About a third of

households are likely to adopt a vMVPD service within the

next year according to Parks

Associates research service OTT Video Market

Tracker, which analyzes the impact of new and existing video services

in the OTT space. Pluto TV, Crackle, and The Roku Channel are

the leading ad-supported OTT options, though Parks finds that no single service

currently dominates the vMVPD market.

Parks latest report finds that one-third of broadband households have trialed an OTT subscription service in the past six months. The good news is that two-thirds of those trialing OTT services subscribe to one or more of the services that they test.

That said, this is competitive market filled

with an ever-growing number of choices. Thus, Parks finds that churn is “particularly

intense in the pay-TV sector.” They

advise that “building a strong customer base over time and continuing to serve its

needs through content” is the best way to prevent churn. Netflix, Amazon, and

Hulu have substantially lower churn rates than less-established OTT players.

However, they point out that, particularly where differentiation is limited (as

in vMVPDs), tenure in the market may not be enough to produce loyalty.

Parks also finds

that:

Given

that vMVPD services are relatively new, service churn is high as consumers test

the different options available. Significant subscriber losses by DIRECTV Now

(AT&T TV Now) contribute to this figure.

A

preference by some consumers for pay TV, service contracts, bundling discounts,

and the hassle of switching providers all contribute to lower annual churn

rates for pay-TV providers compared with OTT or vMVPD services.

The

Pay-TVchurn figure for Q3 2018 includes all pay-TV services, including both

traditional and vMVPD.

OTT services are increasingly moving beyond customer acquisition as they seek to build a sustainable customer base. The upcoming market entry of Disney+, Apple TV+, HBO Max, and NBC’s Peacock (among others) has caused many industry players to reassess their approach to retention and consumers’ interest in subscribing to multiple streaming services.

By better understanding consumer attitudes, motivations, and

habits related to churn, service providers can more effectively create service

experiences will reduce churn and create a loyal customer base.

Cooking and watching TV: it’s a culinary combination that’s been a

staple of the small screen since Philip Harben whipped up a batch of lobster

vol-au-vents for BBC viewers way back in 1946 (look it up, kids). But try asking Harben to remind you how

many tablespoons of olive oil he said to add to the saucepan and see how far it

gets you.

Of course, Harben died in 1970, a situation which certainly doesn’t

help the promptness of his reply. But to be fair, even when he was still

with us, his program (Cookery) offered little in the way of

interactivity.

Needless to say, digital offers a buffet of opportunities to

enhance how-to experiences like cooking. And, with its multiplatform,

entertaining, and interactive approach, Discovery Inc.’s Food Network Cooking

app aims to take cooking shows to a whole new level.

“I remember watching Julia Child on WGBH in Boston when I was

growing up. Back then, unless your living room TV was near the kitchen or you

actually had a small TV in your kitchen, you couldn’t actually make it

along with her,” said Tim McElreath, Discovery, Inc’s Senior Product Manager of

Emerging Platforms. “Now you can just bring your iPad or Fire tablet or your

Echo show over to your kitchen counter.”

Launched in October 2019, Food Network Kitchen provides on-demand

cooking classes, which incorporate an option for online grocery shopping to secure

all the right ingredients. However, the strategy doesn’t stop there. Food

Network Kitchen also offers interactive cooking instruction with some of the

biggest names in culinary television across a wide range of platforms.

Live and lively

“Right now, we’re doing up to 10 live broadcasts a day out of New

York and Los Angeles. We’re also doing more and more on-location broadcasts,”

said McElreath. “So, we’ll have, say, Bobby Flay up in Chelsea Market on a

Sunday demonstrating how to make a chorizo omelet or something like that. He’ll

walk you through and try to do it at a pace so that you can cook along. And if

you’re watching on a mobile, you can type in a question. It’ll get relayed to

the chef by a monitor and then they’ll answer you. Or if they can’t answer it, someone

will answer it for you. So your question will get answered.”

“What we’ve seen is that our talent really starts to shine in a

live context. They’re great at producing polished scripted programming. But if you

get somebody like Michael Simon in front of the camera, talking

extemporaneously… He’s just a great raconteur. He can just talk your ear off

while he’s cooking. He’ll talk about his experiences, he’ll talk about his

family, he likes to talk about how his dad taught him to cook.”

Sometimes the questions submitted during a live broadcast aren’t about

the recipe being made, they’re about the chef and their experiences and how

they learned to cook. These kinds of questions are also welcome. “It prompts

them to start telling a little bit more about themselves.”

Demanding on-demand

Beyond the live programs, Food Network Kitchen also boasts a

library of more than 800 on-demand classes. Many of these are bundled into

courses, such as Rick Bayless’s traditional Mexican cooking course.

“We also have courses by cooking types, so we have a baking

course, a grilling course, and things like said,” said McElreath. “Each class

within a course has a recipe associated with it. But if you watch the course,

get the gist of the recipe, and then want to make it again later without

necessarily watching the whole course over again, we have regular step-by-step

text recipes that you can walk through as well.”

Listening to audio opportunities

For McElreath, the big focus with Food Network Kitchen has been to

build the smoothest possible virtual smart-screen situation for at-home chefs,

while also providing customers with a value proposition.

The approach McElreath and his team are using for the Food Network

Kitchen app – interactivity, value, and entertainment – is an extension of the

work they’d been doing on Alexa and Google Assistant.

“We’d been working on voice

platforms since early 2016, and it’d been largely kind of a research and

development type group for experimenting with the capabilities of the platform,”

said McElreath. “The voice multi-mobile platforms were so new that, across the

board, people were just kind of making things up as they went to try and figure

out how it fit in with their digital strategy. But we’d done a lot of

experimentation for things like searching for recipes and recommendations on

both the voice and the smart-screen platforms.”

Ease and extensions

For Food Network Kitchen, part of this strategy is making the app

available on Amazon Alexa and Echo Show, Fire Tablets, Fire TV streaming media devices,

and Fire TV Edition smart TVs. This gives McElreath and his team an opportunity

to integrate some of the work they’d already done while also extending the

platform out to a very specific situational interaction.

