Digital video in 2019 looks like digital content at the dawn of the information superhighway when it started to be commercialized in formative ways. With booming audiences for streaming video, new OTT video services are gearing up to ‘party like it’s 1999’. While the industry has been overshadowed by Netflix for quite some time, a slew of new “Princes” is making their presence known, including Disney, WarnerMedia, and NBCUniversal.

The OTT service establishment today—spearheaded by Netflix along with Amazon, Hulu, and Apple—spend a staggering $20 Billion plus dollars annually on original content. At the same time, up and comers like Pluto TV are trying to replicate the success of traditional TV over the Internet. And, under the ownership of Viacom, they’ve started to stream premium original content in a channel lineup that now includes BET, Comedy Central, MTV, and Nick.

On the other hand, YouTube is attempting to crossover from being a user-generated network to a general entertainment content destination. And numerous video services have emerged that cater to more niche audiences or content segments. These range from Vimeo’s traction with small business organizations like yoga studios to offerings like Lifetime Movie Club for original drama fans and Britbox for domestic fans of British programming.

The point of saturation will inevitably arrive and the number and mix of AVOD and SVOD will eventually play out. If this concerns you, remember that cable boasts thousands of channels. The digital tuner on a TiVo can access over 1,300 of them. Nationwide, without duplication, there are tens of thousands of channels and over 500 premium scripted shows.

History is a

reliable predictor of the future. Looking back, linear TV grew five-fold in channels

and shows during the golden age between the 90s and early 2010s. Even so, total

viewing time increased by just 15% as monitored by TV measurement companies

like Nielsen. Ultimately, free time and content consumption are on an X-and-Y

axis.

The heaviest TV viewership comes from a core of the total TV

viewing population, which is comprised of those over 55 years old in age. However,

the median age of a viewers for newer and more tech savvy OTT platforms is just

over 30 years old. Clearly, the preferences and expectations of younger

audiences are going to shape plans for premium content offerings in the future.

Keep in mind that the proprietary premium content offerings

of services like this will be a clear differentiator. Consider the much hyped

Disney+ OTT service. In addition to boasting its deep well of animated and

family programing, Disney is also the owner of the Star Wars franchise, which

provides an intergalactic bridge to the post-millennial generation. And let’s not forget that WarnerMedia

will soon distribute the Star Wars of our time: Game of Thrones. That franchise

alone could provide the foundation for a significant OTT presence.

So, what will happen next in OTT as established and upcoming

services prepare to battle? Most likely, the future will not belong to a

handful of OTT services alone. Rather, we’ll see the proliferation of OTT

brands that cater to niches of interest and genres, as well as those providing

general TV style content offerings. These services will range widely in terms

of content and tactics and the growing OTT audience will allow them to propagate

on the Internet like TV channels did on cable.

It is less about who is going to take over OTT and more about who is going to take their audience for a great ride on the TV superhighway.

Local television news enjoys a somewhat unique vantage point among audiences: It’s America’s most trusted source of news according to the 2018 Poynter Media Trust Survey. Just over three quarters of respondents said that they either trust local TV news “a great deal” or “a fair amount,” beating out network news at 55% and online news at 47%. (Though local newspapers weren’t far behind broadcast at 73%).

But local news is not without its challenges, as younger generations change their viewing habits and cord cutting becomes more common. In fact, bridging those gaps are the stated goals of CBS’ new local news streaming services. Earlier this month, CBS announced the launch of CBSN Los Angeles. It’s the second local news over-the-top service offered by the Eye Network after a version in New York started streaming last December. Available 24/7, the service offers viewers access to not only the regularly scheduled one-hour news broadcasts, but also exclusive news and weather content produced by a dedicated team.

A local stream

The effort is built on the experience and infrastructure of the CBSN streaming service launched in 2014, according to Executive Vice President and General Manager of CBS Local Digital Media, Adam Wiener. “It’s an investment in innovation. We want to be wherever our consumers are and we’re creating product to meet that need.”

While bringing local news to an online streaming might feel like the natural next step in news delivery, there could be reasons it ends up more complex than that. “I love the idea of experimenting with local news,” said Christopher Ali, associate professor of media studies at the University of Virginia. “I’m a huge fan of it, we need to find different ways to keep local news going.”

Ali also points out that the corollary of the fact that younger people not watching the news, is that the main audiences are older adults, Unfortunately, at least at present, this demographic is the least inclined to adopt new viewing habits. He thinks the audience for local news could remain older as there are unique properties of the local news viewership.

Youthful news

For example, to combat declining audiences, a February 2019 report from the Shorenstein Centre and Northeastern University suggested that local news needs to look at online outlets like Vox for inspiration. But that might not be enough to change local news’ fortunes among the young, says Ali. “We tend not to settle down until we’re in our 30s, which means that local politics, local zoning issues don’t tend to matter, really, until we have kids or we buy a house,” he says.

Another factor that marks the CBSN services are their locations in major hubs. With LA and New York online as well as planned expansions to Boston and the Bay Area, there’s not yet talk for movement to smaller markets. “Places that are hurting for local news are the mid sized cities, your Kansas City or St. Louis. These are the ones where we’re seeing the collapse of the newspaper, and also the kind of a less robust television ecosystem,” says Ali. “So how do we scale what CBS is trying to do to make sure that these other markets, which are quickly becoming local news deserts, are going to be served as well.”

Since not all small towns and remote areas have fast internet, that could also stratify the potential audiences for digital local news broadcasts, Ali says.

Consider the source

Valerie Belair-Gagnon, assistant professor of journalism studies at the University of Minnesota, agrees that any move to digital will favor those with better internet access. However, she also says that local news’ move to OTT is “part of a larger trend of news organizations to rely on third party platforms to produce news, reduce costs and a reaction to the diversification and segmentation of audiences.”

While CBS certainly has control over its distribution offering stream access through a website, it also has apps located on the App Store, Google Play Store, Amazon’s Fire TV, and Roku’s streaming platforms. For (relatively) smaller companies, these relationships have also proven to be a challenge to navigate. Apple has been accused of anti-competitive behavior by Spotify, and the music streaming service has filed a legal complaint in the E.U. It alleges that the 30% cut Apple takes from digital purchases grants an unfair preference for their own product.

Belair-Gagnon also worries about the ultimate responsibility of creating journalism could be rendered ambiguous. “In a world where news organizations are increasingly relying on third party outside of regulated channels and where there is increasing opportunities for different forms of storytelling, whose responsibility is it to produce news? Who is liable when journalists relinquish their control over third parties?”

The bottom line is that the need for local news is great and experimentation with ways to serve this market is critical. However, there also remain important unanswered questions in the path to modernize the evening news broadcast.

The fight for talent is on all over the world. Companies need more engineering, product, user experience, QA automation, and developers than they can find and incorporate in their business. In a recent 3Pillar survey, a third of global services decision makers said they used outside partners because they didn’t have the right kind of developers or that their developers didn’t have the right skills to get the job done.

More than ever, companies are bringing in outside help to serve their customers and hit their business objectives. This is a smart move. Most organizations don’t have the resources to hire and retain the talent needed to do this in-house, and it may take too long to hire a person at a time when what’s really needed is a team. The reality is that most companies will better achieve their goals by partnering with those with a diversity of experience.

No matter what “Agile process” you use, working

with a partner who understands the fundamental principles that make digital

products successful can help your company create new revenue, increase your

customer base and spur innovation.

