The subscription media landscape continues to evolve, reshaping how consumers engage with digital content and how businesses strategize to maintain their market share. As digital media matures and price sensitivity increases, the market has responded with innovative pricing models and premium offerings.

The DCN Digital Media Subscription Tracking Report provides insights into these changes, offering year-over-year trends and brand-specific data exclusive to DCN members. Here are key highlights from the latest report:

Subscriptions Decline, Spending Rises: While the average household subscription count fell by 4% in Q4 2024, annual spending on digital subscriptions grew 7%, indicating a shift toward prioritizing high-value services.

Bundling Gains Popularity: 59% of SVOD subscribers opted for bundles in Q4 2024, up from 52% earlier in the year, as consumers seek value-driven solutions.

Ad-Supported Tiers Surge: Consumers increasingly choose ad-supported streaming services to cut costs. SVOD with ads saw a 14% increase, while no-ad services declined by 12%.

Top Performers in SVOD: Amazon Prime Video with ads quickly ascended to the top spot among users. Hulu with ads rose to third, Peacock with ads rose to fourth, while Disney+ Premium with no ads dropped to fifth place.

As the media subscription landscape continues to evolve, innovation in bundling and tiered options remains crucial. These findings underscore the resilience of premium digital content and the importance of staying attuned to evolving consumer needs.

DCN members can access after logging in, or registering an account (top right corner). Once logged in, a download button will appear below this text.

The Economist is an industry leader when it comes to subscriptions innovation: Last year, they paved the way in audio by paywalling all but one of their podcast portfolio. The Economist’s multi award-winning Espresso app has been used as a blueprint for other publishers looking to offer a sample of content behind a cheaper paywall. Earlier this year they also launched the largest brand campaign since the early 2000s in a bid to attract younger readers.

What binds these initiatives together is a strong consumer research team. In addition to brand building and surveying about new initiatives or products, this team is also involved in almost all aspects of the organization, from retention efforts to optimizing its growing B2B business.

The Economist’s Global Head of Consumer Research Seema Hope believes that this is a function more publishers should be seriously considering to optimize subscription efforts. There is real value to be gained in getting to know audiences on a deeper level, even for those without paywalled products.

Getting to know consumer research

Hope’s Consumer Research team is one of the few which has ongoing communication with readers. “We get a lot of dialogue through editorial; people write in,” she noted. “But that two-way conversation is where we come in, and we take that really seriously. We’re there to represent what consumers are saying, and it’s our job to be frontline and independent on that.”

The team is made up of a mixture of disciplines, from UX and design to data and research. Hope firmly believes that it is more important than ever to bring these together rather than operate in silos. “You want to make sure that you’re understanding everything about the consumer, not just the way they’re interacting with a product. You want to understand their needs and motivations,” she explained.

This does add a layer of pressure on research teams to specialize in multiple methodologies. But Hope has seen this be advantageous for careers. Her team has people who are strong in UX, qualitative research and talking to people, as well as experts in qualitative and statistical methodologies. As consumer researchers, being able to operate across all of these means that they can work more effectively with teams across the business, from product to consumer marketing. “We touch nearly every aspect of the organization. And that can only get wider,” Hope said.

An internal and external independent voice

One reason the consumer research team at The Economist is so effective is because they believe in taking stakeholders on the research journey with them. “We won’t just deliver a project and say: ‘Here you go,’” Hope said, explaining how they anticipate any resistance to findings. “We start in partnership with them, working out what the objective is, what the business challenges are. Then our job is finding the right methodology to get them to a deeper understanding.”

Most of the projects the team are involved with are “quite iterative, with constant dialogue,” so findings aren’t a surprise. Hope also outlined that her researchers are often embedded in other teams while a project is ongoing so that everything is transparent. For example, if a consumer has made a statement about user experience in a video, that video is shared with the relevant people in The Economist’s Slack channels.

This perception extends to their interactions with participants, too. “It’s really important that we’re independent when we’re talking to consumers, and we make it really clear that you’re not going to hurt anyone’s feelings [with honest feedback],” Hope said. Constant and open dialogue with customers helps, as does keeping each other’s biases in check internally, with the team ensuring they’re not asking leading questions or putting a spin on data interpretation.

Currently working on growth and retention – once customers are acquired, how do we best keep them, as well as brand perception. Also students and what loyalty means for a news org.

Uncharted territory with Podcasts+

One prominent example of the Consumer Research team’s influence was in in shaping The Economist’s Podcasts+ program. Last October, the publisher moved all but its daily The Intelligence podcast behind a paywall, offering a separate podcast subscription product.

Planning for this was a challenge as virtually no other publishers had made such a move (and still haven’t!). Many consumers will have never come across a paid-for podcast until they hit The Economist’s paywall.

