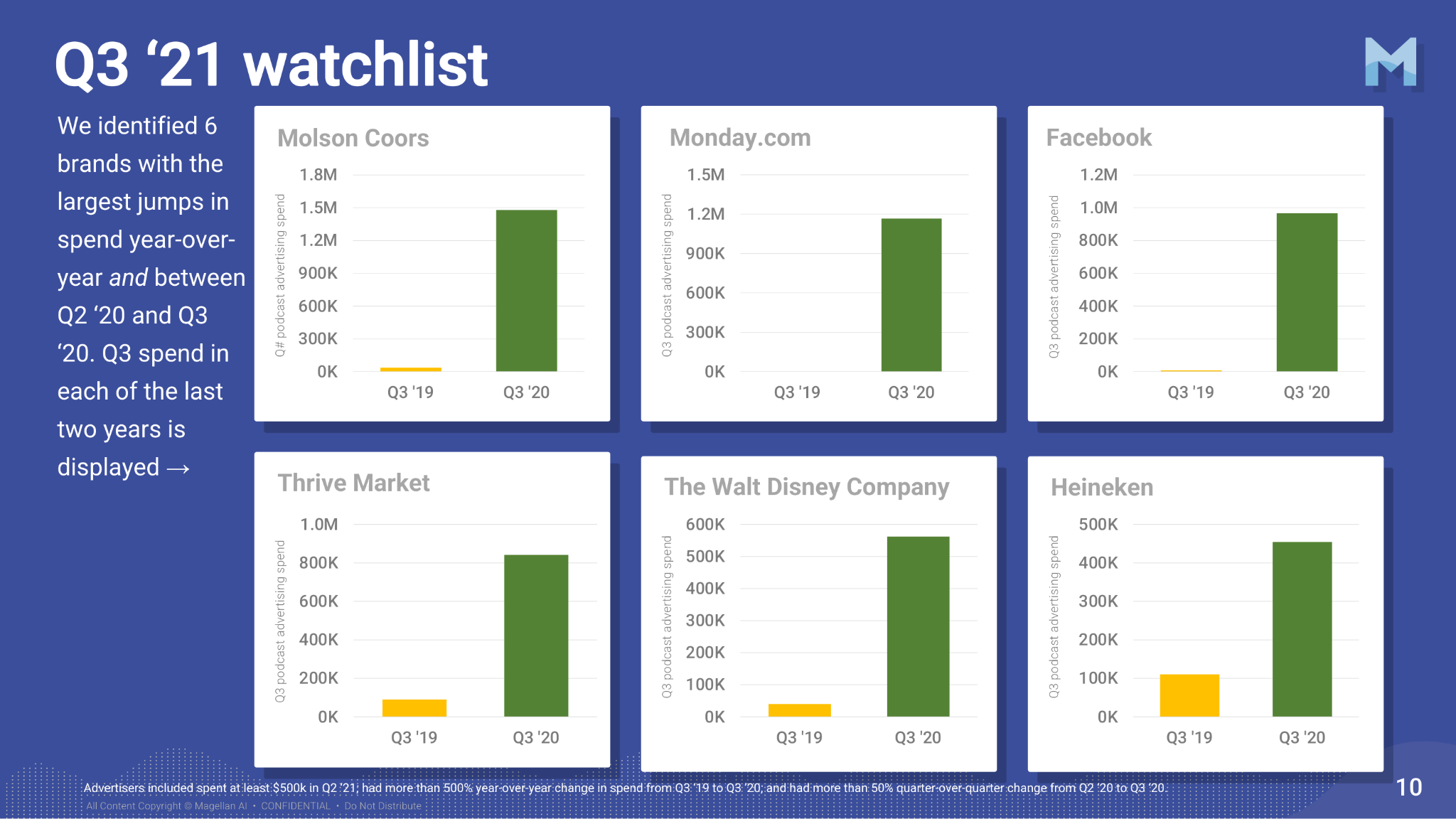

According to research conducted by Magellan AI, podcast spending in the second quarter of 2021 rose by a sizable 22% from the first quarter of this year, a 40% increase year-after-year. It’s worth noting that, according to Magellan AI, sports podcasts added the most new advertisers in Q2 than any other genre.

Source: Magellan AI

Impactful advertising

Which brands packed the biggest ad-spend punch? For longtime podcast listeners, direct-to-consumer brands like HelloFresh, Casper Mattresses, or BetterHelp may come to mind. Although, in recent months, larger corporations have risen to the top of the list of biggest ad spenders.

What makes the podcasts so valuable to advertisers, especially the behemoth brands that seemed to have gone “all in” on podcast advertising in recent months? (In particular, what’s in it for those like Amazon or Geico, which seemingly have no lack of demand for their products/services?)

“When you look at that [podcasting] audience, that audience is typically more affluent, more educated, has a higher disposable income. So, it’s very attractive to advertisers,” according to Damian Radcliffe, digital media analyst and professor of Journalism at the University of Oregon. “The other big factor here is that podcast advertising tends to be pretty limited & there’s a value in that exclusivity for podcasters which is quite appealing.”

Source: MagellanAI

A season of exclusive brand extensions

As the podcast industry continues to rise in listenership and sponsorship, we can also expect a growing wave of corporate partnerships and exclusive podcasting networks. This month, HBO Max and WWE both announced they would be launching exclusive podcast programming for their subscribers.

HBO Max will be producing a number of ad-free podcasts as in-app exclusives to subscribers, beginning with “Batman: The Audio Adventures,” a scripted series featuring the voices of A-list actors Jeffrey Wright and Rosario Dawson. HBO already has over 25 network-specific podcasts that expound upon its programming including “The Chernobyl Podcast” and “Allen vs. Farrow.” However, “Batman: The Audio Adventures” will be the first audio program exclusively available to HBO Max subscribers beginning this fall.

WWE has teamed up with The Ringer, a subsidiary of Spotify, to create an exclusive audio network specific to wrestling-related content, in what will be a multi-year audio content partnership

“I think this is a model we’re going to start to see also in the podcasting space,” explained Radcliffe. “Instead of this content being available and distributed via an RSS feed to any number of podcast platforms it’s going to be locked in, behind a paywall. The only way [listeners] are going to be able to access it is by taking a subscription to that platform.” Radcliffe also points to an interesting development that’s emerged over the last couple of months, the ability to subscribe to specific shows with a paid relationship.