“You know, if somebody’s looking to take a cooking class, and we

have a set of ingredients, it should be very easy to get the exact ingredients

delivered very quickly,” he explained. “And since we’re on TV, Mobile, and Smart

Screen, you can watch something on TV and say, ‘Okay, I want to save the recipe

I’m watching right now,’ which shows up in your saves on Mobile while you’re

out shopping so that you’re able to use that as your shopping list, after which

you’ll go home and be able to walk right over to your kitchen counter and be

able to pull up that recipe on Smart Screen without having to search for it

again.”

Mind you, with audiences expecting such interactivity between

their devices, content companies are going to have to step up their game.

Fortunately, McElreath has already considered the many possibilities that exist

beyond the kitchen.

“We have a lot of short-form

how-to videos like how to chop an onion, how to poach an egg, and things like

that. And if we have a content template, then I think there’s a pretty big

opportunity to start thinking about applying it to some of our other Discovery

brands.”

From the boom of direct-to-consumer (DTC) brands to the introduction of new OTT streaming services such as Disney+, 2019 brought significant innovation to the digital media space. As we begin 2020, it’s time to think about which media trends will shake up the new year. Here’s what the MediaRadar team sees on the horizon.

The year of paradox for linear TV

In 2019, it was estimated that 6.4 million paid subscribers stopped paying for television. In 2020, as OTT streaming services continue to gain control, an almost equal, incremental decline in number of paid subscribers is predicted. However, despite “cord-cutting” in the TV industry, linear cable and broadcasters are poised to have a successful year. This is due in part to several major TV events set to occur throughout 2020.

The 2020 presidential election will have politicians spending significant amounts of ad dollars to get their messages across. Some estimate that spending will approach as much as $10 billion – or almost $6 billion more than the 2010 election. Advertisers are also predicted to allocate heavy ad spend towards the Tokyo Summer Olympics, as well as other large tent-pole sporting events like the Super Bowl. This year’s Super Bowl is expected to deliver strong financial results, as Fox reported in early December 2019. In fact, 80% of the inventory had already sold at a reported $5.6 million per 30 seconds. That marks a 7% jump from last year.

Amidst the evolving TV landscape, providing viewers with

real innovation will become crucial for success. Keeping that in mind, in 2020,

it’s believed that nearly all major broadcasters will either reboot or unveil

their paid streaming businesses. While this is just the start, this shows

broadcasters are committed to re-engaging with their audiences and future

proofing subscribers.

Politics’ role in digital media

An exploding ad spend isn’t the only way the presidential

election will shape the industry this year. The election is expected to take

over much of the news cycle and political ads. Every platform will be

scrutinized for accuracy more than ever before. Ahead of the election, digital

ad companies are expected to face strong public pressure to ensure their

political ad policies are tightly “buttoned up.”

Twitter recently announced they will be opting out of politics, disallowing political ads entirely. Google announced that they are restricting targeting capabilities for political ads and Facebook is predicted to follow suit, despite pressures to go further.

Based on these companies’ decisions, it’s likely that other

media will feel the same pressures in 2020. It will be up to these companies’

leadership to navigate this evolving digital landscape during the election

cycle. Foremost: an emphasis on clear and ethical business decisions.

OTT remains hot

Over the past few years, investment in the OTT space has been heavy and rapid. It shows no signs of slowing down in 2020. UBS estimates a combination of 16 media firms will spend $100 billion to produce content in 2020. Of that $100 billion, just three firms – Netflix, Disney and WarnerMedia – are projected to account for 25%, producing unique content for their viewers.

For the financial health of the companies competing in the space, it’s likely that this investment cannot last long-term. Bob Iger, Chairman and CEO of The Walt Disney Company, has acknowledged that Disney+ will probably not break even for at least the first five years. Meanwhile, AT&T has said the same of upcoming streaming platform, HBO Max.

Eventually, it’s predicted that end user prices will rise,

ad-supported models will become more common – SVOD versus AVOD – and spend on

content will decrease to ensure profitability. Being in the early days of the

streaming wars, however, the major players are willing to gamble with losses

now to gain profits later. In the fight to capture the attention, and monthly

payments of consumers around the world, and to make the investment worth it,

not all can win.

2020 outlook

2020 looks to be both an exciting and transformative year

for digital media. The TV industry will shift focus as they seek to re-engage

with audiences through paid streaming businesses and offerings. Major TV

events, specifically the 2020 presidential election and flagship sporting

events, will help sustain linear cable and broadcasters through the year.

Investment in OTT is only expected to increase, especially as “cord cutting”

continues.

Perhaps the biggest change in 2020, though, will be as a

result of the state of politics. With politics playing a larger role in the

space than ever before, media companies will begin adjusting their strategies

and policies accordingly – a change that could have a lasting impact on the

future.

It’s a big month for streaming. The launch of Apple TV+ and Disney+ are finally upon us. So it’s a good time for an update on the state of the streaming wars.

In this strange new world, tech companies like Apple are investing in content, and media companies like Disney are investing in technology. So how does? all this effort stack up? A closer look at the content and ad spend of these new OTT major players provides some insight into the future of streaming.

Content spending among new OTT services

At launch, Disney+ unsurprisingly boasts a sizable catalog of Disney-owned content. The company has also announced that $2.5 billion will be allocated to producing more original content for the platform over the next 5 years.

Conversely, Apple has opted for a small but mighty catalog. At launch AppleTV+ was armed with considerable “star power” to entice subscribers. The platform will host entirely original content exclusively available to AppleTV+ subscribers. And pre-launch advertisements reveal some of the biggest names in acting and directing.

Although these two major players bring promising new content to the OTT lineup, they will have to continuously find ways to retain value in the eyes of consumers.

Monthly subscriptions to the top seven streaming platforms will collectively cost $61. Consumers will more realistically pick and choose the platforms they actually want to pay for. These leaves companies pitching both price point and content.

Clearly, these numbers indicate that Disney and Apple are attempting to join the royalty of OTT, made up of existing streamers like Netflix, Amazon, and Hulu, which all have their own originally produced hits. With the launch of HBO Max in 2020, AT&T’s WarnerMedia may join the club soon.

With content creation underway and platforms officially launched, OTT services can now shift focus to conveying value to win the favor of consumers, who have more options than ever before. And that is where marketing and advertising come in. What does advertising an OTT option in an already crowded space look like?

Apple and Disney spend big ahead of streaming launch

For now, let’s look at the two headline makers: AppleTV+ and Disney+.