The decision to charge for podcasts was one the whole company stood by. It seemed incongruous to have such a significant product available for free when nothing else was? But they had concerns about how audiences would respond. Hope’s team started with needs, behaviors and motivations. This shaped their messaging and approach.

“It was interesting the way the project evolved. Our consumers were telling us, ‘I can see why you’re doing this. You value your journalism. It’s really in-depth. It’s well-researched. It’s amazing to hear the voice of the journalists in my ear. I feel a real personal connection to this person,’” she explained. “So in the end, our consumers told us the kind of language that we should use when talking to them.”

It took months of conversations and rigorous testing before they arrived at a model that made sense for the publication, as well as one consumers would take up. The Intelligence daily podcast would remain free as a daily touchpoint. However, all other weekly and daily shows would be available for $4.90/month, or as part of the full Economist subscription package.

Hope says that there has been uptake not just of the podcast-only package, but also to the full subscription. One finding that her team were able to pick up was the perception of increased value now that the podcasts were paywalled. “Once you start charging for something, people put more of a value on it. So it’s changed that perception of quality content because they’re now paying for it, and increasing their listening,” she noted.

Now, their focus is on understanding how to move people along the funnel from free to podcast to full subscriber. Hope’s work is never done; consumer research is an ongoing dialogue as tools, technology and behaviors evolve. “I think it’s naive to think you get it right the first time. It’s naive to think that you stop learning. So we rarely say, ‘That’s the end of a project’,” she said.

Lessons from The Economist’s consumer research

Hope has had over 16 years working in audience research, and firmly believes it’s a role all publishers should have to inform decisions across the business. It’s a role that changes and evolves. “But at the very crux of it, we are, as publishers, curating and creating content for a person,” she emphasized. “If you don’t understand what they’re thinking and the why, what, who they are as people, it’s very difficult to adapt what you’re doing.”

We may have more data and insights than ever before into our audiences. But this can’t always provide the full picture about what is going on with consumers. To truly create products that audiences not only enjoy, but are willing to pay for, benefits greatly from insights that run deeper than data. For The Economist – ranked sixth most effective subscriber conversion publisher globally – having a dedicated consumer research team to get under the skin of what really makes their audience tick is clearly paying off.

Not too long ago, the consensus was that a significant digital reader revenue strategy could only work at two or three outlier news organizations. The New York Times had the breadth and depth and quality of content for which the average person highly engaged with the news might pay. The Wall Street Journal had a large potential base of readers who needed its specialized content for their jobs and who had expense accounts that would cover it.

Beleaguered regional newspapers such as the Minneapolis Star-Tribune and the Boston Globe eventually proved this wrong. Voice of San Diego and dozens of other local and national nonprofit newsrooms found they could have public radio-like success with small donations from readers who understood the altruistic mission of accountability journalism.

Beyond the business side

Local news organizations are right to pursue the formula. We’re past the debate over whether a significant number of readers will pay to support strong journalism. It’s been proven they will.

Industry leaders and journalism funders continue to put crucial focus on testing and improving revenue models. Many cohorts of local publishers have been trained in the business-side factors involved in a reader revenue strategy. Help on achieving the level of journalism that will capture an audience and move them to give or subscribe has been much harder to come by.

And that’s the elephant in the room: The media support system – the dot orgs, foundations and funding organizations – need to figure out how to help make the journalism at under-resourced newsrooms strong and impactful enough to generate the kind of support that will make them sustainable. (And ultimately lead to more such journalism.)

This isn’t a question of building a business model or fundraising. This is about staffing and data acumen and the knowledge and tools it takes to create powerful journalism and a user experience that audiences value and support.

As they long have, amazing training opportunities exist through organizations such as IRE, ONA, SPJ, the Ida B. Wells Society and more. But the barriers for small and under-resourced news organizations to actually take advantage and put that training to use are high.

Small is the new normal

Zooming out, we see a local journalism landscape dominated by hundreds of very small newsrooms: local independent online startups that are one- to three-person operations and legacy Black and brown news organizations. They have limited resources or are chain-owned daily newspapers whose staffs have been reduced to one or two reporters.

First and foremost, these newsrooms need more direct operational funding to employ more journalists. This is something that the massive Press Forward initiative created by a coalition of journalism-supporting foundations is seeking to address.

But the industry also needs to have teams equipped for the future. Newsrooms like these will benefit from a system of training, resources and mentorship to support “capital J” accountability journalism in news ecosystems that are now decentralized.

Readers are well-served and grateful for coverage of the day-to-day news of the community. However, every newsroom yearns for the space and resources to also do work that goes deeper, that holds the powerful accountable, that has impact and drives change. It’s the kind of work that elevates the stature of your brand, that exposes your organization to more people, that is the catalyst to subscribe or give for many.