As media Goliaths and corporations continue to expand their purview to the podcasting sphere, brands across every industry are finding ways to appeal to even the most obscure of consumer niches. Considering that some podcasts have as much listenership as prime-time television viewership, there is no lack of ‘big fish’ in the podcasting pond. All advertisers need to do is find ways to reel them in.

Best practices for embracing the ‘podvertising’ future

Focus on presenter reads

The Super Listeners 2020 study from Edison Research found that 48% of respondents reported paying greater attention to podcast ads than any other form of media advertising. A big reason for this is due to presenter reads.

“If you look at things like presenter reads as a format…It is seen as a very effective way to reach an audience because it feels more integrated into the show, a more seamless part of the content,” explained Radcliffe. “It doesn’t feel as intrusive as ads coming in the same way as pop-ups, banner ads online, or TV advertising.” Radcliffe added that when it comes to presenter-read advertisement, tone matters. If advertisement copy is read casually and informally, it has a tendency to be less obtrusive to listeners.

Select podcasts that make sense for your brand

According to Radcliffe, “As [podcast advertising] continues to grow and as we see more specialized content being offered, that creates more opportunities for targeted advertising.” Although, Radcliffe was quick to emphasize an overlap in listeners and brands’ target consumers. “There has to be a cultural fit there. A fit in terms of style and content.”

Benchmark ROI with listener discount codes

If you’ve ever listened to a podcast, you may have heard advertisements that provide discount codes to listeners of the show. Not only do these discounts incentivize potential consumers, they are “quite a quick way to get a benchmark of ‘Is this advertising working? Am I actually converting listeners into consumers of my product?’ which matters a lot to advertisers,” said Radcliffe, adding, “They know exactly where that consumer has then come from.”

For larger brands, small conversion rates can still be valuable

“Because the reach of a lot of these shows is large, brands don’t need a large percentage of conversion,” Radcliffe articulated. “Their equivalent ‘open’ rate could be small but because brands have got scale in terms of that audience reach. That could still be very valuable for them.”

How many publishers do you have a paid subscription with? While you may be a paid subscriber with one or two digital publishers, you remain a “never-subscriber” from the lens of the next publisher. The 2021 Reuters Digital News Report states that the majority of people pay for one subscription (for content from publishers and local papers), and that the median number of subscriptions for U.S. consumers is two.

To digital publishers, never-subscribers mean lost revenue. But in today’s digital-first world, where ad revenues are unreliable and subscription fatigue is mounting, should never-subscribers remain a lost revenue opportunity? The answer lies in implementing dynamic paywalls.

A typical dynamic paywall journey looks like this: Place a first-party cookie so you can track user visits. Then, give the visitor access to a few pieces of metered content. After a set number of articles, it’s time to show a registration wall. Then, as soon as those views are up, it’s time to show the “all you can eat” subscription paywall/offer.

Many users traverse this journey but for those that don’t subscribe, publishers tend to “rinse and repeat” the same journey. Some publishers might try discount offers for “all you can eat” subscriptions or even suggest custom-bundles at lower price points before allocating dead end users to the “rinse and repeat” pool.

Untapped revenue opportunities

Despite visit recency and frequency metrics, there are users who defy registration, subscription, or custom-bundle offers even after relentless efforts by the publishers. These dead-end users are your never-subscribers. And there are hoards of them. There are also those users who churn after the subscription trial period is over, or sleepers who churn at the beginning of the month when they evaluate their credit card bills. All of these users offer an untapped revenue opportunity.

Putting never-subscribers (dead end users and churned users) back in the “rinse and repeat” bucket is hardly a strategy. However, there are a few questions that needs answers before a real strategy for never-subscribers can evolve:

Who are the dead end users?

What are the additional options available beyond discounting or custom-bundles?

If users were given additional options, would fewer users subscribe?

If users were given additional options, would there be fewer sleepers?

If users were given additional options, would it accelerate subscription churn?

Dead end users could be visitors with high visit frequency who subscribed elsewhere. They might be casual visitors referred via social media. Or perhaps they are low frequency visitors from international geographies. The mix differs for each publisher, but retrospective analysis of user journey data should yield quick segmentation of never-subscribers.

Extending the user journey with discounted subscriptions or custom-bundles are good options for users approaching a dead end. But how do you know how much discounting would suffice? Or what custom-bundle offers will work for the user?

Unbundling solutions

To get this understanding, publishers have to unbundle the existing content pool to evaluate the true worth of each piece of content. Extending to unbundling solutions such pay per content provide insights for custom-bundles. They also provide substantial revenue streams for the long term.

Understanding the direct impact of unbundling solutions on the publisher’s existing subscription business requires sustained experiments and aligned goals between departments. For example, subscriber numbers dominate reader-revenue headlines.

However, they fail to focus on subscriber retention or revenue. Marketing teams could be focusing on increasing pageviews without any consideration about the quality of the audience which converts into subscriptions. The editorial team on the other hand could be working in a silo without any revenue linked objectives.

Playing the long game to win

Improving audience engagement and customer-lifetime-value are high level goals that every department’s KPI should be linked to. For example, changing the KPI to net new subscribers and average revenue per subscriber are better health barometers of the reader-revenue business. New subscribers per-1,000 pageviews focuses the marketing team’s efforts on quality audiences. And, average time spent per page allows editorial teams to focus on quality content for their audience.

No publisher can escape the fact that subscriptions are a long game. The Google News Initiative reader revenue playbook carries an ominous message:

“For some of the [news] organizations we’ve worked with, the transition can take years if not decades. But it’s achievable. For many news organizations, converting just 3-5% of readers into paying subscribers or contributors can support long-term sustainability”.

Therefore, understanding never-subscribers and the monetization opportunities that lie within is a long game too! But why is it that publishers are ever so quick to dismiss the never-subscriber cohort and bring them back into the “rinse and repeat” pool for subscriptions? It turns out that extending the user journey with unbundling options might bear more fruit.

About the author

Abhishek is a Co-founder & CEO of Fewcents, fintech-for-publishers that brings incremental reader revenue from “Never-Subscribers.” He is a seasoned business leader and technology product manager. He has worked in management consulting with PwC and Altman Solon in Boston, USA before moving to Singapore permanently. In Singapore, he started his own venture, Shoffr, a digital marketing solution that provides online to offline attribution for digital marketers. In 2019, Abhishek sold Shoffr to Affle, a publicly listed ad-tech company in India. After solving the advertiser’s offline attribution problem, Abhishek has now set his eyes on solving the content monetization problem for online publishers.