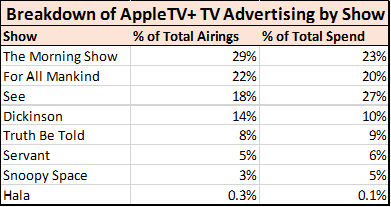

Here at MediaRadar, we found that both platforms only started running ads in late August. AppleTV+ quickly overtook not only Disney+’s ad spend, but the entire streaming space. In the month of September, AppleTV+ was the top ad spender out of all streaming platforms. This includes established players like Netflix, Hulu, and Amazon Prime Video.

To date, Apple TV+ has outspent Disney+ five times over on paid media. What’s more, AppleTV+ has not slowed their efforts now that the platform has launched. Ten days into November, AppleTV+ is on pace to once again be the top ad buyer out of all the streaming platforms this month.

The two companies differ in strategy, as well. Disney has promoted its new streaming platform as a whole, using clips from owned content to pitch the breadth of the platform. While Apple has been promoting its original content in stand-alone spots. So far, it has focused ad spend around eight shows in particular.

AppleTV+ may be outspending Disney+ on paid media. However, that does not mean Disney’s marketing push has been insignificant in any way. In fact, Disney has been orchestrating a massive marketing push using all of their various channels.

This push includes everything from on-air endorsements from Tom Bergeron (host of “Dancing With the Stars” on the Disney owned ABC network), to billboard and bus ads around Disney’s theme parks, to QR codes on lanyards worn by Disney’s 7,000+ retail workers at various Disney store locations. In one of the more interesting moves, Disney posted a video on YouTube titled “Basically Everything Coming to Disney+”, using snippets of movies available on the platform. The video was over 3 hours long.

On top of this, Disney has rolled out packaged deal after packaged deal thanks to its extensive holdings and powerful partnerships. For example: Verizon announced a year of free Disney+ for both new and existing customers, and more impressively Disney announced a $12.99 bundle with Disney+, ESPN and Hulu (both of which are majority-owned and controlled by house mouse). Visa card holders who have a Disney branded credit card can even lock in a discounted price for 2 or 3 years. Apple, for its part, is including a year subscription to Apple TV+ with the purchase of any Apple product.

Apple is almost on the defensive in this new world, playing as a tech company against media giants like Disney. No one says the best movies come from Apple today. They have a real deficiency in terms of changing perception that they are a place where you should go to watch your content.

In a bid to make that case, Apple has spent $20 million advertising its two biggest shows ahead of the launch.

In contrast, Disney’s robust offerings, combined with constant messaging across Disney properties, may immediately drive Disney+ to the top. “Think of Disney like a giant pinball machine, with content and initiatives pinging between divisions in an effort to drive up the ultimate score,” Gene Del Vecchio, a marketing professor at USC, told The New York Times.

With all this activity from the new platforms, and platforms like HBO Max and Peacock yet to join the fray, the streaming wars are heating up. It will certainly be interesting to watch how these companies market themselves as they fight for subscribers who will have many providers to choose from.

OTT players and channels are changing faster than the seasons. The spring will bring a crop of new streaming entrants, joining an already crowded market. Still dominated by Netflix, a growing number of major players are drawing video viewers.

In the publishing industry, a remarkable level of transformation is happening by way of mergers that are driven, in part, by capacity to produce video. Recently, Vox Media and New York Media joined forces. This followed close on the heels of the recent tie ups of Group Nine Media and PopSugar along with Vice Media and Refinery29. An underlying theme is upping the production of quality video programming for seeking OTT platforms and rising streaming channels battling for subscribers. So, the question is: How will consumers be watching?

Get SmartTV

The answer is on a Smart TV—whether a Vizio with WatchFree powered by Pluto TV or an LG with LG Channels powered by Xumo—the CTV universe is made up of a growing number of streaming channels (or so-called FAST services). Now, major OTT platforms are following suit with Fire TV’s IMDb TV and Roku’s The Roku Channel.

In this dynamic, programming from media companies is produced in a seller’s market as FAST services look to differentiate with new and, if possible, exclusive content. The goal is to set themselves apart from aggregated CTV ad budgets. The result is that programming is starting to be distributed on 24/7 streaming channels (like the advent of cable news). The end game is to develop an audience that can be channeled to an owned and operated network/app.

Streaming channels that take form of the lean back TV world are also coming over-the-top via leading cable/MVPD companies. For example, Spectrum recently released a skinny bundle that allows viewers to choose what they actually want to watch. And that’s for approximately the same price as an SVOD service like Netflix. The skinny bundle is trending.

Netflix vs. niche

So, here we are. We find ourselves at an interesting intersection of an on-demand world (with active content discovery and viewing) and a programmed channel world with passive watching of round-the-clock streaming content. The king of OTT and SVOD, Netflix, is ad-free. It also set a high bar with premium content licensing and quality original shows as it outspends the competition.

However, we see an emerging universe fueled by

advertising/AVOD and channels that run 24/7 content of essentially any genre of

choice as an expanding orbit of media publishers become producers of OTT

programming. On the sidelines, streaming

sports and leagues are expanding their own OTT plus channels. This delivers

their content straight to fans or through digital upstarts that make sports the

core of their offerings, like Fubo and DAZN.

The best of the bunch

The pendulum is going to swing in a direction that improves the TV experience the most. At the heart of it all is content discovery and recommendation. The next show you’re going to watch is still the biggest unknown. According to the State of Viewing and Streaming study released by Horowitz Research last year, just over one-third (36%) of viewers consider personalized recommendation algorithms helpful in discovering shows. Whereas TV ads, word-of-mouth, and social media are attributed with 35%, 34% and 26%, respectively in frequency of new discovery. The better the content recommendation, the more that will be watched on-demand.

From there, the more

“connected” your TV experience, the more it will look like a digital network

versus a TV network. It will become a more social and shareable experience. The

advertising that puts the A in AVOD will increase in value as it becomes more

data driven complying with user privacy and better in targeting viewers. The

better the social integration, the more that will be watched on constant programmed

channels.