We need great journalism

I’d argue that the same dynamic applies to advertising at many news organizations, even if they don’t realize it. They can’t compete with the price, reach and targeting of the digital ad tech that drives the biggest online platforms. But small newsrooms can make a hell of a case to local advertisers that they want to be adjacent to and associated with the kind of journalism that has the community appreciative and engaged.

This has happened in incredible (even Pulitzer Prize-winning) ways and it is exciting how quickly collaborative journalism has been embraced. But it’s never completely organic. This movement has happened in large part through the facilitation, research, training, convening and cheerleading of the Center for Cooperative Media at Montclair State University in New Jersey. Solutions Journalism Network has built training programs into its facilitation of regional and topical journalism collaboratives. And ProPublica, the Center for Investigative Reporting/Reveal, ICIJ and my alma mater, the Center for Public Integrity, helped show a new generation of investigative and single topic-focused nonprofits how having collaboration in your DNA allows you to punch far above your weight.

Meanwhile, Report for America is building training, mentorship and additional editing support into its process, to make sure that its ambitious goal of putting hundreds of additional reporters in under-resourced local newsrooms across the country has the intended impact. And the Investigative Editing Corps is pairing small newsrooms with experienced editors to provide support for enterprise and investigative reporting that goes beyond their typical daily news coverage.

Emphasis on essentials

Technology is also playing a part in making more advanced reporting possible in smaller newsrooms, from data journalism resources such as The Accountability Project and Big Local News to the document and records-access tools of Muck Rock.

When the Center for Public Integrity focused its mission four years ago on investigative reporting that confronts inequality in the U.S., we thought about how to scale that work beyond what our 25-person newsroom could do. When we obtained secret White House documents showing the true extent of the COVID-19 outbreak in 2020. We shared them directly with journalists across the country, and it saved lives. After spending thousands of hours obtaining and cleaning more than a decade’s worth of data about polling place locations and closures, we made it available to power not just our own reporting, but others’ work ranging from small local news organizations to NPR, the Wall Street Journal and the New York Times.

A lightbulb went off when we were publishing “Unhoused and Undercounted,” an investigation that proved public school districts across the country were failing to identify and serve homeless students as required by federal law. We realized that this story, using our data analysis, could be written in almost any local community in the country and have a high potential for very direct impact in helping kids.

We were offering the data and the formula of questions to ask. How could we get it — and similar investigations — into the hands of any/every willing local newsroom able to tackle it, in a way that allowed them to have impact with few resources but also an entry point to go far deeper into the topic in their community if they could?

Decentralized journalism calls for decentralized solutions for seeding and supporting the kind of work that will spark a virtuous cycle of revenue that rewards the most impactful journalism. Our media ecosystem is supported by a robust network of organizations that are focused on keeping newsrooms afloat. But like all things digital, even this support must continue to evolve. Revenue models are only as effective as audiences’ willingness to support journalism. It’s time to focus on empowering under-resourced newsrooms to deliver the highest caliber journalism, to support society – and to inspire audiences to support them.

About the author

Matt DeRienzo is a veteran newsroom leader whose work over the past four years as editor in chief of the Center for Public Integrity was recognized with a national Edward R. Murrow Award for general excellence. Previously, he served as vice president of news for Hearst’s Connecticut newspapers and as the first full-time executive director of LION, a national nonprofit supporting local independent online news organizations. He can be reached at [email protected].

Subscriptions are far and away the most consistent source of revenue for newspapers. However, to grow their subscriber numbers, sometimes they need to throw away consistency in favor of a more experimental approach.

The Independent has been a digital-only title for six years, having sloughed off its loss-inducing paper edition in 2016. While it has been solidly profitable for those years, its revenue has largely been generated through digital advertising; the same sort of business model that led to mass layoffs and bankruptcy at BuzzFeed and Vice respectively.

To head off problems with digital advertising, the Independent has made it a priority to diversify its revenue. While ecommerce and video advertising are core, its chair John Paton told me it sees a way clear to multiplying its direct reader revenue by five within three years.

To do that, he states the Independent is pursuing an “unknown to known” approach to its audience. Like many digital publications, it asks audiences to register to read. This provides the publication with data that can be used to track their propensity to ultimately pay for editorial content, among other things.

He said direct revenue is “now going to be a fast-growing. Part of that based on the back of the fact we’ve got these registered users who want to talk to us, and our marketing towards that as well. This improved our pitch and led to revenue of about 2 million. That’s going to be a big number like 10 million in two [or] three years.”

The process of turning a user from an anonymous, fly-by-night stranger to a potential customer is vital because every user’s likelihood of signing up for a subscription is wholly unique. The more data a newspaper has on its users the better its chances of converting them.