Following years of growing adoption, Connected TV (CTV) consumption took center stage in the last year as consumers overwhelmingly shifted toward remote work. In fact, IAS research has shown that 90% of consumers have access to a CTV device. And 66% of them say their CTV consumption increased as a result of the pandemic.

Advertising dollars are also shifting in that direction, too. CTV ad spend for the U.S. is expected to grow nearly 50% in 2021, surpassing $13 Billion, according to eMarketer. And while there remain some hesitations about advertising on CTV, these environments are rich with opportunity.

New horizons create fresh starts and CTV is no exception. CTV environments connect advertisers with highly engaged audiences. They also put publishers, specifically CTV Channels, Virtual MVPDs, and Web/Mobile Publishers, in a strong position to facilitate those connections.

Let’s unpack that.

How publishers can make the most of CTV

Create exceptional ad experiences

From weekly releases to bingeable drops, and ad-free to ad-supported services, the streaming experience comes in various shapes and sizes. With more than 200+ streaming services to choose from globally, consumer attention is easily fragmented yet important to capture. Facilitating meaningful connections between advertisers and viewers starts by creating an exceptional ad experience.

And when it comes to CTV, consumers are already in favor. IAS research found that 90% of consumers think there are features of the CTV ad experience that make it better than linear TV.

Publishers should lean into consumer preferences by optimizing and maximizing the quality of the advertising experience. In particular, publishers should consider working with a partner that helps streamline the delivery process and provides the highest quality experience to the end user. Publica is a great example of one such partner by utilizing Server-Side Ad Insertion (SSAI) technology. SSAI stitches the ad into a single high-quality stream. This minimizes lag time and avoiding content disruption, which allows publishers to foster positive connections between consumers and brands while delivering a seamless streaming experience.

Leverage first party data

Publisher first party data has often been underutilized. When it comes to CTV, publishers have unique insight into what users are watching, when they’re watching, and how often. When leveraged in a privacy-compliant manner, this information is essential for effectively packaging and selling valuable CTV inventory.

Insight into consumer preferences and behaviors allows publishers to create audience segments and streamline the buying process for their advertisers. Additionally, publishers can work directly with advertisers to access advertiser first party data and match it to their own for increased accuracy.

Finally, publishers who work with third party partners with audience management capabilities and integrations, such as Publica, typically see increased yield by having deeper insight into buyer performance metrics and the ability to optimize as needed. This is a win for both viewers and advertisers. That’s because viewers are less likely to skip contextually relevant ads on CTV. IAS research found 42% of CTV users are likely or very likely to view an ad to completion if ads are contextually relevant.

Optimize for programmatic

CTV is still in the early stages of developing efficient optimization for programmatic inventory. This means there’s an opportunity to streamline the process as though it’s (almost) brand new. Working with a partner who can hold a unified auction can help drive efficiency, transparency, and optimization throughout the programmatic buying and delivery process.

Unified auctions allow publishers to offer inventory to multiple ad exchanges, removing the cumbersome need to integrate directly into an ad server and result in increased yield for publishers. Publica, for example, is built for scale and allows publishers to offer inventory to multiple sell side partners at the same time, via a single tag integration, and allows real-time bidding, opening up more demand.

Bottom line

In the last year, CTV has reached ubiquity in U.S. households. Not only do nearly 9 in 10 consumers have access to a CTV device, but most prefer the CTV ad experience to that of linear TV. With nearly 50% of workers planning to continue some remote work, it’s likely that CTV will continue to grow. And it will eventually usurp the role of family hearth once held by linear TV and radio before it. In the meantime, publishers have the rare opportunity to forge a new path and optimize for excellence.

Researchers continue to prove that ads viewed within a premium publisher environment drive greater advertising effectiveness. Each of the studies (here, here and here) offers insights and empirical data proving ad performance is better in premium content environments.

A new study to add to this notable library is the second phase of The Benchmark Series, the largest cross-media advertising effectiveness study conducted in Australia.

It’s important to note that the first phase of research showed that ads in premium environments offer 1.8 times better recall and 2.8 times the brand lift than short-form video on run of the internet. Further, ads in premium content also deliver 1.8 times higher recall than Facebook video. It appears that the brain processes ads differently depending on where an ad is seen. When people see ads in an environment that helps contributes to memory encoding, ad effectiveness is maximized. Premium editorial sites offer this context.

This new research supplies a unique perspective on advertising performance in premium long-form using Broadcast Video on Demand (BVOD). The VOD broadcasters’ included were 7Plus, 9Now, and 10 play. The study compares BVOD to YouTube, Facebook, and run-of-the-internet sites. It uses core ad effective measures likeability, brand recall and lift.

Both phases of the study were conducted by MediaScience, which is well-known for their expertise in neuro-measures (i.e. biometrics, facial expression analysis, eye tracking and EEG) methodologies. It included more than 5,350 participants and campaigns ran across 252 websites in Australia.

MediaScience defines premium content as:

Professionally produced content.

A media brand that people know and trust.

Brand safe environment.

Meaningful scale for advertisers.

Overall, the new research shows that ads that appear in BVOD are more effective and outperform video advertising across YouTube, regardless of whether the ads align with short or longer-form content.

Recall

Ads in BVOD environments are remembered better (1.3 times) than ads aligned to YouTube videos of any length. Further, when ads in BVOD are compared to YouTube videos shorter than 9 minutes, they generate 1.5 times greater unprompted recall.

Further, BVOD advertising delivers better unprompted recall (4.7 times) than Facebook video ads and 2.5 times better recall than run of internet short-form video.

Likeability

In terms of likeability, ads in BVOD generate 15% greater likeability compared to YouTube short-form. Dr. Duane Varan, CEO of MediaScience explains, “advertising in premium long-form video environments benefits from the content the ads sit alongside with premium content boosting their impact.” He adds, “The content is priming you for certain emotions and that benefits the ads that follow.”

The research shows that not all digital video environments are equal when it comes to advertising performance. Quality content environments matter when advertising and there’s plenty of research to support this statement. The reality is that it’s long overdue for advertisers to reevaluate where they place their ad dollars and their micro-targeted ad campaigns.