This starts with

transitioning from an outdated “IT mindset” to a “Product Mindset.” This means

adopting a way of thinking that ensures that people at every level of an

organization are making the most effective, data-driven decisions with a shared

goal in mind. The most successful agile organizations are ones that are

applying these three core principles to make the most of their software

development approach:

1.Minimize Time to Value

Most products fail

because the team runs out of money and support before the product starts to

bring in revenue or serve customers.

Value only exists in the

hands of customers. Put the smallest solution to their biggest problems in

their hands, monetize it, and learn what to do next. A successful digital

product is one that creates dollars, instead of saving pennies.

Partnering with an

external technology provider can help agile organizations create a product that

furthers learning and starts earning revenue quickly.

2.Solve for Need

Every day, consumers

choose certain digital products while failing to choose others. A company must

deliver what the customers want and need most, so that customers continually

choose to pay for what the company is offering.

Many companies are

driven by internal forces. This could mean building products based on what

management is asking for or products that reflect what they think

customers want.

Co-creating with a

development partner that prioritizes solving for need can challenge a company’s

entrenched thinking and push back against “requirements.” This kind of

partnership will ultimately generate new ideas and can help companies focus on

outcomes, instead of attempting to solve challenging technical problems.

Technical problems are often an impediment to releasing a successful digital

product quickly.

3.Excel at Change

Great digital products

are never done. Companies must embrace changing customer needs and a changing

marketplace in order to succeed in the digital economy. Often, having an

outside partner can spur agile organizations to be more adaptable to change.

This may mean

implementing vital elements such as continuous integration/continuous

development, automated testing, and development and operations. It may also

mean adoption of new tools or new technologies, like robotic process automation

or virtual reality.

These partnerships

enable technology management to be more adaptable. Software leaders often tell

us that their firm’s sourcing policies and contracting rules slow them down.

They want to try out interesting software from new providers or an open source community

but must wait while their procurement colleagues argue about what are, in their

opinion, unimportant legal details. An outside partner that pushes to keep

change at the forefront, however, can play a critical role in a company’s

success.

Partnering with a

software development company that has product-oriented and outcome-driven goals

can accelerate the successful delivery of digital products, and help agile

organizations compete and win in the digital economy.

Consumer interaction on digital platforms is a key driver of

revenue for entertainment and media companies. With increasing affordability

and availability of broadband, mobile continues to be a strong contributor to the

growth of this segment. However, according to the new PwC’s

Global Entertainment & Media Outlook 2019–2023 Report, further

innovation and personalization will significantly change how we access and use the

Internet.

PwC predicts that creative new offerings and business models will increasingly revolve around people’s personal preferences. New applications will involve artificial intelligence in combination with digital assistants. Media companies will strive to build products that empower consumers to set their individual preferences and curate their own context.

The PwC Outlook Report cites personalization as a central theme in overall entertainment and media revenue growth. Global spending is expected to rise 4.3% over the next five years, with revenues hitting $2.6 trillion in 2023. The report provides a strong and notable resource for revenue estimates in the both the US and global markets.I

Additional forecasts from PwC’s Outlook Report include:

Subscription TV revenue in the U.S. will experience a 2.9% CAGR (compound annual growth rate) decline to from $94.6 billion in 2018 to $81.8 billion in 2023. Much of the loss comes from cord-cutting and SVOD competition. Interestingly, the US remains the biggest Pay-TV market accounting for 46% of the total global revenue in 2018.

SVOD’s continues its popularity as more streaming services are introduced and unbundling continues to grow. Newcomers to the market will need to differentiate themselves to attract subscribers.

The OTT market is also dominated by the U.S., contributing to more than half (55.6%) of global OTT revenue in 2018. OTT video revenue in the US reached $14.5 billion in 2018 and is set to double by 2023.

The U.S. virtual reality (VR) market registered $934 million in revenue in 2018 and is expected to grow at a 16.6% CAGR to reach S$2 billion by 2023. Gaming remains the primary application of VR, accounting for 57.4% of total VR revenue in the US in 2018. VR video, however, will see the most growth in the forecast period, climbing at a CAGR of 22.4% to reach $861 million in 2023.

There’s an important effort in

today’s entertainment and media marketplace to meet consumers where they spend

their time and to deliver what they need wherever they are. These sorts of personalization

efforts cut across OTT, SVOD, and VR. While evolving business models around customer

behavior is far from new, the renewed focus amplifies the importance of placing

consumers at the center of the media experience.

The advance of high-speed networks and affordable data plans hasn’t only whet audience appetites for unlimited anytime, anywhere access to the content they desire. It has created ideal conditions for data-hungry streaming apps to proliferate, displacing traditional broadcast TV, and driving the meteoric growth of on-demand video. The phenomenon is global in scale, but nowhere is the impact as profound as in India, the fastest-growing video streaming market in the world. In India, on-demand entertainment services are forecast to account for more than 74% of mobile data traffic by 2020, up from 47% in 2014.

Streaming viewership is soaring, but it’s Hotstar—part of the Walt Disney entertainment empire and India’s largest premium streaming platform —that is seeing numbers climb into the stratosphere. In June Hotstar set a new global benchmark for live events. It reported a record 18.6 million users simultaneously tuned into the company’s mobile website and app to watch the deciding game of the Indian Premier League (IPL) cricket games. This sort of high-octane content has allowed Hotstar to grow the number of monthly users across app and web to 300 million, up from 150 million the previous year.

Hotstar balances a mix of blockbuster entertainment (including rights to popular movies and shows from ABC, HBO, and Showtime) with a bouquet of content aligned with India’s obsession with Bollywood and demand for local language translations. (Note that India hosts hundreds of dialects and over 20 official languages). As a result of this winning combination, Hotstar dominates India’s on-demand video streaming services market. The latest research from Jana pegs Hotstar’s total market share at 69.7%, compared to Amazon (5%) and Netflix (1.4%).

Using data to differentiate the customer

experience

At first glance, it’s remarkable that large global players with deep pockets continue to struggle in the Indian market—despite significant investments to ramp up local content. But look under the hood, and you may be surprised. Hotstar’s success may start with broadcast rights for live premium sports paired with high-quality vernacular content that attracts record numbers of viewers. However, it’s driven by a strategy that harnesses personalization, recommendations, and psychographic segmentation to keep them coming back.

Finding

the right balance between acquisition and retention is crucial for a company

like Hotstar, which thrives on live events. It pays to spend millions of

dollars to acquire audiences at scale—but only if users don’t leave in droves

when the event is over. Hotstar turned a potential problem into a massive

opportunity by mapping individual user journeys to move audiences across the

funnel from freemium viewers to paid subscribers.

How

Hotstar moves viewers from fremium to subscription

In an

exclusive interview, Mihir Shah, VP of Product & Marketing Growth at

Hotstar, distills the company’s data-driven approach into the four fundamentals

companies must get right to turn casual users into committed fans.

1. Personalize the entire user experience

It’s

important to look beyond demographics to gain a deeper understanding of who

your user is, what job your product solves in their lives, and how they use

your product, Shah explains. In this scenario, actions are just as important as

inactions to develop relevant engagement and re-engagement strategies. How many

times has the user opened the app or viewed the content? How long has it been

since the last interaction? How quickly or slowly is the user moving through

the funnel, and what“nudges” might convince and—ultimately—convert them?