The lessons have been learned

by media companies is that they must maintain their own brand and operated

environments in the world of platforms. However, they must continue to

experiment with publishing channels to direct audiences and own distribution (and

monetization). In the grand experiment of OTT programming, content is being

produced and distributed in 24/7 streams to start up on platforms that garner

the greatest audience for the brand. The future of OTT is here, flipping your

favorite channel.

Digital Content Next (DCN) has released findings from its new research, DCN Digital Subscription Economy*, that indicate a healthy and rapidly-growing digital subscription marketplace. The DCN study surveyed 1,000 U.S. consumers regarding the array of direct-to-consumer paid digital subscription offerings across numerous media sectors and genre.

On average, digital media subscribers are paying for more

than four unique subscription services. And two-thirds of subscribers (64%)

perceive high value in connection with their subscription(s). Consumer value is

high no matter how much they spend, how many services they have or how much

they earn.

The market is transitioning with several big-brand entrants like

Disney+, Apple TV+ and HBO Max joining the booming marketplace. However, it

doesn’t appear that consumers are anywhere near reaching a tipping point of

“too much” spending or “too many” services.

Streaming subscription value is driven more by video

streaming services than by live TV streaming, digital audio or digital print

subscriptions. This is fueled, in part, by big-budget original productions,

significant media publicity, “must have” status and consumer’s

attraction to bingeing content.

Value also appears to be driven more by consumers enjoying

the ability to choose from among a variety of streaming services than by desire

to shed their cable service. For those who continue to subscribe to cable,

their driving reason is that they’ve always had it and are “used to it.”

Subscription spending

A majority of digital media subscribers are not immediately

sure how much they spend on their digital subscriptions each month. This is

another indicator that they have not yet reached a sense of over-spending. When

asked to think about and to calculate their monthly spend, their $54/month

average expense suggests a willingness to add to their news and entertainment budget.

In other words, pricing of many of the most popular digital streaming

subscriptions – particularly video subscriptions – seems to be perceived as

reasonable and affordable, at least for the time being.

Drivers of subscriptions

Across the board, subscribers of all digital media types (video, audio, print) prize their control(direct, personalized, anywhere/anytime access) above everything else. Propensity for show bingeing, a manifestation of control, also means consumers are frustrated when complete seasons of what they want to watch aren’t available. Content discovery appears to be a non-issue with just one-quarter of video streamers (28%) reporting difficulty with discovering video content worthwhile to view.

DCN will continue to track this dynamic and shifting marketplace of digital assets consumed à la carte to provide publishers with insight into the dimensions of consumer value and to help inform their subscription strategies, offerings and messaging.

* An abridged version of the findings from the DCN Digital Subscription Economy Study is accessible to the public. Please note the full 48-page DCN Digital Subscription Economy Study is only available to DCN members. If you are a DCN publisher member, please be sure to log in or register to access this special members-only research, which will appear below this notice once you have logged in.

Digital video in 2019 looks like digital content at the dawn of the information superhighway when it started to be commercialized in formative ways. With booming audiences for streaming video, new OTT video services are gearing up to ‘party like it’s 1999’. While the industry has been overshadowed by Netflix for quite some time, a slew of new “Princes” is making their presence known, including Disney, WarnerMedia, and NBCUniversal.

The OTT service establishment today—spearheaded by Netflix along with Amazon, Hulu, and Apple—spend a staggering $20 Billion plus dollars annually on original content. At the same time, up and comers like Pluto TV are trying to replicate the success of traditional TV over the Internet. And, under the ownership of Viacom, they’ve started to stream premium original content in a channel lineup that now includes BET, Comedy Central, MTV, and Nick.

On the other hand, YouTube is attempting to crossover from being a user-generated network to a general entertainment content destination. And numerous video services have emerged that cater to more niche audiences or content segments. These range from Vimeo’s traction with small business organizations like yoga studios to offerings like Lifetime Movie Club for original drama fans and Britbox for domestic fans of British programming.

The point of saturation will inevitably arrive and the number and mix of AVOD and SVOD will eventually play out. If this concerns you, remember that cable boasts thousands of channels. The digital tuner on a TiVo can access over 1,300 of them. Nationwide, without duplication, there are tens of thousands of channels and over 500 premium scripted shows.

History is a

reliable predictor of the future. Looking back, linear TV grew five-fold in channels

and shows during the golden age between the 90s and early 2010s. Even so, total

viewing time increased by just 15% as monitored by TV measurement companies

like Nielsen. Ultimately, free time and content consumption are on an X-and-Y

axis.

The heaviest TV viewership comes from a core of the total TV

viewing population, which is comprised of those over 55 years old in age. However,

the median age of a viewers for newer and more tech savvy OTT platforms is just

over 30 years old. Clearly, the preferences and expectations of younger

audiences are going to shape plans for premium content offerings in the future.

Keep in mind that the proprietary premium content offerings

of services like this will be a clear differentiator. Consider the much hyped

Disney+ OTT service. In addition to boasting its deep well of animated and

family programing, Disney is also the owner of the Star Wars franchise, which

provides an intergalactic bridge to the post-millennial generation. And let’s not forget that WarnerMedia

will soon distribute the Star Wars of our time: Game of Thrones. That franchise

alone could provide the foundation for a significant OTT presence.

So, what will happen next in OTT as established and upcoming

services prepare to battle? Most likely, the future will not belong to a

handful of OTT services alone. Rather, we’ll see the proliferation of OTT

brands that cater to niches of interest and genres, as well as those providing

general TV style content offerings. These services will range widely in terms

of content and tactics and the growing OTT audience will allow them to propagate

on the Internet like TV channels did on cable.

It is less about who is going to take over OTT and more about who is going to take their audience for a great ride on the TV superhighway.

Consumer interaction on digital platforms is a key driver of

revenue for entertainment and media companies. With increasing affordability

and availability of broadband, mobile continues to be a strong contributor to the

growth of this segment. However, according to the new PwC’s

Global Entertainment & Media Outlook 2019–2023 Report, further

innovation and personalization will significantly change how we access and use the

Internet.

PwC predicts that creative new offerings and business models will increasingly revolve around people’s personal preferences. New applications will involve artificial intelligence in combination with digital assistants. Media companies will strive to build products that empower consumers to set their individual preferences and curate their own context.