At the same time, many general-interest newspapers eschew that approach in favor of a one-size-fits-all hard paywall, sacrificing flexibility for clarity. So which approach, then, works best for different types of media brands?

Flexi and freemium

For many titles, flexible paywalls grew out of a freemium model. Austria’s Kleine Zeitung, for example, offers the traditional freemium model with a number of articles available to read before the paywall prompt appears. Other titles can also manually drop the paywall for certain premium articles, the better to entice people to pay.

In this model, eventually, inevitably, the paywall slams down. This is often paired with messages asking for support for independent journalism, or for registration to continue reading. This multi-pronged approach is vital, as research has demonstrated that the single-approach strategy of demanding payments rarely works.

Ultimately, however, these are largely blanket strategies, decisions made manually by human editors based on analytics and gut instinct. It is a beneficial approach both in terms of cost and messaging, as it reinforces the idea that the journalism behind the paywall is universally valuable.

Over the past few years, though, things have shifted. More personalized approaches have come to the fore, powered by AI and machine learning.

Tech and touchpoints

Analyst and founder of A Media Operator Jacob Donnelly explains that audience ID tech is making personalization of paywalls appealing to newspapers after years of scale-based priorities: “You have to start every conversation with the who, and really be clear about who the audience is, so that you can get everything else right.”

It’s a view echoed by Tim Rowell, general manager APAC for Piano, a paywall tech provider. He says that tools to model propensity to pay have been high up publishers’ agenda for years: “The reality is that, for most newspapers, these data are in disparate systems and the challenge is how to to turn all these data points into insight that can be acted upon. Those that can have built models to identify propensity to pay”.

One of the tech advances has been early deployment of proprietary AI tools. Swiss newspaper NZZ, for example, uses AI to personalize its paywall based around individual users’ propensity to pay.

Its managing director Stephen Neubauer explains: “We’re using machine learning today to derive dynamic segments, and to identify these patterns of preference” as a result of which the paywall can be rigidly enforced or relaxed on a per-person basis, the better to entice that reader to pay.

NZZ, however, is one of the most successful digital newspapers out there. As such it is well-positioned in terms of resources to develop and experiment with that AI tool. For many regional and local news groups that time and spend is beyond them, even as the cost of the tech falls. It is far from a foolproof system, as explained by the New York Times’ own applied/data scientist Rohit Supekar – but it is powerful provided you have the resources to do it.

Experimentation and confusion

But to what extent can newspapers try new things with paywalls without confusing their readership – or more likely causing them to wait for a better deal or free access during trial periods?

The same technology and techniques that allow for personalized paywalls is ameliorating that issue. For one thing a vanishingly small number of readers are likely to compare their own paywall offering with others, preventing confusion at a macro level. At the individual level, the ability to tailor messaging also helps users to understand that they are being served deals based on their usage habits rather than some arbitrary decision.

Rowell says: “It’s theoretically possible that audiences get confused by experiments. But the experiments would have to be pretty extreme to do that. We’d argue that it is a fallacy. Sound experiments based on insight and data and designed to improve conversion rates are likely to involve offers that are attractive to the audience”.

Despite all the advances in tech and strategy that allows papers to entice readers down an ever-shifting, personalized funnel, there is still one fundamental issue: a sizeable proportion of people say they will never pay.

According to the latest Digital News Report, 65% of UK news consumers said nothing could encourage them to pay – compared to 49% in the US, both higher than the 42% average across the 20 surveyed markets where paywalls are in effect. That is primarily ascribed to a lack of perceived value in the news products. And if audiences never seek out your site, the opportunity of going from unknown to known to paying subscriber vanishes.

In an increasingly crowded and competitive landscape, media companies are constantly seeking new strategies to increase revenue and customer loyalty. Bundling can play an integral part in achieving these goals. By combining multiple products or services into a compelling package, bundling can unlock new subscribers and revenue streams, as well as help reduce churn.

According to Meredith Kopit Levien, Chief Executive Officer of The New York Times Company, bundle subscribers pay more over time and are less likely to cancel. As a result, bundling can support strategies for customer acquisition and retention. Subsequently, it’s currently an area of growing strategic focus for many media companies.

Here are seven features that can strengthen your bundling strategy:

1. Make it financially compelling

You may not realize it, but you’re probably already bundling.Many publishers offer products, such as combined print/digital subscriptions, at a discounted price. These are often attractive to audiences due to minimal price differentiation, and dual access can improve their experience of your product(s).

For publishers, this also opens opportunities to sell advertising across both mediums. This can be especially valuable given the importance of print advertising, and the premium it can demand compared to digital.

The Seattle Times demonstrates this principle by offering a Digital +SundayDelivery subscription for the same price ($4.99 a month) as their digital-only package. Bundling in the Sunday print edition, complete with home delivery at no extra cost, is potentially very persuasive for readers.