Shah says these are critical questions marketers can only answer if they get a

firm grasp of behavioral segmentation models aimed at understanding and

predicting user attitudes and outcomes. “Once you establish a degree of

predictability around how your users behave, the way is clear to progress users

through the funnel with the help of content that is packaged and promoted based

on a deep understanding of user personas and psychographics,” he says

2. Recommend your content along the customer

lifecycle

User

acquisition burns money if audiences don’t stick around to explore and consume

the breadth of content available on the platform. This can be a major marketing

challenge, and why a big part of Shah’s job revolves around “converting the

sports fans who come to our platform—about 70 to 80 million daily for live

events like IPL—to start watching more of the entertainment we offer. And,

ultimately, get them to commit to a subscription.”

Achieving

this objective requires the ability to identify and segment users based on

digital details, including their browsing and viewing history, content

consumption patterns and other preferences. “Based on a collaborative filtering

method, we recommend entertainment titles that other sports viewers watch,”

Shah says. “If the user is a free user on our platform, we move them through

the funnel by recommending content from our Premium library that they are most

likely to appreciate—content suggestions based on freemium viewership patterns.

The relevant recommendations are then delivered to users off-platform as part

of an omnichannel campaign strategy that spans push notifications, social and

programmatic.

3. Messaging must be personal and perfectly

timed

Keep

up the momentum with campaigns that seek to influence user behaviors, not just

move metrics. Shah illustrates using the example of users who have streamed

live cricket matches. “We know that sending them push notifications based on

the actual game event will encourage them to relaunch the app and view the game

in progress.” In practice, he says, this means “delivering over 100 million

push notifications tailored to the moment and timed perfectly within a very

small window of just a few minutes.”

It’s a critical timeline that Shah says Hotstar reaches with the help of CleverTap, a customer lifecycle management and engagement platform that is capable of delivering more than 25 million push notifications a minute/ Shah says it was essential to reach Hotstar’s app install base of over 250 million. Significantly, “event-centric” campaigns appear to resonate most with audiences, boosting engagement and the average watch time per session by 12% and more.

“As we

cross-sell entertainment content, let’s say a movie, to our sports viewers, our

marketing creatives bring out a connection between the sport and the

entertainment content, thus making the content more appealing to a sports fan.”

But making the connection is just part of the strategy. Shah stresses it’s also

a good idea to pinpoint the days and times of the week that different user

segments are the most active and receptive to push notifications. Hotstar used

these insights to optimize send times, increasing click-through rates by 3x in

the process.

4.

Engaging with users in real-time is a game-changer

RFM

(Recency, Frequency Monetary) analysis is a behavioral segmentation model that

examines user activity to identify how recently and frequently they performed a

key action. To make sure the effort marketers invest in this model also drives

returns, RFM also looks at the monetary value of the action (such as purchasing

an item or, in the case of Hotstar, subscribing to programming). Shah is a huge

proponent of RFM, a framework his company has harnessed to bring context to

user engagement campaigns and, more importantly, predict churn. In both cases,

Hotstar segments users in real-time based on certain actions or inactions they

undertake within the app.

Imagine

a scenario where users who were watching a particular episode of a series

simply leave the app for some reason. “We see that as a trigger and send them a

customized push notification encouraging them to come back to finish viewing

that particular episode at precisely that moment.” Similarly, users who have seen previous episodes of

a series but not the latest one, are sent a contextual push notification as

soon as the latest episode is released. The outcome, he adds, is “more

conversions and increased content consumption.”

The future is interactive

As Hotstar continues on its impressive

growth trajectory, Shah says, the company is ready to take on one more bet:

that “the future of all sports streaming will be social.” As he sees it,

there’s no reason to limit the flow of content to push or pull. “Why should

content consumption be one way?,” he asks. “Why can’t it be immersive and

interactive?”

To enable two-way exchange, Hotstar is

laying a new layer on top of its platform. Last year it introduced Watch`N`Play, a game that challenges

users to guess cricket gameplay and outcomes, as well as social features and

streaming using virtual reality (VR) to make the match more immersive. This

year Hotstar is going one better, adding “another layer of chat” to the

platform, allowing fans to invite their friends from their Facebook account or

phone book contacts to the platform.

Effective user acquisition ends in

advocacy, and that means meeting and anticipating needs that consumers

themselves might not be able to identify. “It’s becoming increasingly clear

that customers are hungry for more, even though they don’t know what they are

looking for,” Shah explains. It’s up to companies like Hotstar to pave the road

for this future, building a platform and adding what he calls “unique,

inevitable and incremental experiences” that go beyond just entertaining

content.

I recently connected with Christa Carone, who joined Group Nine Media as president in 2017, at the Collision Conference in Toronto, Canada. Carone, who came to the media side of the industry after leadership roles on the marketing and agency side, oversees Group Nine’s sales and marketing teams as well as its data insights group. Group Nine is a digital media holding company comprised of four popular digitally-native media brands Thrillist, The Dodo, Seeker, and NowThis. Carone and I discussed revenue and distribution diversification, content strategy, and building a business based on brand equity.

Here are some highlights from our conversation:

Michelle Manafy: Tell me a little bit about your content

distribution strategy and why you are all-in on social.

Christa Carone is President of Group Nine Media. Prior, Carone spent 17 years at Xerox Corporation, most recently serving as CMO.

Christa Carone: Well, I’d say we’re all-in on omni

channel—and that includes social. Right now, we’re distributing content on over

20 different platforms. That includes Amazon Prime, Pluto, Roku, and distribution

deals with networks literally around the world. So, our approach to being

completely agnostic on distribution is that we want to bring our content to all

of the different places where people are spending their time. And we want that

to be a pretty frictionless experience. Instead of spending a ton of money to

get you to come to my website, I want to bring our storytelling to the place

where you are already hanging out.

Michelle Manafy: Truly connecting with audiences at

scale almost sounds like almost an oxymoron to me. What do you think?

Christa Carone: You can debate that content is king

and distribution is queen and whether they have an equal seat at the table. But

that’s really kind of how I look at it. When both are working together extremely

well, you are able to build successful brands like The Dodo, NowThis, Thrillist,

and Seeker. It’s like really honing-in on higher value content. We’re building

lifetime value of the content, what’s going to keep an audience interested, and

remain totally agnostic on the distribution strategy.

Michelle Manafy: The trick, of course, is the

monetization. The other side of a distributed model is fragmentation. So, talk

to me a little bit about how managing all of those channels ties into an overarching

strategy.

Christa Carone: The beauty of our strategy is

diversification. I often say that if Facebook sneezes, we don’t want to catch a

cold. Just like in any industry, you don’t want to be overly dependent on one

particular revenue stream. It’s business 101. Media is no different than any

other type of business. So, that’s why we’ve been so focused on building

audiences across a number of different channels. We’re building audience on TikTok

right now. The monetization strategy there is nascent. But it’s going to come. IGTV

is another great example. We produce great content for IGTV and put it on IGTV

pre-revenue. But I have no doubt at all that Facebook is going to open up

monetization opportunities there. And I want to have established an audience when

it does.

Michelle Manafy: You mentioned diversification and that

every company should be focused on diversified revenue. I take it that Group

Nine that’s been baked in from the start.

Christa Carone: Keep in mind that we’re two years old. So, we’ve had the benefit of learning from a lot of traditional companies. And I often say: We’re not pivoting to anything. Some of our brands were born into video so there wasn’t a pivot to video. And the business model was already established. Some of our brands were social first. NowThis, in particular, was born as a social-first distributed brand. We didn’t pivot our business model from taking audience from owned and operated to distributing through external platforms.