The PwC Outlook Report cites personalization as a central theme in overall entertainment and media revenue growth. Global spending is expected to rise 4.3% over the next five years, with revenues hitting $2.6 trillion in 2023. The report provides a strong and notable resource for revenue estimates in the both the US and global markets.I

Additional forecasts from PwC’s Outlook Report include:

Subscription TV revenue in the U.S. will experience a 2.9% CAGR (compound annual growth rate) decline to from $94.6 billion in 2018 to $81.8 billion in 2023. Much of the loss comes from cord-cutting and SVOD competition. Interestingly, the US remains the biggest Pay-TV market accounting for 46% of the total global revenue in 2018.

SVOD’s continues its popularity as more streaming services are introduced and unbundling continues to grow. Newcomers to the market will need to differentiate themselves to attract subscribers.

The OTT market is also dominated by the U.S., contributing to more than half (55.6%) of global OTT revenue in 2018. OTT video revenue in the US reached $14.5 billion in 2018 and is set to double by 2023.

The U.S. virtual reality (VR) market registered $934 million in revenue in 2018 and is expected to grow at a 16.6% CAGR to reach S$2 billion by 2023. Gaming remains the primary application of VR, accounting for 57.4% of total VR revenue in the US in 2018. VR video, however, will see the most growth in the forecast period, climbing at a CAGR of 22.4% to reach $861 million in 2023.

There’s an important effort in

today’s entertainment and media marketplace to meet consumers where they spend

their time and to deliver what they need wherever they are. These sorts of personalization

efforts cut across OTT, SVOD, and VR. While evolving business models around customer

behavior is far from new, the renewed focus amplifies the importance of placing

consumers at the center of the media experience.

The advance of high-speed networks and affordable data plans hasn’t only whet audience appetites for unlimited anytime, anywhere access to the content they desire. It has created ideal conditions for data-hungry streaming apps to proliferate, displacing traditional broadcast TV, and driving the meteoric growth of on-demand video. The phenomenon is global in scale, but nowhere is the impact as profound as in India, the fastest-growing video streaming market in the world. In India, on-demand entertainment services are forecast to account for more than 74% of mobile data traffic by 2020, up from 47% in 2014.

Streaming viewership is soaring, but it’s Hotstar—part of the Walt Disney entertainment empire and India’s largest premium streaming platform —that is seeing numbers climb into the stratosphere. In June Hotstar set a new global benchmark for live events. It reported a record 18.6 million users simultaneously tuned into the company’s mobile website and app to watch the deciding game of the Indian Premier League (IPL) cricket games. This sort of high-octane content has allowed Hotstar to grow the number of monthly users across app and web to 300 million, up from 150 million the previous year.

Hotstar balances a mix of blockbuster entertainment (including rights to popular movies and shows from ABC, HBO, and Showtime) with a bouquet of content aligned with India’s obsession with Bollywood and demand for local language translations. (Note that India hosts hundreds of dialects and over 20 official languages). As a result of this winning combination, Hotstar dominates India’s on-demand video streaming services market. The latest research from Jana pegs Hotstar’s total market share at 69.7%, compared to Amazon (5%) and Netflix (1.4%).

Using data to differentiate the customer

experience

At first glance, it’s remarkable that large global players with deep pockets continue to struggle in the Indian market—despite significant investments to ramp up local content. But look under the hood, and you may be surprised. Hotstar’s success may start with broadcast rights for live premium sports paired with high-quality vernacular content that attracts record numbers of viewers. However, it’s driven by a strategy that harnesses personalization, recommendations, and psychographic segmentation to keep them coming back.

Finding

the right balance between acquisition and retention is crucial for a company

like Hotstar, which thrives on live events. It pays to spend millions of

dollars to acquire audiences at scale—but only if users don’t leave in droves

when the event is over. Hotstar turned a potential problem into a massive

opportunity by mapping individual user journeys to move audiences across the

funnel from freemium viewers to paid subscribers.

How

Hotstar moves viewers from fremium to subscription

In an

exclusive interview, Mihir Shah, VP of Product & Marketing Growth at

Hotstar, distills the company’s data-driven approach into the four fundamentals

companies must get right to turn casual users into committed fans.

1. Personalize the entire user experience

It’s

important to look beyond demographics to gain a deeper understanding of who

your user is, what job your product solves in their lives, and how they use

your product, Shah explains. In this scenario, actions are just as important as

inactions to develop relevant engagement and re-engagement strategies. How many

times has the user opened the app or viewed the content? How long has it been

since the last interaction? How quickly or slowly is the user moving through

the funnel, and what“nudges” might convince and—ultimately—convert them?

Shah says these are critical questions marketers can only answer if they get a

firm grasp of behavioral segmentation models aimed at understanding and

predicting user attitudes and outcomes. “Once you establish a degree of

predictability around how your users behave, the way is clear to progress users

through the funnel with the help of content that is packaged and promoted based

on a deep understanding of user personas and psychographics,” he says

2. Recommend your content along the customer

lifecycle

User

acquisition burns money if audiences don’t stick around to explore and consume

the breadth of content available on the platform. This can be a major marketing

challenge, and why a big part of Shah’s job revolves around “converting the

sports fans who come to our platform—about 70 to 80 million daily for live

events like IPL—to start watching more of the entertainment we offer. And,

ultimately, get them to commit to a subscription.”

Achieving

this objective requires the ability to identify and segment users based on

digital details, including their browsing and viewing history, content

consumption patterns and other preferences. “Based on a collaborative filtering

method, we recommend entertainment titles that other sports viewers watch,”

Shah says. “If the user is a free user on our platform, we move them through

the funnel by recommending content from our Premium library that they are most

likely to appreciate—content suggestions based on freemium viewership patterns.

The relevant recommendations are then delivered to users off-platform as part

of an omnichannel campaign strategy that spans push notifications, social and

programmatic.

3. Messaging must be personal and perfectly

timed

Keep

up the momentum with campaigns that seek to influence user behaviors, not just

move metrics. Shah illustrates using the example of users who have streamed

live cricket matches. “We know that sending them push notifications based on

the actual game event will encourage them to relaunch the app and view the game

in progress.” In practice, he says, this means “delivering over 100 million

push notifications tailored to the moment and timed perfectly within a very

small window of just a few minutes.”