Alongside appealing pricing, a further tactic media companies can deploy involves highlighting the benefits each subscription tier – or bundle – offers you.

In doing this, publishers typically point to subscriber-only content such as articles, newsletters, podcasts and events, or access to their archives. In many cases, this content is not available outside the requisite subscription bundle. And that’s a benefit that publishers are keen to emphasize.

Interestingly, the New York Times also utilizes a different approach, by stressing what you don’t have access to. This is most explicit for those accessing their news-only package (see below). The FOMO here is potentially very real, making an upgrade to “All Access” seem like good value.

It’s hard to say exactly what role this tactic plays in their continued subscriber growth. However, the company added one million new subscribers in 2022. Commenting on this, CEO Meredith Kopit Levien observes that “with each passing quarter, we saw more proof that there is strong demand for a bundle of our news and lifestyle products, hitting records on both total bundle volume and the share of new subscribers choosing the bundle.”

3. Prioritize building your stack

The cost of living crisis means that many people have less money in their pockets. To offset this, households are looking carefully at their expenditure and cutting back where they can. CNBC reports that Americans are more likely to cut back on groceries and gas than subscriptions. But this headline overlooks how low down the subscription food chain non-streaming content is.

Given publishers’ emphasis on reader revenue and subscriptions, this belt-tightening brings with it a certain vulnerability. To offset this, it is incumbent on media players to ensure that their offering is one consumers feel they cannot afford to cancel.

To help them do this, Greg Piechota, Researcher-in-Residence at INMA, suggests three ways media companies can add value to their bundle: build, buy or borrow.

Using The New York Times as a case study, he charts how the Gray Lady built Games and Cooking; bought The Athletic in 2022 (it costs $7.99 a month to subscribe to independently) and borrowed products in the form of a 2017 link-up with Spotify whereby new All Access subscribers also got Spotify Premium for a year. Bundling in Spotify for free (mirroring a similar initiative by The Times of London in 2014) arguably made their core subscription offerings more attractive to younger audiences. That means it may attract a new demographic of paying subscribers.

4. Flaunt your assets

Alongside the approaches outlined by Piechota, we should also add peacocking. Media companies with deep portfolios can prominently display this to potential suitors (i.e. subscribers) by creating bundles that tap into the sheer breadth of content at their disposal.

We have already seen this in the form of the Disney Bundle, which includes Disney+, Hulu, and ESPN+. These three content-rich services are considerably cheaper when purchased collectively. The “trio” bundle also comes with ad and ad-free versions too, another model that more publishers can emulate. (NB: ESPN+ comes with ads regardless of the package.)

In Europe, Scandinavian media giant Schibstedhas also put this notion into practice. They launched “Full Tilgang” in Fall 2022, a bundle of their Norwegian titles including national, regional and finance news, alongside magazines and their podcast platform PodMe.

For national subscribers, this regional and local content is a potentially useful value-add that they might not otherwise have consumed. It’s a model other companies might look to replicate. twipe reports that Schibsted is rolling out a similar model in Sweden.

Of course, not every outlet has the deep pockets – or the smorgasbord of content – enjoyed by The New York Times, Disney or Schibsted. Nevertheless, many outlets can deepen their bundles via partnerships.

These can come in a myriad of different forms. Digiday has outlined how partnerships with non-publisher brands – such as financial and educational institutions – are being employed by The Wall Street Journal and The Washington Post. Business Insider has also followed suit. In 2020 they offered holders of certain American Express cards a free 12-month subscription.

Tie-ins with other business and tech providers can also be seen. Major League Baseball has a long-standing partnership with T-Mobile, providing free subscriptions to MLB.TV (worth $149.99 a year) to T-Mobile subscribers. And in 2014, The Sun, a British tabloid, struck a deal with the UK mobile operator O2 to offer 02’s 4G customers content from soccer’s Premier League that gives them a glimpse of The Sun’s content which, in turn, might encourage some users to become subscribers.

It’s common for publishers to offer bundles with other titles in their stable. The Wall Street Journal offers a package featuring its Dow Jones stablemates Barron’s and MarketWatch. More interesting perhaps are partnerships with other content providers.

In the past, I’ve seen smaller outlets – like my local NPR affiliate KLCC –offer a free subscription to larger publications (like NYT and WaPo) as part of their membership model. For smaller players, this association may bring some extra cachet, or provide an additional incentive to nudge people over the line by taking out a membership or donating.

Even bigger players can successfully adopt this approach. The Weather Channel is a seldom talked about subscription behemoth, with over 1 million subscribers. It recently partnered with several organizations to offer bundles providing “companion subscriptions.” This trend may only become more prominent.