Thrillist is the oldest of our brands and it has such a

loyal audience. So, we are looking at diversification around where we can take

the Thrillist brand and make it more of a whole-lifestyle brand.

Overall, our focus is on lifetime value for the content. So,

if we’re bringing in revenue with licensing, great. Bringing in revenue from

the syndication model, great. If we’re bringing in revenue by production deals

with OTT content providers, like a Netflix, that’s perfect. And if we are continuing

to bring in a healthy amount of revenue from advertising, wonderful. And increasingly

we’re thinking about how we can tap into other revenue streams like commerce and

events.

Michelle Manafy: Could you tell me a little bit about

your commerce strategy?

Christa Carone: Our approach to commerce is really looking at brands like The Dodo and Thrillist and saying there’s intellectual property here. There’s a maniacally loyal fanbase. Can we be licensing The Dodo into product? The Dodo clearly has enough brand equity to be producing large scale consumer and canine events. Thrillist has been a friend to people for a long time. It is your recommendation action for food and beverage and travel. So, our ability to take that brand equity and bring it into commerce is already built in. And stay tuned: We will definitely be doing some more on that later this year and we just hired a head of ecommerce.

Michelle Manafy: So, you mentioned that maniacal

audience, that loyal audience. What’s the Group Nine secret? Because, as

publishers, that audience relationship is what differentiates us from the

platforms.

Christa Carone: It’s such a credit to our editorial

teams. They know how weave a great narrative and tell an amazing story. It

sounds simple but I’m always amazed … A great example is from NowThis. Many

people are familiar with the NowThis video about Beto O’Rourke that went viral.

The raw footage of that video was already posted on Twitter. It already lived

on the Internet someplace. The NowThis team found it and was able to put it

through their storytelling lens. They said how can we construct it in such a

way that viewers are compelled to watch the entire piece? There is an art to

it. There is a narrative that was built in through the use of text on the

screen, through the use of effective editing so that we as the viewer were

compelled to watch it from start to finish. That is the secret sauce that

really exists within our editorial teams and applies to how we produce content

across all of our brands.

I would say the other massive factor for us is that scale

matters. We have such amazing insights that we’re able to glean from the

consumption of our videos that informs how we produce content. Based on our scale,

our data team is looking at 115,000 views of our content every minute. Every minute. We’ve built a very sophisticated

data engine that is able to pull in insights for things like the right color

for the text on the screen, the right size of font, the number of words that

should be on your screen, the fact that videos about dogs have three times

longer watch time than videos around cats. So, the editorial team can say maybe

that dog video should be three and a half minutes but maybe that cat videos

should just be two or something along those lines. You’re able to really start

to use these signals to inform your storytelling.

Michelle Manafy: So,

what’s your growth plan?

Christa Carone: Our business is really becoming much

more analogous to a TV buy. What I mean by that is that we have access to sell

all of the pre-roll against all of Group Nine content across all of the major

platforms. So, you have a television commercial and you are in, say, an auto

company and the pet owner is really interesting to you. You can come to us and

have 100 percent share of voice across all Dodo content on Facebook, on

Twitter, YouTube, Snapchat. You can buy our pre-roll on our channels and

transact that directly through Group Nine instead of the platforms. Brands are

responsive to it because of the importance of brand safety. When you have the

brand safety conversation with a marketer, you need to be able to say here’s

the right audience and it is against premium, brand safe content. It’s

fascinating to me that we’re having more conversations with TV buyers who are

shifting that investment from linear to wherever they can get eyeballs.

Michelle Manafy: I’m finding the distinction between television and all digital video is increasingly blurred, particularly for buyers.

Christa Carone: Completely. I think we have to redefine

what TV means. So, TV is not a device anymore. When the linear players, the

cable players start talking about TV everywhere, we’re in that boat. It

includes YouTube, it can arguably be IGTV, it could be lean-back viewing on

Facebook… It can be TikTok. How define TV going forward is going to be interesting.

Michelle Manafy: Talk to me about how you’re

innovating and how the industry needs to innovate.

Christa Carone: Maybe for some media companies,

diversification is innovative. It’s different at Group Nine because we were

born that way. We’ve learned so much from how past companies have run that we

know what we need to do as a media company. I feel like innovation is really

coming through how companies are able to scale intellectual property.

Michelle Manafy: Your background is marketing. How does that impact your leadership and view of your organization?

Christa Carone: I mean that’s been such an advantage

coming into a company like Group Nine. What I’m able to tap into is the

perspective of a marketer and think of everything we’re doing from the

perspective of the client. Will an advertiser really buy into this? I come from

companies with significant brand equity so I’m a massive believer in

intellectual property and that’s what appeals to me about Group Nine. these

aren’t four media companies. These are four brands. So: How can we look at

building brand equity that isn’t just about one particular revenue stream? That

has been super helpful to me to bring more of an innovative marketing approach

to building brands.

C-3PO as a nightly news anchor? Alexa winning a Pulitzer Prize? These silly scenarios sound like the stuff of science-fiction. But the reality is that automation, which often takes the form of artificial intelligence and machine learning, is increasingly infiltrating the fourth estate and impacting how media companies gather, report, deliver, and even monetize the news.

From transcribing to fact-checking and polling to tweet parsing, artificial intelligence has been hard at work in newsrooms for years. However, the number of organizations large and small—including giants like The Washington Post, Forbes, AP and Reuters—using AI and machine learning to compose content is on the rise. And that’s got the industry and consumers sitting up and taking notice.

Naturally—along with those in a number of fields—there are journalists worried about being replaced by automation. However, there are many who embrace these technological advancements, seeing them as useful assistants that help process and distribute the news.

“AI can help journalists cover and deliver the news more efficiently by freeing them from routine tasks, identifying patterns in data, and helping surface misinformation,” said Lisa Gibbs, the Associated Press’ director of news partnerships.

Chris Collins, senior executive editor of breaking news and markets at Bloomberg, agreed. “Technology is good at repetitive tasks and newsrooms tend to be overloaded with those. If you leverage technology to help with them, journalists can spend more time doing journalism—interviewing sources, breaking news, writing analysis and so on,” said Collins.

Success stories

Bloomberg built Cyborg, a program that extracts key info from corporate earnings reports and press releases. Bloomberg also has AI-assisted monitoring tools that rely on machine learning to filter out spam, recognize key names, and classify topics to cut through this noise and capture specific events relevant to Bloomberg’s financial audience.

“By doing that, we’re able to be more competitive

when it comes to identifying news events,” said Collins.

AP uses a similar AI resource to automate corporate

earnings articles. It also employs video transcription services that create transcripts

for its broadcast customers, saving AP’s video operations personnel precious time.

Additionally, the AP’s newsroom is beginning to focus more on how AI can help the news-gathering process itself. “We recently completed a test of event detection tools, such as from SAM, which uses algorithms to scan social media platforms and alert editors when it has identified likely news events,” said Gibbs. “What we found is that using SAM, in fact, does help our journalists around the world discover breaking news before we otherwise would have known.”

Reg Chua, COO of Reuters Editorial, said his organization has been using AI for several years. “A lot of it is your basic automation stuff like scraping websites and pulling stuff off feeds and then turning them into headlines published automatically or else presenting this information to humans for checking before we publish. We also employ quasi automation and technology that scans and extracts important information from documents,” said Chua.