It’s a critical timeline that Shah says Hotstar reaches with the help of CleverTap, a customer lifecycle management and engagement platform that is capable of delivering more than 25 million push notifications a minute/ Shah says it was essential to reach Hotstar’s app install base of over 250 million. Significantly, “event-centric” campaigns appear to resonate most with audiences, boosting engagement and the average watch time per session by 12% and more.

“As we

cross-sell entertainment content, let’s say a movie, to our sports viewers, our

marketing creatives bring out a connection between the sport and the

entertainment content, thus making the content more appealing to a sports fan.”

But making the connection is just part of the strategy. Shah stresses it’s also

a good idea to pinpoint the days and times of the week that different user

segments are the most active and receptive to push notifications. Hotstar used

these insights to optimize send times, increasing click-through rates by 3x in

the process.

4.

Engaging with users in real-time is a game-changer

RFM

(Recency, Frequency Monetary) analysis is a behavioral segmentation model that

examines user activity to identify how recently and frequently they performed a

key action. To make sure the effort marketers invest in this model also drives

returns, RFM also looks at the monetary value of the action (such as purchasing

an item or, in the case of Hotstar, subscribing to programming). Shah is a huge

proponent of RFM, a framework his company has harnessed to bring context to

user engagement campaigns and, more importantly, predict churn. In both cases,

Hotstar segments users in real-time based on certain actions or inactions they

undertake within the app.

Imagine

a scenario where users who were watching a particular episode of a series

simply leave the app for some reason. “We see that as a trigger and send them a

customized push notification encouraging them to come back to finish viewing

that particular episode at precisely that moment.” Similarly, users who have seen previous episodes of

a series but not the latest one, are sent a contextual push notification as

soon as the latest episode is released. The outcome, he adds, is “more

conversions and increased content consumption.”

The future is interactive

As Hotstar continues on its impressive

growth trajectory, Shah says, the company is ready to take on one more bet:

that “the future of all sports streaming will be social.” As he sees it,

there’s no reason to limit the flow of content to push or pull. “Why should

content consumption be one way?,” he asks. “Why can’t it be immersive and

interactive?”

To enable two-way exchange, Hotstar is

laying a new layer on top of its platform. Last year it introduced Watch`N`Play, a game that challenges

users to guess cricket gameplay and outcomes, as well as social features and

streaming using virtual reality (VR) to make the match more immersive. This

year Hotstar is going one better, adding “another layer of chat” to the

platform, allowing fans to invite their friends from their Facebook account or

phone book contacts to the platform.

Effective user acquisition ends in

advocacy, and that means meeting and anticipating needs that consumers

themselves might not be able to identify. “It’s becoming increasingly clear

that customers are hungry for more, even though they don’t know what they are

looking for,” Shah explains. It’s up to companies like Hotstar to pave the road

for this future, building a platform and adding what he calls “unique,

inevitable and incremental experiences” that go beyond just entertaining

content.

I recently connected with Christa Carone, who joined Group Nine Media as president in 2017, at the Collision Conference in Toronto, Canada. Carone, who came to the media side of the industry after leadership roles on the marketing and agency side, oversees Group Nine’s sales and marketing teams as well as its data insights group. Group Nine is a digital media holding company comprised of four popular digitally-native media brands Thrillist, The Dodo, Seeker, and NowThis. Carone and I discussed revenue and distribution diversification, content strategy, and building a business based on brand equity.

Here are some highlights from our conversation:

Michelle Manafy: Tell me a little bit about your content

distribution strategy and why you are all-in on social.

Christa Carone is President of Group Nine Media. Prior, Carone spent 17 years at Xerox Corporation, most recently serving as CMO.

Christa Carone: Well, I’d say we’re all-in on omni

channel—and that includes social. Right now, we’re distributing content on over

20 different platforms. That includes Amazon Prime, Pluto, Roku, and distribution

deals with networks literally around the world. So, our approach to being

completely agnostic on distribution is that we want to bring our content to all

of the different places where people are spending their time. And we want that

to be a pretty frictionless experience. Instead of spending a ton of money to

get you to come to my website, I want to bring our storytelling to the place

where you are already hanging out.

Michelle Manafy: Truly connecting with audiences at

scale almost sounds like almost an oxymoron to me. What do you think?

Christa Carone: You can debate that content is king

and distribution is queen and whether they have an equal seat at the table. But

that’s really kind of how I look at it. When both are working together extremely

well, you are able to build successful brands like The Dodo, NowThis, Thrillist,

and Seeker. It’s like really honing-in on higher value content. We’re building

lifetime value of the content, what’s going to keep an audience interested, and

remain totally agnostic on the distribution strategy.

Michelle Manafy: The trick, of course, is the

monetization. The other side of a distributed model is fragmentation. So, talk

to me a little bit about how managing all of those channels ties into an overarching

strategy.

Christa Carone: The beauty of our strategy is

diversification. I often say that if Facebook sneezes, we don’t want to catch a

cold. Just like in any industry, you don’t want to be overly dependent on one

particular revenue stream. It’s business 101. Media is no different than any

other type of business. So, that’s why we’ve been so focused on building

audiences across a number of different channels. We’re building audience on TikTok

right now. The monetization strategy there is nascent. But it’s going to come. IGTV

is another great example. We produce great content for IGTV and put it on IGTV

pre-revenue. But I have no doubt at all that Facebook is going to open up

monetization opportunities there. And I want to have established an audience when

it does.

Michelle Manafy: You mentioned diversification and that

every company should be focused on diversified revenue. I take it that Group

Nine that’s been baked in from the start.

Christa Carone: Keep in mind that we’re two years old. So, we’ve had the benefit of learning from a lot of traditional companies. And I often say: We’re not pivoting to anything. Some of our brands were born into video so there wasn’t a pivot to video. And the business model was already established. Some of our brands were social first. NowThis, in particular, was born as a social-first distributed brand. We didn’t pivot our business model from taking audience from owned and operated to distributing through external platforms.

Thrillist is the oldest of our brands and it has such a

loyal audience. So, we are looking at diversification around where we can take

the Thrillist brand and make it more of a whole-lifestyle brand.

Overall, our focus is on lifetime value for the content. So,

if we’re bringing in revenue with licensing, great. Bringing in revenue from

the syndication model, great. If we’re bringing in revenue by production deals

with OTT content providers, like a Netflix, that’s perfect. And if we are continuing

to bring in a healthy amount of revenue from advertising, wonderful. And increasingly

we’re thinking about how we can tap into other revenue streams like commerce and

events.