Mobile is a massive opportunity only heightened during the pandemic as audiences turned to their smartphones for the comfort food of apps and entertainment. Significantly, though, throughout this period consumer tastes and appetites changed. Users had both the time and the desire to discover new apps and content, a dynamic that allowed many niche apps and content creators to gain mainstream appeal and profits. In some markets, it created a perfect storm of opportunity for hyperlocal news and entertainment that meets consumers where they are.

Continuing with our series of industry interviews [video below], I talk to Jani Pasha, Founder and CEO of Lokal, who is harnessing hyperlocal content in a play that has the potential to make it the NextDoor of India. With a model built on monetizing connections and transactions at the intersection of community, content, and commerce, Lokal is making the most of a booming opportunity.

The model is smart and replicable in other markets. However, Lokal also benefits from a seismic shift in the fabric of its addressable audience. For the first time, India now counts more Internet users in rural areas than cities. And rural users typically aren’t as interested in national and international news developments. Instead, they crave information about civic, political and social issues that impact their towns and villages.

But India isn’t the only country experiencing these shifts. The explosion in the number of Internet users, accelerated by the pandemic, reveals opportunities in regions such as Central and South America. While we might think that growth has slowed, in the last 12 months alone, the total number of Internet users globally has grown nearly 8% to reach 4.72 billion. That’s more than 60% of the world’s total population.

From silver surfers to app initiates, new users in these regions rely on mobile and apps as their personal lifeline for news and information (even education). They turn to them to make daily decisions about how they live and what they buy. Tapping that potential requires companies to micro-segment audiences and tailor content to the needs of towns and communities, not cities. It also helps to focus on fundamentals.

Understanding that new users are likely to be low on the learning curve, Pasha made a bet on voice that paid off. Bypassing bell-and-whistle tech features for a dead-simple interface like voice fast-tracked new users to frequent app use and interaction. Ease of use also increased trust in the app. And that trust allowed Lokal to acquire new users easily through the most effective advertising on the planet: word-of-mouth.

Voice also empowers every user to make a contribution. This enabled Lokal to grow its ecosystem at minimal cost. Users call in stories about developments in their local towns, creating the content that keeps other users engaged and loyal. They rely on the app to learn about offers and events nearby, sparking conversations that end in commerce conversions.

And this is where Lokal’s strategy to be a local content platform, not a content provider, makes business sense. By positioning itself as a super app — one that allows a user to access several services in one place — Lokal establishes itself as the trusted middleman in interactions and transactions. What’s more, Lokal drives in-app activities it can monetize. And let’s not forget that first-party data is gold.

In our interview, Pasha shares how Lokal is training creators to ensure its content is fresh, relevant and relatable for audiences who crave hyperlocal content on their terms. He also weighs in on the future technologies and opportunities local news apps and outlets everywhere should embrace to grow their revenue streams.

WATCH OR LISTEN TO THE FULL INTERVIEW

FULL TRANSCRIPT

Peggy Anne Salz, Founder and Lead Analyst of Mobile Groove interviews Jani Pasha, Founder and CEO of Lokal:

Peggy Anne Salz: The pandemic had a massive impact on local media. In the U.S. alone, more than 300 national newspapers closed their doors. Local newsrooms also shut down contributing to the growth in news deserts, that is, cities where people depend on one local news source, if any at all.

But one company is bucking the trend big time, Lokal, a hyperlocal news app in India is not just growing its user base, it’s also making money. It’s a new twist on monetization. And we get the inside track here on Digital Content Next. I’m your host, as always, Peggy Anne Salz, mobile analyst, content marketing consultant, and frequent contributor to DCN, which is a trade association serving the diverse needs of high-quality digital content companies globally. And in this series, we shine a light on the people pushing the envelope. That’s why I’m so excited to have Jani Pasha, Founder and CEO of Lokal. Welcome, first of all, to Digital Content Next, Jani.

Jani Pasha: Hi, Peggy. Nice to be here.

Salz: Absolutely. And coming to us from a very hot Bangalore today, I understand.

Pasha: Yeah, right. It’s very hot, actually.

Salz: So let’s start with Lokal. You have described it as a hyperlocal Tinder because it cuts out the middleman in finding a date or partner. But it’s also a news service. It’s much more than that. So tell me about Lokal and, above all, the user experience.

Pasha: Yeah, Peggy. So we are not just only the Tinder of that place. We do quite a lot. But I’ll tell you the backstory of how we started. So essentially, if you take India, it’s a very diverse country with 90% of its population living in tier-2, tier-3 cities, and towns of India. And these people, most of them, have not traveled further than their adjacent district, because it’s so diverse that with every 50 to 100-kilometre radius, your food habits change, cultures change, language change quite frequently.

So they are staying in those locations of their towns and cities generationally with their parents, grandparents, their homes, and businesses. So naturally, they’re so curious to know about what is happening around them. And there is one more factor that kicked in, in 2016, Jio, a mobile operator who has reduced the prices of internet drastically to make India the cheapest place for 1 GB data for you to use mobile internet.

So then we have this, all these 90% Indians who didn’t have access to internet previously suddenly had access to internet. But essentially, these users are new internet users who are not comfortable in English language. And so then what will they do with the internet, right? So Lokal is the platform which we started it as a platform to deliver hyperlocal content, which is extremely useful for them. And that is the gateway of how they’re adapting to the internet to use internet more usefully in their life. So today, if you take this 90% Indian audience who are new to internet, they are using internet prominently for entertainment, either to… You know, we used to have TikTok. We don’t have it anymore. It is banned by the government. So there are many TikTok parallels and YouTube and Facebook. And then they use WhatsApp for communication.

Apart from that, they can’t use internet meaningfully. And Lokal is actually being that platform giving them the content that they can use and that is of importance for them. Then naturally, making them use internet for multiple use cases. And as at a location, our density of usage increased. We evolved as a platform. So you rightly said we evolved as a Tinder, a place where people find other people to get married. It’s a place for businesses to advertise about their businesses to local community. It’s a place for businesses or people to actually sell their properties. And all this is happening in their native languages of Telugu, Tamil, and Kannada. We are expanding across the country. And we have seen because we have a lot of density in that location, users are adopting platform like crazy with more use cases coming up almost every day.

Salz: But, of course, internet penetration alone doesn’t spell the profits that you’re getting. Part of it is also the experience. You talked about ease of use. You talked about local languages. What are some of the innovations in the UX and UI design that contribute to your success? What does an app with local news need to look like and offer?