Reuters News Tracer filters noise from social media to help discern fact from fiction and newsworthy angles from countless tweets and posts.

One of Reuters’ newest AI tools is News Tracer, which filters noise from social media to help discern fact from fiction and newsworthy angles from countless tweets and posts. “News Tracer’s core function is to tell journalists about things they didn’t know they were looking for—to quickly find news that can be reported on,” said Chua, who added that the tool provides a newsworthiness score and a confidence score to help reporters determine what to focus on.

Big and small papers

benefit, too

RADAR (Reporters and Data and Robots), a London-based

news service, has been a trailblazer in the realm of AI-reported local news.

“We operate as a news agency with a subscriber base of UK local news publishers,” said Gary Rogers, RADAR’s editor-in-chief. “We employ six data journalists. Our reporters work largely with UK open data, seeking out stories that will be relevant and informative for local audiences. They work as any data journalist might in finding the stories, but they use software as their writing tool in order to produce many localized versions. These are distributed to local news operations all over the UK.”

Rogers noted that AI allows RADAR to achieve

a scale of story production that would not be possible by human effort alone.

“We tackle about 40 data projects each month.

Each project will yield an average of 200 to 250 localized versions of the story,”

said Rogers. “Since last autumn, we have been producing between 8,000 to 10,000

stories per month.”

Smaller community newspapers are investing in big machine learning capabilities, as well. Case in Point: Richland Source, a Mansfield, Ohio daily, uses a program called Lede AI to automate local sports reporting.

“Lede Ai writes and publishes game recaps for every high school sporting event in Ohio immediately after it finishes,” said Larry Phillips, managing editor of Richland Source. “If it’s a big game, we will send a reporter and Lede Ai writes and publishes the first draft; our journalist adds color, flavor, and flare that can only be done by being at the game. With Lede Ai, we’ve never received a complaint about inaccurate reporting, and we’ve published over 20,000 articles.”

Education and

transparency

News media professionals worry about human

obsolescence in the face of such quickly accelerating automation. Yet many believe

those concerns are premature or misguided.

“While this has been true in most industries

and may happen in media, there is a broader picture of AI’s enabling rather than

employment-destroying qualities,” Rogers said. “AI can take over repetitive and

boring tasks, which frees journalists to do more important work. It can help journalists

find stories by sifting large amounts of information. In our case, it allows our

reporters to amplify their work, write a story in the form of a template, and produce

hundreds of versions of the story for local newspapers across the UK who lack the

resources to do it themselves.”

Consider, too, said Phillips, that “AI still

can’t ask follow-up questions, can’t knock on the doors of multiple sources, work

a beat, make a follow-up call, do the shoe-leather grunt work, garner an off-the-record

comment which leads to a story angle, and certainly can’t replicate the human element,

the nuance, that encompasses the very best work in the profession.”

Even if their human resources are relatively

safe for now, news organizations have to navigate carefully through uncharted waters

when it comes to ethics around and disclosure of AI practices.

“As these technologies evolve, having standards

around transparency and best practices – such as how do we prevent bias in data

from impacting our news coverage – will be critical for the entire industry,” added

Gibbs.

Bloomberg’s Collins echoes that sentiment.

“It’s essential to understand what technology can and can’t handle. Clearly, as

with all journalism, you need judgement, best practices and processes in place to

ensure what you are writing is accurate, fast and worthwhile,” said Collins. “You

need to be transparent about how a story was produced, if it was assisted or published

using AI. In our experience, the combination of years of human journalistic experience

with technology such as AI is powerful. Obviously, the technology isn’t left to

run the newsroom. It is trained and overseen by journalists, who are learning new

skills in the process.”

Reading the tea leaves

Looking ahead, artificial intelligence will

create exciting new capabilities as well as troubling obstacles, say the pros.

“As newsrooms increasingly embrace AI, it will

help with everything from spotting breaking-news events, to finding scoops in data

to audience personalization,” said Collins.

But prepare for even more fake news fiascos.

“Distribution of so-called deepfakes, assisted by AI, is a troubling trend,” Collins cautioned. “How technology evolves to both spread and combat misinformation will be a major challenge for the industry.”

Yet Richland Source publisher Jay Allred and

others remain optimistic. “In the near-term

at the local level, I think AI will largely be used for two things. First, it will

fill the gaps on informational journalism tasks that simply are not done anymore

due to shrinking payrolls,” said Allred. “Second, it will surface insights from

public databases—finding out, for instance, how a particular city floods and where,

how many speeding tickets were issued and where throughout a state, where do the

most citations for drunk and disorderly conduct occur within a city. This will spur

and support investigative journalism that wouldn’t otherwise happen.”

When was the last time you channel-surfed to figure out what to watch?

It’s probably been a few years, right? But less than a decade ago, almost everyone watched live TV—either cable or network broadcast. Then in 2007, Netflix launched its streaming service and AppleTV was released, catalyzing a major shift in how we watch TV. Hulu and Amazon also launched streaming services, and a number of other smart TVs were released, including Roku and Amazon Fire.

The technical term for these increasingly popular services is Over The Top (OTT). With OTT, content providers distribute streaming media as a standalone product directly to viewers over the internet, in turn bypassing telecommunications, multichannel television, and broadcast television platforms that traditionally mediate such content. A recent study predicts that global streaming subscriptions will surge to 333.2 million by 2019.

This new world order will likely cause a major turn away from traditional broadcast TV.

While traditional TV providers face physical network limitations, OTT opens the door to reach a global audience wherever an adequate internet connection exists. This will both decentralize content recommendations and democratize content, allowing content providers to reach previously untapped markets. But it’s not without its challenges—and the traditional program menu is chief among them.

Here’s how OTT is impacting the way content providers deliver media to their customers:

Today, both providers and consumers have more content options than ever before.

Once upon a time, the only way to get to consumers was through that one pipe coming into their homes. No more. Today, there’s no longer a stranglehold on network connections, which means content providers have more delivery options than they know what to do with.

Thus, all those innovative services and content aggregation companies—like Netflix and Hulu—were born.

Open access has allowed for content aggregation companies or new content delivery companies to provide whatever content they please to massive audiences. And skyrocketing connection speeds are only intensifying this trend.

In particular, 5G—or the fifth generation of cellular mobile communications—promises faster speeds, a more stable connection, lower latency, the ability to connect even more devices to the network, as well as reduced costs and energy consumption. In terms of speed, 5G technology intends to be 10 times faster than 4G. Ever faster mobile speeds are changing what real-time means. It’s also made it easier for content providers to reach audiences.

And content providers aren’t the only ones with more options. The OTT revolution gives consumers more choices than ever, too. Instead of just subscribing to Comcast or basic cable, consumers now have access to any number of OTT services. They can also watch on multiple devices, whether it’s Apple TV, Roku, or their smartphone.

In my house, we’re heavy users of AppleTV. But we also use YouTube TV, ESPN+, and Bleacher Report (to get all my Champions League soccer matches). And HBO, of course, because we have to watch Game Of Thrones.

Traditional economic theory says that choice is always better for the consumer and will lead to pricing efficiencies. However all of these options can be more than a little overwhelming—which is something the industry needs to think about in this new OTT world order.

Content owners need a better technological solution—but there are no easy answers.

In the past, it was a big deal for the service providers to figure out how you were going to design the program menu. Even the smallest changes to the design can have a major impact on the user experience.