Looking ahead – where bundling might go from here?

And what of that future? Given the need for media companies to attract new audiences, as well as retain subscribers and maximize income from them, bundling will remain integral to reader revenue strategies. Here are two further ideas worth considering.

1. Explore different pricing models

In 2019, the advent of dynamic paywalls prompted Piano CEO Trevor Kaufman to ask, “Has AI brought an end to the metered paywall?”. New York Media and Neue Zürcher Zeitung (NZZ, Switzerland) are some of the outlets that have used this model, harnessing variables – such as your location, device type and browsing history – to determine when users hit the paywall.

Taking this to the next level, The Atlantic recently started using this technology to shape the price of their bundles. Dynamic pricing can be used when signing people up and for retention. For the latter, prices for renewal are determined based on the probability of a subscriber’s subscription lapsing.

“It is a concept worth exploring,” suggests Subscription Insider, although they stress the “biggest risk is how consumers will feel if or when they find out about it.” How will consumers feel if they get different prices to sign-up (or stay), each time they click on the site?

At present, audiences are at the mercy of bundles offered to them by publishers. But what if it were possible to build your own bundle?

Let’s say I just want the newsletters and audio provided by The Economist? Or I want to bundle The New York Times’ Cooking and Games subscriptions, getting them for less than two individual subscriptions?

Similarly, if I have a $25 a year standalone subscription to Politics with Charles P. Pierce on Esquire, what If I could cherry-pick additional elements to bolt onto my politics subscription?

I cannot do that at present, and this type of choose-your-own-adventure model might be technically tricky. However, personalization could enable me to subscribe to content by topic, writer, location, beat, or sports team that matters to me.

Of course, it may risk cannibalizing the take-up of other more expensive bundles. However, it might also hold strong consumer appeal, especially those for whom existing packaged offers are not compelling enough.

Moving forward, bundling is here to stay, supporting subscription strategies by playing a role in consumer attraction and retention.

Fundamental to this is making your bundle attractive and distinctive from your competitors. Subsequently, adding value to the bundle may well shape acquisition strategies, be that for talent (and the newsletters and podcasts they may front) as well as other properties.

At the same time, consumers need to be attracted by price and value proposition, this includes access to content and services they may not currently consume, but might if it’s bundled in.

The use of free trials, as well as partnerships with other media companies and brands, can be a way to get a customer’s foot in the door. Meanwhile, dynamic pricing and opportunities for personalization could become key tools to keep them there.

By bundling multiple products or services together, publishers and media companies can offer greater value to customers and increase subscriptions. There’s no hard and fast way to do this, but these seven steps demonstrate how all publishers can potentially use bundling to drive revenues and improve customer loyalty.

The news media plays a crucial role in supporting a healthy democracy. Newsrooms are to provide accurate information and holding powerful interests accountable for their action. However, new research shows that most Americans now think news organizations prioritize their business needs over public service. The research highlights a central contradiction of the U.S. news media: It is an institution with critical public duties within a system of little public funding.

The Gallup/Knight Foundation report shows that approximately 76% of U.S. consumers strongly or somewhat agree that most news organizations are “first and foremost businesses, motivated by financial interests.” Only 12% of consumers strongly or somewhat agree that most news organizations are “first and foremost civic institutions, motivated by the public interest.”

This report is Part 1 of a two-part study, American Views 2022. The first part focuses on consumer attitudes and behaviors, and the second will delve into what drives Americans’ trust in news. The analysis includes survey results from over 5,500 U.S adults aged 18 and older.

Nearly two-thirds (62%) of U.S. adults report that news companies lean more toward staying in business than serving consumers. Younger Americans, 67% of Gen Z and 70% of Millennials, are most likely to believe news organizations prioritize their business needs. Only a small percentage (6%) of consumers think news organizations lean toward providing a public service. Importantly, 30% of those surveyed think news organizations balance business needs and public service well.

Further, more republicans (81%) and Independents (82%) than Democrats (69%) strongly or somewhat agree that news organizations are motivated by financial interests than serving the public interest.

The Gallup/Knight analysis shows that the 29% of consumers “very favorable” toward the news media also say news organizations are first and foremost civic institutions. More than double the amount compared to the total consumers at 12%.

According to the Gallop/Knight analysis, almost three-quarters (72%) of Americans report never paying a news organization directly for their content. Among the 26% paying for news content, the majority did so via subscriptions (86%), donations (39%), membership (36%), micropayment (10%), and day pass (5%).

Those more likely to pay for news include:

Younger Americans (Gen Z and Gen X)

Democrats are more likely than republicans and independents

White Americans

College educated (four years)

High income, more than $150,000

Predictably, those with more favorable attitudes toward news media are willing to pay to access news in the future. One-third of consumers (33%) with favorable attitudes about the news media report having paid for news in some form. Further, 25% of consumers with favorable attitudes about the news media would pay to access news in the future.