Pasha: Very interesting and relevant question, Peggy. So when you talk about these new users right, so all the smartphones have the keyboards in English language. So one challenge when we’re trying to build Lokal was how can you make the content creation easy on Lokal, especially that of text format.

Like, a lot of information about what are the vegetable prices in that location to what are the updates happening in that town, not everything can be captured on video. So they have to be typed. How can you make that easy? So, the first thing that we did, or we built was, making this creation easy, where the user will input the content by voice instead of typing. So they are using voice to actually create the content. And once we started doing that, we realized that creation with our voice is much more convenient than typing on a keyboard because you have to… It’s not natural, right?

Like humans, we speak to each other. So that’s a major shift, right? So if you go on a website today like on Amazon, you have multiple navigation. There are filters, there is sorting, there are multiple pages, multiple categories, but for an interaction, like the natural interaction for a shopkeeper in our location is to go and ask to a small retail shop owner that, “You know, what is the cost of this item? And how can I get it?” It’s natural voice-based input. In India, a lot of businesses are SMEs, sort of small and medium businesses unlike in U.S. where you have a Walmart. You go and then you select. It’s a voice-based communication. You ask, the shopkeeper goes and gets the information, and we’re replicating the same because the technology has caught up.

Salz:Interestingly enough, you were talking about how your audience is very focused on local content. I mean, hyperlocal is really hot in India right now. It’s fascinating that local newspapers, right, newspapers are growing at a double-digit rate. Now, you also have impressive growth results. Now, I’ve seen numbers growing 25% roughly month on month, that’s the last I’ve read, and that’s because of your monetization model. So one is the content, but it’s also a very smart approach to how you generate revenues. Tell me about that.

Pasha: We have built a playbook, via which we launch a location, and we get local content creators in that location to create content, which is very relevant to that community, very, very hyperlocal in nature. And then you get a density of users using the application. And once you have that critical mass of density at a location level, then it becomes a platform where everyone…like, everyone relevant started coming onto the platform, and then they start doing a lot of things, which are monetizable.

Even this is true for people in the West also. Newspapers used to be the place for everything, right, at a location level. You want to do real estate, you want to do jobs, classifieds. Everything used to happen on newspaper. Internet came in. All the small, small parts became large businesses, right? Craigslist, Airbnb, they’re all part of this local newspaper, right? Had these newspapers, you know, are technology-friendly or had they been…had they had that vision or foresight, they would have been the super applications that everything is happening on them.

It’s just that the news publishers migrated their digital publishing online, but they left the rest of the parts for others to pick. In India, we have that opportunity right now, where it’s a very new audience. Internet is being built for them in their native languages. And Lokal is trying to do that with our approach of delivering hyperlocal content. So we don’t consider ourselves as a local news platform. We consider ourselves as a local content platform. So that is the different approach that we are taking compared to newspapers, Peggy.

Salz:That is fascinating because you’re showing that there is a great deal of benefit to being a fast follower here. I mean, you have purposely… It sounds like you have thought this through, Jani. How to be a content platform, keep the social media, keep the connection for yourself and not give it over to the big tech giants or the big social media platforms. That’s the focus. That’s the essence of your strategy. How do you keep the momentum? Because, of course, you’re on a growth trajectory, all of India is on a growth trajectory. And high growth usually means high competition. And how are you keeping these large companies literally from eating your lunch?

Pasha: Our competitive advantage that comes in is based on how hyperlocal we are and how much our team understands the nuances of India, which is very difficult for a tech platform sitting in the U.S. or sitting in some other place to understand and build for it. And these are very new behaviors Peggy. So, as I told you, right, how does a business establish trust digitally? What happens on Amazon is that you go and list on Amazon their ratings, and those are the places how you do it. But how will it happen for a new internet use case, right?

For these very new people where the trust on internet is low, right? How will you do that? It’s a new challenge that we will solve probably for a small business to establish trust very quickly on our platform, and how they can do it. So it’s just that, the nuance, I would say. I would like to summarize that the nuance is very difficult for someone to understand. And hyperlocal in general, is a network effects business, right? You have large density using your platform for multiple use cases, someone coming and replacing it would be difficult.

Salz:It’s interesting that you started monetizing wishes. Tell me about that.

Pasha: It’s just crazy. We never expected all this to happen. We just thought we’re solving a problem of local content not available digitally. When we started creating content, people started coming. So that is the nuance. Like, in India, you have this behavior.

In the small town of India, especially in the southern part, this is very prominent, so that south Indian part, that if Peggy you were a friend of mine and I want to wish you a happy birthday, and I want to do this in a way that everyone in the community would know that I care for you, and we are actually close friends. And how will I do that? I used to either buy advertisement on newspaper with your photo, my photo coming and I’m wishing you happy birthday. Or I am sticking a big banner in the city or town center wishing you a happy birthday.

So the same behavior has been adopted on Lokal now, where the same people who used to do that are posting their wish, like I’m wishing Peggy happy birthday. So there is a standard template where your photo, my photo, will come and I’m broadcasting it to 10,000, 15,000 people in the town, the same purpose they wanted to accomplish previously, now, they’re accomplishing on Lokal. And they have that data to see also that how many people are actually looking at it. So this is being monetized on Lokal. And this is a very, very interesting, unique use case, Indian use case that we are monetizing. And we are seeing a lot more use cases coming like this, and we’re super excited for that.

Salz: You’re also speaking very much as the maker of a content platform. And, of course, a content platform needs creators, needs citizen journalists. It’s all local. So it’s probably very much just about empowering individuals at the local level to grow your business, how do you do that? How do you find them? Train them? How do you make it possible for them to contribute to your platform?

Pasha: The prominent content distribution platforms used to be newspapers like how it happened in the West also. And over the last three, four-, or five-decades time In India, large news publications, this content distribution platforms, have created a lot more content creators in these locations by training them, by informing them, by letting them know what is happening.

And most of these creators in this town used to work for this large distribution platforms like newspaper or television for free, most of them. Why? Because I told you, right, how important these small locations and communities are for these people.

So if I am a creator who can get the word out in a big distribution place like a largest newspaper, I get invites to events happening in the town. Anything big happening in the town, I get to know about it first. So I’m an influencer in that location. So then we have these influencers across India, hundreds of thousands of them. What we simply do is that we have this network of people. We have this digital crunch of hyperlocal content; we just connect them. And that is how we are getting this content.