But what’s a user to do when there are 17 services and they need to figure out which to watch?

This is one of the biggest challenges for content owners in the OTT era. There are so many different independent streaming services people regularly use, and consumers don’t want to have to sit down and click on 17 different top menus in order to figure out what to watch.

After all, watching TV is supposed to be a relaxing experience.

As we enter this new world order, content providers need to figure out a user-friendly menu where consumers can easily toggle between streaming services. There’s no one recipe. However, one option is to have the various content services pick up on user intent/interest based on their actions in the moment. At my predictive analytics company, Liftigniter, we provide a lot of the building blocks to do this. But it’s going to require more than just some really good tech from a startup.

Rather, it’s going to require the industry to pull together to devise a solution.

Regardless of how this all shakes out, the primary goal for the user should be twofold: price efficiency and a user-friendly personalized experience. After all, the OTT revolution is all about democratization and relevance.

Publishers attempting to unlock new sources of reader revenue are understandably honing in on device usage, particularly when there are an estimated 5.1 billion unique mobile users around the world that could be paid subscribers.

Chartbeat data between May 2018 and April 15 of this year shows that mobile continues to dominate device-based engagement across the world, with between 55% and 60% of readers engaged through this channel, followed by desktop and tablet. This trend is also reflected across North America, where approximately 57% of readers prefer mobile devices to consume content.

However, simply possessing the analytics to know whether readers prefer your mobile, tablet, or desktop experience is only step one. The next and crucial step is understanding the sources of retention and churn.

Therefore, we wanted to take a closer look at the relationship between devices and subscriber behavior, specifically where subscribers most often convert or churn. From there, publishers can uncover the solutions that will improve subscriber retention rates.

Analyzing subscriber conversions by device

We began by analyzing subscriber status changes (i.e., conversions or churns) that took place across publishers in January. In order to be included in the dataset, a user* would have had to visit a site on their device at least once in the last quarter of 2018 and at least once in January.

Quick note: Why do we refer to the data population as “users”? Since we don’t track individuals across devices, it’s possible for a single person to appear multiple times in the data if they’re accessing a publisher’s site on multiple devices.

Subscriber patterns

Our findings show that while tablets have the most subscribers (as a proportion of total audience size on each device), they are also the most likely to convert, as indicated in the chart below. This is followed by desktop and mobile, suggesting on first impression that publishers should be focusing their web conversion UX efforts on tablet and desktop.

You can also see that the churn/conversion ratio is highest on mobile (which also has the greatest number of users), followed by desktop and tablet. This suggests that the mobile web subscription and/or login experiences on websites is simply not up to par with their desktop counterparts. This could potentially take the form of slow loading speeds or difficulty navigating through form fills, for instance.

What can publishers do to improve subscriber experiences?

Chartbeat’s analysis demonstrates that publishers will want to shore up their mobile UX and subscription flows, thereby improving the likelihood of subscriber conversions and retention while reducing churn. This is particularly important on mobile devices, given that those sites are now the predominant way new users experience a publisher’s website, but through which so few are being converted.

We also think it’s worth noting here that this slice of data does not include app users, which tends to be where mobile loyalists congregate. That said, we see a good opportunity for experimentation—publishers can analyze the impact of tailoring experiences towards acquisition, engagement, and conversion on the mobile web versus re-engagement and retention on the mobile app.

All publishers need to take a deep dive into new and churned subscribers over various time periods, their reading patterns by device, and whether their user journey flow would encourage, or turn off, a potential subscriber from converting. Our approach is to help publishers integrate subscriber analytics in an effort to provide a clear idea of the connections between audience engagement, loyalty, and more paying subscribers. Clearly, publishers need to develop a deeper understanding of their subscribers’ device-based usage.

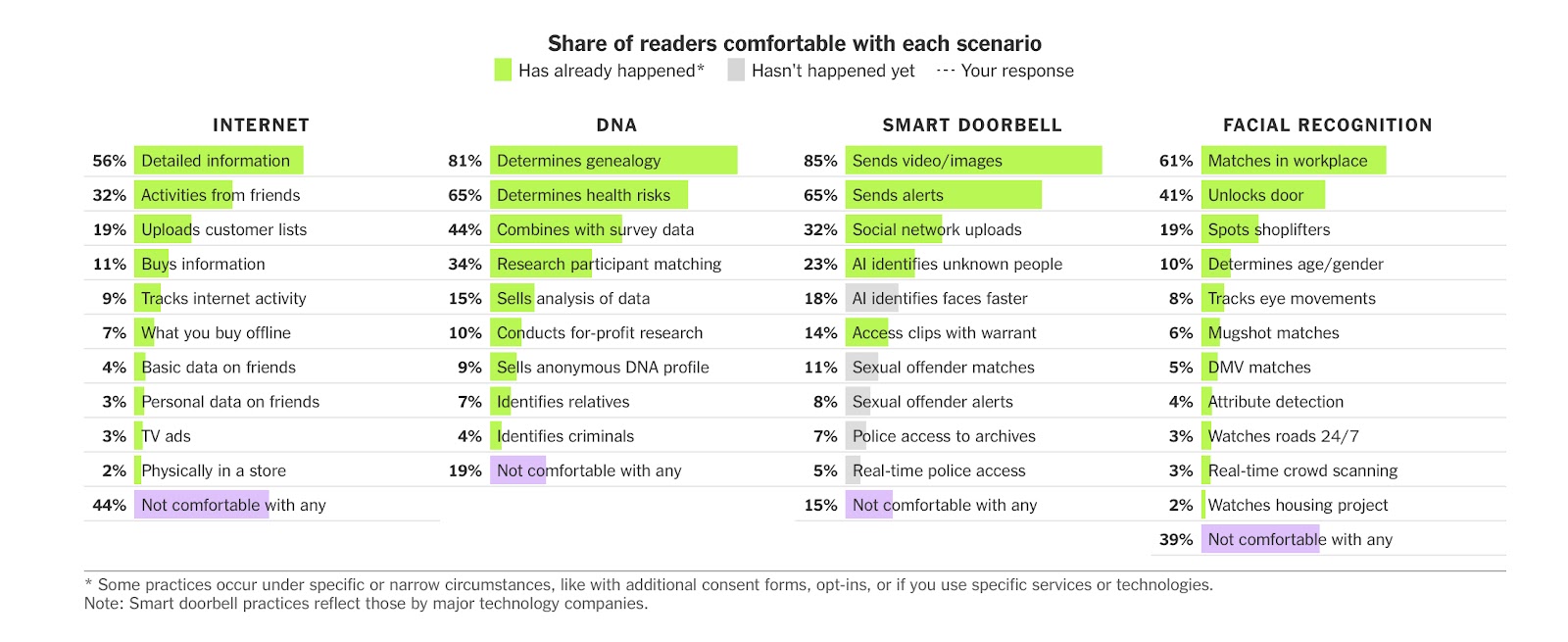

The waves of negative press about privacy intrusions and breaches are becoming a regular occurrence. Yet the outrage cycle seems to have a short lifespan and there’s confusion and a range of expectations when it comes to data collection and usage. That said, consumers need to remain vigilant about new and unexpected ways digital organizations leverage personal data collection.

Already, we face some pretty significant questions: Do you want your genealogy company to sell analysis based in your DNA? Your smart doorbell clips accessible by warrant? Mugshot-matching facial recognition capabilities?