Seventy-six percent report their decisions to pay for news depend on the content, and 62% say that the deciding factor is the cost. Gen Z and Millennials are considerably more likely to report that content is an essential decision factor, 82% each.

As new organizations look at new revenue streams, they should carefully target Gen Z and Millennials. We know Gen Z and Millennials index higher on willingness to pay for content. However, they also show a stronger inclination towards paying for events and exclusive content.

Striking a balance between servicing the public and managing a news organization’s financial interests is tied to consumers’ willingness to pay for news content. Ensuring this balance can help drive consumer favorability and grow their willingness to pay for content. Further, younger adults appear more open to diversified revenue streams, such as news organizations charging for events, newsletters, and exclusive content. As younger generations continue to gain buying power, these attitudes could translate into real financial growth opportunities for news outlets.

Reader revenue models raise concerns about subscriptions serving only wealthy and highly educated audiences. According to a Reuters Institute’s survey, almost half of news leaders (47%) are concerned that subscription models may “super-serve” more affluent and more educated audiences

A recent article by Laura Oliver identifies news publishers in Sweden, Spain, and South Africa that are creating inclusive offerings to ensure trusted news sources aren’t just available to those who can pay for them. Oliver offers examples of how publishers are paying it forward to readers who may not otherwise be able to afford a subscription. This allows them to access the news at a reduced cost (or even for free), while building good will and paving the way for a long term subscriber relationship.

Daily Maverick in South Africa provides a “pay what you can” model, while Spain’s elDiario.es allows members to pay nothing. Portugal’s Publico offers digital subscriptions to the unemployed, and Sweden’s Dagens Nyheter uses a flex paywall to attract younger and more geographically diverse audiences. Importantly, these publishers are focused on inclusivity and are setting the stage for others to follow.

South Africa’s Daily Maverick’s sliding scale

South Africa’s Daily Maverick offers a sliding scale payment for subscriptions. Readers decide how much to contribute, with prices ranging from just under $5 to just under $23 a month. There is also an annual subscription option from just under $50 to just under $230. Subscribers paying more than approximately $12 a month received the same amount in an Uber voucher as a perk.

The sliding scale attracted 24,500 Maverick Insiders, with a slight majority paying more than $12 a month. Additional benefits include ad-free browsing and invites to speak with journalists. Unfortunately, Daily Maverick Retention is somewhat problematic given credit card expirations and no auto-renewal process. Even with these obstacles, there are 17,100 active members. The Daily Maverick is looking into direct debit cards for less friction in the renewal process.

Sweeden’s Dagens Nyheter targets younger audiences

Dagens Nyheter introduced digital subscriptions in 2015 and expanded its offerings a year later. They employ a metered model, a premium model, and a dynamic model where most articles are free immediately after publication but then move behind the paywall. Approximately 60,000 people signed up for the free offer, and close to 30% converted into paying subscribers in the following year.

They used this strategy again during the COVID-19 pandemic, which resulted in 300,000 free registrations, with 25% converting into paying subscribers later. Dagens Nyheter subscribers started with approximately 2,000 digital-only subscribers. Now it has about 250,000 and reader revenues account for 78% of their total revenue.

elDiario.es reduced-fee options

Spanish news site elDiario.es believes developing an emotional relationship with audiences will grow its membership. Their offer allows members to pay from $8.50 to $80 or more a month for a subscription. They also offer a free or reduced-fee option for those who cannot pay. The site uses a metered paywall technology to help encourage loyal audiences to become supporters.

Nearly 21,700 members signed up for elDiario.esunder the free option. The site has almost 61,000 paying members, including 3,600 paying a reduced fee. In the elDiario.es revenue model, 50% of revenue comes from readers and 50% from advertising.

Pricing options allow readers with financial limitations to identify how best they can support newsrooms. Publishers willing to experiment with different pricing offers such as “paying what you can” show readers they are more human and less transactional. These efforts help them form a loyal and lasting relationship with audiences, regardless of their financial circumstances.

A mid-sized digital media outlet dropping its paywall is not usually the stuff of national news. But when Quartz, the digital business outlet, scrapped its paywall earlier this month, the move was promptly written up in the New York Times. What gives?

The degree of attention paid to Quartz’s decision has something to do with the media environment of the moment. As we’ve written aboutmore than once, digital subscriptions are on the rise across the industry, boosting profits for everyone from the New York Times to local papers in Buffalo and St. Louis.