Salz: You are more than a Nextdoor in India, you’re a content platform, news platform connecting, making business possible, helping merchants. And the reason I have you here today on Digital Content Next is because there are lessons here for publishers everywhere. What do they need to pay attention to if they want to succeed in hyperlocal news?

Pasha: My take is that technology is evolving very rapidly. Publishers should be open to work with new technology coming in. Like, Substack is a great platform where publishers are able to monetize their content. So there are a lot more innovation that is coming. So publishers should be thoughtful and be open to experimenting with these technology players because these new platforms are coming in. And with the creator economy coming in, I’m also very hopeful of how publishers becoming much more important than what they used to be before.

Salz:We started off by talking about the situation particularly in the U.S. where local news, local newsrooms, they are declining, there’s no question. What would be some advice to those that are there to say, “Here’s what you can do to up your game. Here’s what you can do to be sustainable and successful?”

Pasha: I think for small-level publishers, I think what is working for us is being hyperlocal and having a plan. And for us, it’s about figuring out that playbook of how you can get or make the things work at a location. So I think for publishers, especially individual publishers, I think hyperlocal play is going to work, with them also having…who are open to work with, new technology players, which essentially are tools and not platforms possibly.

So Substack is a tool for you to distribute your content. It’s a tool, right? And essentially, for payments, you can use a tool. So someone who is more open to work with these technology platforms and having hyperlocal focus would be able to build sustainable businesses. That is what our belief is. And I can’t compare clearly India to U.S., but in India, specifically, because of how the market is, the maturity of the user towards internet interest, it’s going to be very, very large play in India, especially the focus of hyperlocal.

Salz: So very, very much about being a platform, which is what you’re doing connecting people, connecting businesses, that’s what local content can do really well. The monetization model currently is about classifieds. What’s it going to be going forward as you try to be more and more a super app?

Pasha: So, yeah, Peggy, we are today connecting people, and monetizing on that for the sake of making money, for the sake of selling property, for the sake of improving…giving deals to people, small businesses advertising about their offerings. As the trust increases among these people, we would eventually go into a place where we will enable commerce as well. So that is what the plan is.

We will enable commerce. We will enable these local economies much more digitally. And we are a user-focused company, Peggy. So we have a creator who creates content, and we always think about how we can empower him or her, how can we make their lives easy. Similarly, we have businesses and how can we better help them to get more business. In that, the natural next step is to enable commerce on the platform to have additional revenue streams for them. So we will figure out how we will monetize. But we want to build that use case on our platform. It can be search, it can be something else, we’ll figure out. It’s too early right now. Probably in a year or two, I can tell you a lot more about it.

Salz: Great, Jani. And I think I’ll be back to hear it as well. Thanks so much for sharing your story at Lokal with me today.

Pasha: Thank you, Peggy. And nice talking to you too.

Salz:And thank you, of course, for tuning in and taking the time. More in this series about how media companies like Lokal are taking charge of change in their business. And in the meantime, be sure to check out digitalcontentnext.org for great content, including a companion post to this interview, and join the conversation on Twitter @DCNorg. Until next time for Digital Content Next, I’m Peggy Anne Salz.

“Transparency is an important part of everything we do at Facebook.” Well, at least that’s according the first line of the company’s just-released Widely Viewed Content Report. The report is intended to provide insight into what content flowed across Facebook in the second quarter of 2021. In particular, it examines what content was viewed most in consumers’ News Feeds.

Facebook claims that most of the content on its platform comes from its users’ friends and family. The report states that news (or content that appears to be news) only represents a small fraction of what users see and share. It appears the company wants us to believe its platform is filled with family pictures and GIFs of kittens. Move along, industry watchers. According to Facebook there’s nothing to see here!

Cleaning house

The New York Times uncovered that this wasn’t the company’s first such report. According to the Times, Facebook prepared a Widely Viewed Content Report for Q1 but not release it. Apparently, the picture it painted wasn’t pretty.

According to the Times, “the most-viewed link was a news article with a headline suggesting that the coronavirus vaccine was at fault for the death of a Florida doctor.” Although the article came from a major publisher, it was the headline – and the way it was shared in a particular context by anti-vaxxers – that put it on top. Meanwhile, the 19th most popular page during Q1 was from the Epoch Times, an outlet widely known for pushing conspiracy theories.

Weird. These aren’t exactly posts about grandma’s mouth-watering apple pie or dare devil kittens hanging from ledges.

Remember, Facebook only reluctantly published the Q2 report after it spent a year discrediting external research from its own CrowdTangle data, which measures engagement (liking and sharing). When Facebook dismissed these reports, academics and researchers responded by pointing out that they were simply using the data Facebook had, itself, put out into the market. Meanwhile, CrowdTangle’s personnel were dispersed to other parts of Facebook, and the tools were pared back by Facebook, in what looked like an effort to regain control of the data and narrative.

It kind of feels like Facebook is hustling us in a giant game of Three-card Monte.

Revisionist history on repeat

Maybe there are those still inclined to give the company the benefit of the doubt. As Facebook spokesman Andy Stone soft-played their actions when he tweeted “we might have been guilty of cleaning up our house a bit before inviting company.” Unfortunately, the dumpsters full of incendiary trash impacted untold numbers of “guests” way before Facebook purportedly tidied things up and invited the “company” of critical analysis.

Facebook has a long track record of covering up and thwarting transparency at critical moments including the countless times where they enabled companies to collect data about consumers and then repurpose that data for number of reasons. Notably, these included selling Facebook’s data to third parties like Cambridge Analytica, which turned out to be one of the largest data breaches in history.

Deception is part of the business model

Recently, Facebook blocked researchers ability to gather information about what political ads are being shown across their services. It was especially galling that Facebook justified its decision as a protection of “user privacy.”

Given the company’s track record, it shouldn’t be surprising that Facebook once again opted to block full transparency. And yes, once again, the real reason is because it could hurt the business model. Even the FTC weighed in and warned Facebook not to use privacy “as a pretext to advance other aims.”

Truth told

For the Facebook model, it doesn’t matter whether the content is truthful. In fact, if there is a bias at all, it must be in favor of the least trustworthy, most salacious content (e.g. vaccine misinformation, Epoch Times) because that content tends to catch fire more quickly. And profits are way up. The business model is clearly working.

On top of that, at key junctures in Facebook’s history, executives have unequivocally chosen to hide the truth to maintain these profits. Vague commitments to transparency come only when they find themselves once again caught with a hand in the proverbial cookie jar. And now, even those promises to “do better” come with a giant caveat: We’ll only tell you something if it makes the company look good.