That’s why Stuart A. Thompson, graphics director of The New York Times Opinion section, and his team set out to figure out how people report their comfort levels in terms of sharing different kinds of personal information. The work, published earlier this month, is part of the ongoing Privacy Project at the paper. It’s a series examining the different ways private groups and governments are using personal information.

Understanding the limits

Perhaps encouragingly, The Times found that consumers are taking notice of the data collection policies of the services they chose to use. But they’re not exactly excited about it when they find out. Many of the activities asked about — which were found to be outside of 90% of respondents comfort levels — are already employed by tech companies.

Readers were asked about their comfort level about the various ways companies use, or could use, personal information. Credit: New York Times.

Thomson also said that there the results offered clear take always for digital publishers. Acknowledging the reliance on third party tracking in the news site business, he explained that blind acceptance of those practices could be coming to an end. “Even if you have an airtight privacy policy that you feel ok with now, you might not feel as okay with it when people start paying attention to what you’ve done or criticizing what you’ve done,” said Thompson.

Privacy by design

Thompson said the goal of this project is to learn what was “the line” for his readers and he used a pretty clever page layout to do so. Readers scroll through increasingly intrusive privacy scenarios and then place a line over the example which they felt uncomfortable with. This skeuomorphic interaction is a technique that The Times has previously used with good results.

“Drawing things was a New York Times/Upshot trademark way to get people to interact with us,” said Thompson. “We were talking through as a group, and I think we kind of fixated on the line.”

One element Thompson wanted to address head-on was the idea that consumers continue to make privacy related decisions that aren’t in their interest, dubbed the privacy paradox.

Understanding the big picture

However, to Thompson, they’re not acting irrationally or unexplainably. People are just caught in larger systems. Individuals aren’t given real opportunity to give consent of the personal data use, such as in cases where data is required to be handed over in order to access a service, and there aren’t consumer guardrails around those practices.

With appropriate regulation, consumers shouldn’t “have to read every detail of a data policy or a privacy policy to consent to what’s happening, because you have to do that a dozen times a week,” said Thompson. “We’re not prepared for that kind of activity and we’re not very good at it.”

He added that tech companies have taken advantage of consumers’ difficulty with risk management. As a result, governments and regulatory bodies have had to enact legislation like the General Data Protection Regulation in the European Union.

The stakes get bigger

Another example of the push back against the surge in the surveillance economy was a lawsuit against the efforts by Alphabet subsidiary Sidewalk Labs in Toronto. The plan to build a smart city in the portland’s of Canada’s largest city could incorporate any number invasive new forms of data collection.

To nip that in the bud, the Canadian Civil Liberties Association launched an application to sue on the grounds that the wholesale data collection of people who just happen to be in the area aren’t allowed under the Charter of Rights and Freedoms protections including against unreasonable search and seizure. While this case is immediately relevant for the smart city project, it could help society establish a point at which it “draws the line” about privacy overall.

But at the end of the day, the path to better privacy management could start closer to home.

“As publishers are working in the public interest, maybe they have an additional responsibility to declare what they’re doing,” said Thompson. “You could argue that they are acting in this pure business sense and they have their own lines that they’re willing to to draw, [but] maybe publishers should think about what they’re comfortable with.”

The mobile app ecosystem will turn 11 years old this summer, and it has evolved into one of the largest industries globally with forecasted revenues of almost $190 billion. There are now millions of apps in both the Apple App Store and Google Play. And they account for over half of digital media usage and time spent in the US. We are obviously in a mobile-first world – at Teads, mobile traffic represents over 70% of our publishers’ traffic worldwide.

However, we find that many publishers continue to focus

investment on web while either treating their existing apps as side projects or

not developing an app presence at all. Given the rapid shift in consumer media

consumption and shift in the publisher landscape, combined with digital

dominance by the “duopoly” (and soon triopoly), the time is now for publishers

to prioritize their mobile app presence.

The Daily Beast

recently confirmed this trend, noting that their app

users average 3x more pages per session than their mobile web users. Bleacher

Report is a prime example of a publisher whose audience is primarily in-app vs.

mobile web – with its users averaging 5

minutes per day in the app. More and more editorial publishers are now

appearing among top apps, as names such as The New York Times, CNN, Bleacher

Report, The Washington Post, BBC News, and USA Today, among others, continually

rank in the top 500 apps in the US (per

comScore, July 2018).

Mobile apps > mobile web

The mobile app user experience (and native apps in

particular) is superior to mobile web for both content and advertising, which

is probably a core driver of consumer engagement in-app. Native apps are

typically faster, lighter, more interactive, and can often allow offline

content browsing. They’re also easier to access for consumers, especially if

apps are loaded on to the home screen of a smartphone.

These benefits extend to ad experiences in-app as well, where advertising growth continues to explode and expected to reach $77 billion in the US this year. Mobile app ads have evolved beyond just traditional display and rewarded videos, which are typically fueled by app-install spending.

The market has evolved to include video, outstream, and

native formats, many of which provide more innovative and interactive

experiences then web since these ads can tap into the native features of

smartphones (i.e., Bluetooth, GPS, gyroscope, camera, compass, etc.).

Measurement is also greatly improved with the IAB’s Open

Measurement SDK, which facilitates 3rd-party viewability and

verification measurement in-app, and this is poised to further accelerate

mobile app ad spending. In addition, mobile apps are relatively immune to ad

blocking which is pervasive in web environments.

Better personalized ads

Mobile app inventory for publishers could become an even more critical component of a wholistic digital ad strategy as industry concerns around data privacy escalate and tech giants clamp down on tracking and personalization in browser environments. Apple’s ITP (Intelligent Tracking Prevention) in Safari and Mozilla’s Firefox browsers have placed significant limitations on cookie usage and hence programmatic ads on mobile web. And Google is rumored to be evaluating similar restrictions in Chrome, which would then effect the majority share of mobile web browsers.

Mobile apps represent both a hedge against these limitations

and a superior environment for personalized advertising. In-app ad targeting

can leverage Device IDs, which are tied to specific users rather than browsers,

as well as more accurate location (GPS) and detailed demographic/behavioral

data (particularly if the app requires registration).

Revenue diversification

Ultimately, mobile apps provide a new path for publishers to diversify their revenue streams. Not only do apps provide more opportunities for advertising, but also a channel for subscriptions, in-app purchases, e-commerce, etc. In-app subscriptions actually fueled growth in consumer spending in non-gaming apps by 120% since 2016. App stores also provide an easy way for engaged audiences (which are generally more prevalent in-app than web) to subscribe and make payments for transactions.

It’s time for publishers to start investing in mobile apps,

which should no longer be an after-thought. While mobile app development and

maintenance is not an easy task for many publishers, it should be considered an

integral part of long-term digital strategy and a major growth driver. A

successful transition of web users to app users can result in significant increases

in loyalty and engagement, leading to new revenue opportunities while defending

publishers against threats in a rapidly changing digital landscape. Mobile apps

are no longer just a game (pun intended).

The cord-cutter’s dream of paying less for entertainment content is already on the rocks. Early analyst warnings about the reality of subscription saturation have filtered through to the mainstream, with a Mashable article titled ‘There are officially too many damn video streaming services’ reaching the front page of reddit. In it, Mashable’s Senior Tech Correspondent Raymond Wong argues that while Disney’s annual $69.99 fee is probably worth it for access to Disney’s vast stock of content from Marvel, Pixar, Fox etc., the arrival of yet another challenger to Netflix’s streaming dominance may ultimately be bad for the consumer.