Michelle Manafy: Could you tell me a little bit about

your commerce strategy?

Christa Carone: Our approach to commerce is really looking at brands like The Dodo and Thrillist and saying there’s intellectual property here. There’s a maniacally loyal fanbase. Can we be licensing The Dodo into product? The Dodo clearly has enough brand equity to be producing large scale consumer and canine events. Thrillist has been a friend to people for a long time. It is your recommendation action for food and beverage and travel. So, our ability to take that brand equity and bring it into commerce is already built in. And stay tuned: We will definitely be doing some more on that later this year and we just hired a head of ecommerce.

Michelle Manafy: So, you mentioned that maniacal

audience, that loyal audience. What’s the Group Nine secret? Because, as

publishers, that audience relationship is what differentiates us from the

platforms.

Christa Carone: It’s such a credit to our editorial

teams. They know how weave a great narrative and tell an amazing story. It

sounds simple but I’m always amazed … A great example is from NowThis. Many

people are familiar with the NowThis video about Beto O’Rourke that went viral.

The raw footage of that video was already posted on Twitter. It already lived

on the Internet someplace. The NowThis team found it and was able to put it

through their storytelling lens. They said how can we construct it in such a

way that viewers are compelled to watch the entire piece? There is an art to

it. There is a narrative that was built in through the use of text on the

screen, through the use of effective editing so that we as the viewer were

compelled to watch it from start to finish. That is the secret sauce that

really exists within our editorial teams and applies to how we produce content

across all of our brands.

I would say the other massive factor for us is that scale

matters. We have such amazing insights that we’re able to glean from the

consumption of our videos that informs how we produce content. Based on our scale,

our data team is looking at 115,000 views of our content every minute. Every minute. We’ve built a very sophisticated

data engine that is able to pull in insights for things like the right color

for the text on the screen, the right size of font, the number of words that

should be on your screen, the fact that videos about dogs have three times

longer watch time than videos around cats. So, the editorial team can say maybe

that dog video should be three and a half minutes but maybe that cat videos

should just be two or something along those lines. You’re able to really start

to use these signals to inform your storytelling.

Michelle Manafy: So,

what’s your growth plan?

Christa Carone: Our business is really becoming much

more analogous to a TV buy. What I mean by that is that we have access to sell

all of the pre-roll against all of Group Nine content across all of the major

platforms. So, you have a television commercial and you are in, say, an auto

company and the pet owner is really interesting to you. You can come to us and

have 100 percent share of voice across all Dodo content on Facebook, on

Twitter, YouTube, Snapchat. You can buy our pre-roll on our channels and

transact that directly through Group Nine instead of the platforms. Brands are

responsive to it because of the importance of brand safety. When you have the

brand safety conversation with a marketer, you need to be able to say here’s

the right audience and it is against premium, brand safe content. It’s

fascinating to me that we’re having more conversations with TV buyers who are

shifting that investment from linear to wherever they can get eyeballs.

Michelle Manafy: I’m finding the distinction between television and all digital video is increasingly blurred, particularly for buyers.

Christa Carone: Completely. I think we have to redefine

what TV means. So, TV is not a device anymore. When the linear players, the

cable players start talking about TV everywhere, we’re in that boat. It

includes YouTube, it can arguably be IGTV, it could be lean-back viewing on

Facebook… It can be TikTok. How define TV going forward is going to be interesting.

Michelle Manafy: Talk to me about how you’re

innovating and how the industry needs to innovate.

Christa Carone: Maybe for some media companies,

diversification is innovative. It’s different at Group Nine because we were

born that way. We’ve learned so much from how past companies have run that we

know what we need to do as a media company. I feel like innovation is really

coming through how companies are able to scale intellectual property.

Michelle Manafy: Your background is marketing. How does that impact your leadership and view of your organization?

Christa Carone: I mean that’s been such an advantage

coming into a company like Group Nine. What I’m able to tap into is the

perspective of a marketer and think of everything we’re doing from the

perspective of the client. Will an advertiser really buy into this? I come from

companies with significant brand equity so I’m a massive believer in

intellectual property and that’s what appeals to me about Group Nine. these

aren’t four media companies. These are four brands. So: How can we look at

building brand equity that isn’t just about one particular revenue stream? That

has been super helpful to me to bring more of an innovative marketing approach

to building brands.

When was the last time you channel-surfed to figure out what to watch?

It’s probably been a few years, right? But less than a decade ago, almost everyone watched live TV—either cable or network broadcast. Then in 2007, Netflix launched its streaming service and AppleTV was released, catalyzing a major shift in how we watch TV. Hulu and Amazon also launched streaming services, and a number of other smart TVs were released, including Roku and Amazon Fire.

The technical term for these increasingly popular services is Over The Top (OTT). With OTT, content providers distribute streaming media as a standalone product directly to viewers over the internet, in turn bypassing telecommunications, multichannel television, and broadcast television platforms that traditionally mediate such content. A recent study predicts that global streaming subscriptions will surge to 333.2 million by 2019.

This new world order will likely cause a major turn away from traditional broadcast TV.

While traditional TV providers face physical network limitations, OTT opens the door to reach a global audience wherever an adequate internet connection exists. This will both decentralize content recommendations and democratize content, allowing content providers to reach previously untapped markets. But it’s not without its challenges—and the traditional program menu is chief among them.

Here’s how OTT is impacting the way content providers deliver media to their customers:

Today, both providers and consumers have more content options than ever before.

Once upon a time, the only way to get to consumers was through that one pipe coming into their homes. No more. Today, there’s no longer a stranglehold on network connections, which means content providers have more delivery options than they know what to do with.

Thus, all those innovative services and content aggregation companies—like Netflix and Hulu—were born.

Open access has allowed for content aggregation companies or new content delivery companies to provide whatever content they please to massive audiences. And skyrocketing connection speeds are only intensifying this trend.

In particular, 5G—or the fifth generation of cellular mobile communications—promises faster speeds, a more stable connection, lower latency, the ability to connect even more devices to the network, as well as reduced costs and energy consumption. In terms of speed, 5G technology intends to be 10 times faster than 4G. Ever faster mobile speeds are changing what real-time means. It’s also made it easier for content providers to reach audiences.