At this point, there are legitimate questions about whether Facebook is a good-faith actor that can ever play a constructive role. Facebook’s business model is at odds with transparency and their executives seem committed to running the business like a Three-card Monte hustle. With deep political divisions in our country hindering our ability to tackle a shared crisis (or even have a thoughtful discussion), we need leaders to step forward and demonstrate an unequivocal commitment to transparency and trust.

Streaming services continue to rack up subscriber growth in the global marketplace. In fact, Juniper Research forecasts nearly 2 billion active subscriptions globally to on-demand video services by 2025. That’s an increase of 65% compared to the end of 2020. Domestically, USB analysts believe that Americans will add 50 million net new video subscriptions this year, up from a 47 million increase in 2020.

To gain insight into the market breakdown of global streaming marketplace, Finder.com conducted a survey with close to 30,000 consumers across 18 countries. In total, approximately 56% of consumers report having access to at least one streaming service. Finder.com is a content site focused on helping consumers make informed decisions in categories such as credit cards, mortgages, health insurance and others.

Streamer concentration and service popularity

New Zealand and Brazil represent the highest concentration of respondents using at least one streaming service (65.3% and 64.6% respectively). On the opposite end, France and Pakistan report the least number of streamers in their countries, 45.2% and 44.6%, respectively.

Respondents were asked specifically about three global services: Netflix, Amazon Prime, and Disney+. Netflix is by far the most popular streaming service among the three with more than two in five (40.1%) consumers subscribing to it around the world. Nearly 14% of those surveyed subscribe to Amazon (13.9%) and 13.1% subscribe to Disney+. Ireland had the highest number of respondents reporting that they subscribe to Netflix and Amazon Prime (56.9% and 19.9%, respectively). The U.S. ranked the highest in Disney+ subscribers at 32.8%.

Demographic appeal

Women tend to consume more on these platforms with an average of 57.2% reporting at least one streaming service compared to men at 55.6%. Countries with highest female usage are Ireland (69.2%), Brazil (65.9%) and New Zealand (65.3%). The U.S. ranks fifth with at least 63.9% of women reporting that they subscribe to at least one streaming service. In terms of popularity, Netflix is the most popular streaming service among women (45.2%) followed by Disney+ (14.7%), and Amazon Prime (13.8%).

U.S. streaming close up

The survey included Netflix, Amazon Prime, Disney+, Hulu, and YouTube TV when asking U.S. respondents about streaming services. Again, Netflix leads with 45.4% of respondents saying they use it, followed by Amazon Prime (32.8%), Hulu (22.3%), Disney+ (18.1%) and YouTube TV (7.4%).

Hands down, Netflix is the most popular platform in the U.S. across each age group. Sixty percent of people aged 18-24, 54.0% of 25-34-year-olds, 53.1% aged 35-44, 50.2% of 45-54-year-olds, 42.3% of 55-64-year-olds, and 38.2% of those over 65 all report that they use the streaming service.

Subscribing to video streaming services is the norm for today’s consumers. But competition is fierce. These services not only need to attract subscribers, they must also hold on to them. With an increasing number of subscription services, retention is critical to market growth and expansion. Importantly, subscription services need to employ strategies that build loyalty, provide added value, and offer personalization to compete in the global marketplace.

In Greek mythology, Odysseus faced many harrowing close calls, traveling to Hades and back just to find his way home. For many involved in the evolution of ConnectedTV, it has felt very much like a 10-year journey to get to the juncture where the promise of the platform finally meets the commercial needs of the market.

Much like Homer’s Odyssey, there always seems to be one last challenge to face before reaching friendly shores. As video investment continues to surge into CTV, the competing challenges between programmers and CTV platforms are coming into sharp relief. The solution may lie in mutually shared data so that platform and programmer can harness the rising tide of OTT viewership on CTV devices and the revenues that come with it.

Big picture problems

For digital publishers, CTV will mean presenting their content on the big screen for the first time. This represents a big leap into the living room on platforms they don’t really control. Even an owned-and-operated OTT app must adhere to the specific requirements of the CTV platform where it resides. And that often means building multiple variations of the app just to conform to the needs of the platform. Even with native video players for environments like AndroidTV, the specific advertising parameters a publisher must comply with to succeed on a CTV platform vary wildly.

Traditional broadcast and cable networks approach ConnectedTV with a set of assumptions from the legacy world of television. Unfortunately, these do not always translate well into CTV. First, they have windowing restrictions around licensed content that can produce an uneven experience between their linear broadcast, cable VOD, and CTV offerings. Second, without an accepted currency equivalent to Nielsen ratings for CTV viewership, they are missing out on the opportunity to bind all TV viewing of their content into a single, sellable, audience. (Nielsen One – a potential solution – is slated to debut in Q4 2022.)

Add into this the fact that ConnectedTV device platforms are becoming owners of advertising inventory across all of the programmers on their platform, and the situation becomes even more complex for everyone. In the past, a TV network would surrender two minutes per programming hour to their MVPD distribution partner, or roughly 12.5% of total inventory. This was mitigated by the terms of a carriage agreement that permitted the distributor to only sell local ads for insertion into their physical distribution footprint. Today, a CTV platform has rights to 40% of a programmers’ inventory and no restrictions around to whom it can sell.

Transition and targeting

Web publishers had to master new techniques and methods to benefit from the consumer transition to mobile screens. Now these same web publishers that have built strong advertising supported video businesses will need to recalibrate their workflows to ensure that CTV publishing is worthwhile. Ultimately, their ability to represent the full scale and dimension of their audience, across owned and third-party platforms, will have a profound impact on their success.

The value of a programmer’s CTV advertising inventory, despite residing within the same content network and delivery platform, is influenced dramatically by the audience targeting data that each party, owner, and distributor, is able to provide. When a network sells this CTV inventory directly or even programmatically, they can apply a limited amount of first party data to the placement given the lack of unique identifiers provided by the CTV platform. The network falls back on presenting its CTV audience as an extension of its broadcast audience. That is, unfortunately, an imprecise and potentially loss-making approach.

Connected competition

The CTV platform is not so constrained. While publishers may not have the option to sell these networks by name, their aggregation of so many CTV impressions allows them to compete directly with the programmers for the same advertising budgets. And because of the additional first party data they have about the consumer: viewing habits, zip code, and even TV size, they can very often out compete the networks for the same campaign commitments.