“$14.99 for HBO, $10.99 for Showtime, $9.99 for Cinemax and $8.99 for Starz all feel expensive relative to Disney’s $6.99 price” ???https://t.co/6hBhzlGQfR

Between Netflix, Hulu, Disney+, Amazon Video, CBS All Access, the upcoming Apple TV+ and any number of other services, it’s easy to see why. Each has exclusive content across a wide variety of genres, so in theory each at least have one or two shows of interest to most audiences. It’s the ice cream stall dilemma on a larger scale: A huge amount of choice, but actually picking one feels more like denying yourself access to every other service.

How much is too much?

So, to get access to all those films and shows would require a number of subscriptions, the total cost of which will run into the hundreds of dollars per month. Small wonder that redditors pushed the Mashable article to the front page; the promise of cheaper, unbundled OTT entertainment is now in doubt. Subscription saturation is already here, and there will be casualties. Even Netflix has already borne the brunt of Disney’s entrance into the space, having lost as much as $8 billion off its market cap in the aftermath of the announcement.

To compound the problem, it’s highly unlikely that the number of streaming services has capped out. For media companies with huge back catalogues of film and television shows, it is far better to own the distribution system, audience data, and direct revenue. So, expect more efforts like The Criterion Channel to launch. Meanwhile, to differentiate themselves from the giants like Netflix and Amazon, smaller streaming platforms like Shudder are making a play for niche audiences clustered around a particular genre.

Hulu is embracing that fact that, with so much competition, people are probably going to jump around between video services. It’s just trying to keep them coming back to Hulu. https://t.co/cjAgrDuFtH

However, while people are more habituated to pay for entertainment content than digital news, there is still a finite amount of subscription revenue out there. More than any consideration, the exclusive content available on a streaming service will be a deciding factor for audiences. That does not mean, however, that the broadest range of films and shows will necessarily win out.

The lure of a new show is what typically attracts subscribers to a streaming service in the first place. CBS All Access made the exclusivity of shows like Star Trek: Discovery the tentpole of its marketing. It even went so far as to commission some short episodes between the first and second seasons to convince subscribers who might have been tempted elsewhere to remain with them.

Similarly the announcement of Apple TV+ notably contained no information about pricing. However, it did showcase the triple-A nature of its commissioned shows and movies, with names like Steven Spielberg, J.J. Abrams, Oprah Winfrey, Jennifer Aniston, and Kumail Nanjiani already on board.

Originals approach

Netflix, wary of the media companies whose content is has licensed until now pulling their content, is also heavily investing in originals. It is reportedly spending $15 billion in 2019 on content, with a commensurate increase in its marketing budget so that everybody knows about it. Analysts expect a close to $3 billion marketing budget this year. It is obvious, then, that the range of content each platform has is currently seen as the differentiating factor for the bigger players in the space.

(This issue is muddied slightly by content considerations, with some US ‘exclusives’ being carried by competitors internationally as with Star Trek: Discovery appearing on Netflix elsewhere, and the requirement for streaming services to create a proportion of their content domestically when they enter a market like France.)

As mentioned earlier, however, there are some services that are making their niche nature the selling point to consumers, trading less mass-market appeal for a more targeted approach to exclusives. Horror-based service Shudder (owned and operated by AMC) has both negotiated the exclusive rights to certain horror movies and commissioned original content, while DC Comics’ VOD service (currently only available within the US) offers access to shows based around popular characters from the comics.

These services, with lower price points, are wisely trying to avoid the crush at the top by offering services that are additive to the larger services rather than in direct competition.

However, as the field becomes more crowded, it is unlikely that content alone will be the sole deciding factor for audiences looking to optimise their subscription spending.

Here, then are three criteria that might help determine which of the current services will be among those counted as ‘winners’:

User experience

Much has already been written about the discovery and recommendation options offered by Netflix, Amazon Video, and their ilk. Between the wealth of user data to which they have access and some smart people at the helm, those services have made user experience as smooth and effective as is possible. In April 2017, UX expert Justin Ramedia wrote:

“Netflix, through an easy-to-use interface, showed us how simple watching entertainment through the internet could be. They used strategic partnerships with Nintendo, Xbox, Roku, Amazon and more to ensure that people didn’t have to watch from their computers. Anyone could sit with their friends and family and stream thousands of hours of media whenever they liked. That genie won’t go back into the bottle.”

One of the criticisms that was most frequently levelled against The Criterion Channel’s defunct predecessor FilmStruck was that its UX was lacking. While in the UK, VOD services like the ITV Player and the BBC’s iPlayer are serviceable lack some of the recommendation tools that have been instrumental in making sure that users stay glued to Netflix even after the whole series has been binged.

The reality is that as newer entrants into the market begin offering exclusive content, they will inevitably be measured against the best in the environment. In order to succeed they’ll need to be as good or better to compete, as we’ll discuss later.

Platform availability

As Ramedia pointed out, Netflix made it a point to have a presence on each and every possible platform, from desktops to connected televisions to games consoles, including the shockingly poorly selling Wii U. Now, Disney appears to be following suit: Its announcement included a slide that showed each piece of tech hardware it intends the service to run on.

— What’s On Disney Plus (@disneyplusnews) April 11, 2019

The point about existing across all these platforms isn’t that those streaming services believe they’ll necessarily get tons of sign-ups through those platforms or even because they exist on them. After all, the install base of the Nintendo Switch, while impressive for a relatively young console, is far smaller than the number of people who will sign up on desktop or connected TV. Instead, it is primarily in service of providing a holistic service to their subscribers, ensuring that they always have access to one particular streaming service on each and every device they own.

As with UX, the idea is to reduce any possible friction for a subscriber base, to ensure that no competitor gets a look-in or advantage from existing on a device that Disney+ does not. And as another plus for us Switch owners, it all but guarantees that Netflix will join Hulu on the console sooner rather than later.

Entrenchment

For many, Netflix’s early entrance into the market all but guarantees it success. It is the go-to comparison when we talk about rival streaming services, and its ubiquity has led to ‘Netflix-like’ comparisons for other digital services. Its entrenchment in the market is primarily due to the early mover advantage it has enjoyed, of which the service is keenly aware. As its competitors gear themselves up to compete in terms of content, Netflix appears to be digging itself in deeper by prioritising maintaining market share above profit. As Variety’s Todd Spangler reports:

“One reason Netflix is continuing to make big investments now is that it’s going to face serious new streaming competition from media giants Disney, WarnerMedia and NBCUniversal starting later this year. So it’s focusing on building out a wider moat instead of delivering profits, a strategy Wall Street continues to praise.”

That makes it an uphill struggle for any new entrant into the market. This is the case even for those without the deep pockets of Amazon, Apple or Disney who can gradually chip away at Netflix’s 139 million global subscribers through offering lower price points or a greater back catalogue.

Despite the ongoing success of the larger streaming services, growing consumer dissatisfaction with the total cost of subscriptions and a soft cap on the amount people can afford to pay means competition is only going to get fiercer over the next few years. And as the dismal performance of YouTube Red (now Premium) demonstrates, investment in original content alone is unlikely to be the sole differentiating factor. Instead, a combination of the other three criteria and harder to measure qualities including audience affinity with a brand are likely to be the determining factor for success in the streaming world.