And content providers aren’t the only ones with more options. The OTT revolution gives consumers more choices than ever, too. Instead of just subscribing to Comcast or basic cable, consumers now have access to any number of OTT services. They can also watch on multiple devices, whether it’s Apple TV, Roku, or their smartphone.

In my house, we’re heavy users of AppleTV. But we also use YouTube TV, ESPN+, and Bleacher Report (to get all my Champions League soccer matches). And HBO, of course, because we have to watch Game Of Thrones.

Traditional economic theory says that choice is always better for the consumer and will lead to pricing efficiencies. However all of these options can be more than a little overwhelming—which is something the industry needs to think about in this new OTT world order.

Content owners need a better technological solution—but there are no easy answers.

In the past, it was a big deal for the service providers to figure out how you were going to design the program menu. Even the smallest changes to the design can have a major impact on the user experience.

But what’s a user to do when there are 17 services and they need to figure out which to watch?

This is one of the biggest challenges for content owners in the OTT era. There are so many different independent streaming services people regularly use, and consumers don’t want to have to sit down and click on 17 different top menus in order to figure out what to watch.

After all, watching TV is supposed to be a relaxing experience.

As we enter this new world order, content providers need to figure out a user-friendly menu where consumers can easily toggle between streaming services. There’s no one recipe. However, one option is to have the various content services pick up on user intent/interest based on their actions in the moment. At my predictive analytics company, Liftigniter, we provide a lot of the building blocks to do this. But it’s going to require more than just some really good tech from a startup.

Rather, it’s going to require the industry to pull together to devise a solution.

Regardless of how this all shakes out, the primary goal for the user should be twofold: price efficiency and a user-friendly personalized experience. After all, the OTT revolution is all about democratization and relevance.

Certain terms like “new wave,” “new school,” and “online video” start to lose their meaning over time. The same seems to be true of the “NewFronts,” now in their eighth year in New York. The showcase for traditional and digital native publishers selling their video offerings to marketers has been split up into twice-per-year affairs (with a fall showcase in L.A.). Just 16 publishers presented in New York this year, down from 36 in 2017.

The idea of the TV Upfronts and NewFronts are to dazzle

advertisers and get them to commit a chunk of their advertising to the

publisher, though there is less scarcity online. Have the NewFronts made

progress over the years? Most definitely. Has that progress meant there is no

need for them anymore? Not quite.

What’s most interesting at this year’s shindig is that

traditional players are pushing new acquisitions and initiatives, while the

digital natives are trying to sound more traditional with ongoing series. This

points to a convergence of purposes and the fact that online video, OTT,

streaming video et al have commingled

to the point of absurdity. This leaves marketers grasping at just what they’re

buying and how they can track and optimize it all. And yet there’s still a

place for publishers at the NewFronts as a showcase for offerings and to

generate much needed buzz.

Platform domination

The biggest challenge for publishers, as always, is trying to stand out from dominant players like Hulu, YouTube, and even Twitter. And the dominant players just get more dominant. YouTube casts an immense shadow as the largest ad-supported video platform online. But, as Digiday’s Sahil Patel points out, YouTube users are spending 200 million hours per day watching YouTube on a TV, up from 100 million hours last October.

And Hulu hit $1.5 billion in ad revenues last year by

offering a mix of legacy TV programming and original shows. During its

NewFronts presentation, Hulu execs pointed out that they have 26 million paid

subscribers, and a much younger audience than cable, at 31 years old vs. 53

years old. Plus, 80% of Hulu viewing takes place on a TV set, up 75% from last

year. (And Hulu even sponsored Digiday’s coverage of the NewFronts.)

This puts many publishers in a bind because

they have to sell their uniqueness to advertisers while also cutting deals with

the platforms to expand reach.

“Mass reach is still a thing,” Mediahub’s Michael Piner told

Digiday. “And there are certain partners that are being prioritized because

they can achieve the mass reach of TV.”

What do publishers get?

So what do publishers get for their money and trouble at the NewFronts now? Well, the decrease in presenters means they do get more attention from attendees. And at least one publisher, Studio71, was touting its upfront ad sales. The company has presented at the NewFronts from 2016 through this year’s edition. Studio71’s CEO Reza Izad told Digiday that 85% of their revenues each year came from upfront commitments. They boast 100 million unique viewers per month on YouTube and vet each piece of content on the network.

Still, many publishers such

as Group Nine and Refinery29 decided to forgo the NewFronts for a private tour

to increase intimacy – and likely save costs. The increased competition for

digital video ads is partly to blame, and people are also paying more for

services such as Netflix and HBO that don’t serve ads at all.

But it’s still hard to ignore the growth of digital video, especially if you sell video advertising in entertainment. The IAB’s Video Ad Spend Report surveyed marketers and found they would be spending $18 million on average this year on digital video ads, up 25% from last year, with the Media/Entertainment vertical up a whopping 75%. (And yes, that means studios are buying more ads on other media.)

Switching places

Meanwhile, notable presentations from Meredith and Conde

Nast discussed new shows for their OTT services, and Meredith is also

distributing them through its local TV stations. And as OTT moves into

broadcast, cable network Viacom was showcasing content on its newly acquired

PlutoTV OTT service.

“Viacom is embracing digital inventory, and at the same time we see Condé and Meredith pushing themselves into the OTT universe,” Wavemaker’s Noah Mallin told AdAge. “They are starting to resemble each other more and more.”

As AdAge’s Jeanine Poggi’s so astutely points out, this is

the year when the NewFronts actually looked a lot like the regular TV Upfronts,

with the themes of brand safety, original programming, and scale. “This year more publishers spoke about renewing

existing shows, creating long-form content akin to TV and

positioning themselves as the new ‘primetime,'” Poggi wrote.

So where does that leave publishers and the IAB? Perhaps the

time has come to ditch the NewFronts and merge them into the regular TV

Upfronts. More importantly, publishers need to calculate carefully the benefits

of a flashy program on stage at the NewFronts, and whether that still beats a

private tour or other marketing outreach. Ultimately, it will take a new round

of upstart video-centric publishers who want to make a splash to inject new

energy into the NewFronts.