So here we have the Scylla and Charybdis of CTV advertising. On the one hand a national brand advertiser can approach multiple networks for their CTV campaigns and craft a schedule that will guarantee distribution and spot delivery. They can be very specific around selected programming and category exclusivity if they so desire.

On the other hand, going to one or several CTV platforms for the same campaign will allow a buyer to define a desired target audience profile to reach. However, they will have limited control around the content adjacency and context of their placements. And the reporting and reconciliation of campaigns is also different in degree and detail, forcing the advertiser to now undertake an analytical effort to assess ROAS from each source.

The route to revenue

Scylla, the six-headed monster in Homer’s The Odyssey ate sailors that passed close enough to be claimed. She sat on one side of the Straits of Messina. Charybdis, a violent whirlpool that would devour entire ships, was at the far shore. Sailing too close to one or the other ensured an unenviable end. Buying impressions from only programmers or only from CTV platforms will leave advertising brands at a disadvantage precisely at the time when CTV can command the enormous share shift of video investment coming from a declining traditional TV audience.

The stakes aren’t quite life and death for CTV advertising. However, it’s worth recognizing that this state of affairs will continue to constrict the growth of the business unless additional progress can be made to harmonize network-sold and platform-sold CTV impressions.

It is incumbent on the industry to coalesce around a shared data set that both platforms and programmers can provide to advertisers programmatically such that they can evaluate and purchase these avails with the same confidence that they used to purchase television. The rising tide of OTT viewership on CTV platforms, on both linear FAST channels and AVOD, suggests that rallying around a common baseline for CTV inventory stands to benefit both the content rights owners and distribution platforms equally, when each will finally have a stake in one another’s success.

We all know that the days of the cookie as the primary means to ad targeting and personalization are coming to an end. From increased legislation to ongoing browser updates, the time has come to put the cookie behind us and move forward. The good news is that there are tried and true methods that ensure the free flow of information and effective advertising.

While brands, publishers, and platforms are likely to leverage cookies for as long as they can, the industry has viable solutions and advertisers should take advantage of them. Those who have gotten a head start already see the benefits of an addressable, cookieless solution that enables authenticated user experiences. Brands and publishers that have already made the transition should use this time to establish stronger relationships based on trust through first-party data strategies. Those who haven’t yet started the journey away from third-party cookies should get started right away by leveraging a trusted, first-party authenticated solution.

Authenticated audiences

Previously, brands looking to reach their audiences have been overcompensating for the lack of a transparent, authenticated solution. Data-driven publishers, with established, first-party relationships can leverage their authenticated data so marketers can target audiences and measure campaign outcomes with people-based identity.

In the past, marketers looking for a measurable solution had to turn to social platforms’ walled gardens, which have enjoyed the benefits of disproportionate media investments. Historically, advertisers spent 60% of their digital advertising budget on reaching audiences in walled gardens, allotting only 40% of the budget to the open web. Yet, consumers spent more than half of their time on the open web (66%), compared to just 34% on closed platforms.

As independent publishers embrace the tactics of walled gardens, they leverage first-party authentications to deliver better, more targeted advertising. Initial campaign results from two publishers, Newsweek and Discovery, illustrate that an authenticated, cookieless solution has proven effective.

People-based solutions

Publishers and brands can now connect identities without the use of cookies or compromising data. For example, Newsweek was able to better plan and execute on advertisers’ marketing campaigns by leveraging a people-based, privacy-safe, cookieless solution that enabled publishers and brands to match identities.

Leveraging solutions independent of third-party cookies, the Newsweek team saw a total lift in eCPM as high as 224%, with an average lift of 52% across all web browsers. The lift in specific browsers — a CPM lift of 55% on Google Chrome, and a 93% and 60% CPM lift on Firefox and Safari, respectively — indicates the significant impact the new, cookieless solution can drive as an alternative to third-party cookies and in cookieless environments.

Although third-party cookies are still a capability in Chrome, Newsweek benefited from an audience lift on the browser by activating on the new cookieless solution. Because both Firefox and Safari no longer enable audience reach with third-party cookies, the lift on both browsers demonstrates how the cookieless solution enables a new, more premium channel based on authentications where marketers and advertisers can reach an audience they were not previously able to.

Newsweek’s COO Alvaro Palacios said, “Newsweek has proven through testing that digital media does not need third-party cookies to increase yields and the value of our inventory. This ID solution provides the infrastructure to match our readers with a brand’s customers, for marketing that could be more effective than with third-party cookies.”

On mobile devices, publishers are also seeing a higher CPM than on cookieless mobile web inventory. Through their new ID solution, Newsweek also achieved a CPM lift of 53% on iOS, compared to those that did not activate on this ID. Discovery Inc., a publisher with sites including HGTV.com, TravelChannel.com, FoodNetwork.com and DIYNetwork.com, also saw an average eCPM increase of 44% when enabling activation on the same ID solution on their cookieless inventory.

A new ecosystem where publishers and brands win

The CPM improvements that benefit Newsweek and Discovery are just an example of the incremental revenue opportunities achieved by leveraging an authenticated solution. As publishers continue to grow their addressable inventory, their revenue will also flourish. Brand marketers can now buy inventory activated by authenticated, first-party data. This enables them to reach more consumers on more channels than ever before. And that’s something third-party cookies were never able to achieve.

While third-party cookies may still exist in the near-term, advertisers should take advantage of the proven, more viable solution already available. Consider the cellular network transition from 4G to 5G. With speeds 100 times faster than 4G and better connectivity for seamless user experiences, 5G is the clear winner for a preferred connection. Yet, 4G still exists. In this same way, having already proven themselves to be more effective, authenticated cookieless solutions have also become the preferred solution while third-party cookies remain.

The digital advertising industry is constantly balancing the interests of publishers, brands, and browsers. The sometimes-competing interests may feel like a three-way tug-of-war at times. However, there are proven viable alternatives to third-party cookies that benefit brands and publishers equally.

To get ahead of impending browser changes, publishers must own their trusted first-party consumer relationships through authenticated solutions. Once publishers succeed in establishing trust with their consumers, they will then be able to develop a relationship that’s independent of cookies. And that will improve the user experience and increase yield for publishers and the brands that work for them.

/ An inside look at the business of digital content

/ An inside look at the business of digital content Archive

Archive