Still, while subscriptions are generally trending upwards, nothing in the media industry stays static. In fact, just a few weeks later, Quartz announced it had been acquired by G/O Media, whose suite of sites is unpaywalled. It’s possible Quartz was just getting in line with its soon-to-be owner. It’s also possible that it is suggestive of a trend. Either way, it might be worth it to take a step back, assess your current paywall policy, and explore other methods of expanding your revenue strategy.

The power of community

In recent years, the rise in paywalls has grown in tandem with another trend: a renewed interest in community on the part of publishers.

The focus makes sense. Even the biggest publishers—outlets that receive tens of millions of visits per day—see only a fraction of the traffic of the big social platforms. On the internet, it seems, there’s no bigger draw than conversation. Give people a place to be heard, to connect with like-minded individuals, and they will repay you with regular visits: this is one of the main lessons of Web 2.0. It’s no surprise that publishers would want to siphon some of that energy for themselves.

For publishers looking to beef up their owned communities, a fully-paywalled site can be a complex proposition.

On the one hand, people who actually pay for a subscription are some of the likeliest to comment anyway. A thriving community can absolutely be built exclusively with paid subscribers. Substack’s a great example of this. Many Substackers only let you comment if you subscribe, and nonetheless host sprawling, engaged comments sections. There is also the fact that only letting paid-up members comment almost guarantees a more civil discourse, as it’s unlikely that a troll would actually pay money to annoy people.

On the other hand, comments are an incredible tool for growth—and paywalling all your articles can negate that function.

There is no question that it’s your content that matters most when cultivating readers. But as mentioned: online, community that creates stickiness. Community keeps readers reliably coming back, day after day. Un-paywalled articles allow first-time or occasional visitors to shake up the conversation, keeping things fresh and luring in still more readers (and participants). This can still be possible with a paywall—some percentage of readers, after all, will opt for a free trial and find the conversation that way—but the process might be slower, the growth less explosive.

To paywall or not to paywall?

Obviously, few sites deploy a paywall for every article (though some do—such as The Washington Post). Most, instead, paywall some content and open other content to anyone who wants to read it. Countless strategic concerns go into the decision of what to paywall. What we’d argue—given the importance of community for growth—is that one of those concerns should be: How likely is this article to generate conversation?

This consideration doesn’t have to be incompatible with a normal paywall strategy. In a normal paywall strategy, the articles that are paywalled are those most likely to drive clicks—juicy scoops or exposes, say, or epic longform features. But the articles most likely to generate clicks are not necessarily the ones that will generate the most conversation. They can be, absolutely. However, the truth is that evergreen, lower-stakes content is just as if not more likely to generate vibrant discussion.

Think, say, a list of the best albums of 1999. Or a quick primer on the best way to cook a steak. Or a write-up of last night’s big prestige-TV finale. Content like that can generate discussion at a surprisingly high volume. It draws in new readers and, in the slightly longer run, subscribers.

All of that said—and despite the Quartz move—there is no real indication that paywalls are on the way out. The beauty of this moment in media is that publishers don’t have to choose. They can grow their audience with paywalls while they can grow their audience with community (and with social media, live events, ecommerce, etc. The options right now are endless, as discussed in our recent guide).

What an engaged community can offer, more immediately than many other revenue concepts, is engagement. Higher engagement means more pageviews and––when leveraged to sell subscriptions or place ads––stronger, more diversified revenue for publishers.

Once seemingly unstoppable, subscription-based digital media services like Netflix now look vulnerable. Netflix reported seeing a drop in subscribers for the first time in 10 years, prompting a recent selloff that shaved more than $50 billion off the company’s market cap. Other streaming services, from Disney to Roku, also reported similar drops. Many worry that we’re witnessing a phenomenon known as “peak subscription,” where consumers facing an increasingly uncertain global economy are growing weary of committing to a laundry list of ongoing subscriptions.

Some publishers have felt the repercussions of peak subscriptions and competition from free alternatives. Quartz reported that some readers subscribe just to read one specific article and then quickly unsubscribe afterward; behavior that hindered real growth. Although metered paywalls have proven effective at driving subscriptions for many publishers, some believe it is a “blunt-force instrument” that won’t work for everyone.

Even as the total number of subscriptions is still high across publishers and creators, there are concerns that the supply of content sources outstrips demand, particularly when we consider more commoditized content. Despite the fact that the global subscription economy is projected to grow by $51 billion dollars in 2022, competition is fierce – even for the likes of Netflix.

As subscription fatigue becomes a growing concern, and competition among subscription-based content of all kinds continues to intensify, media companies seek ways to go beyond pure subscriptions and increase their revenue. The good news is that various solutions already exist.

Redefining the journey to becoming a subscriber

One of the key solutions to combat subscription fatigue is to let audiences become paying readers and members at their own pace. Instead of asking people to lock themselves into a subscription model off the bat, some companies monetize the subscriber journey in smaller steps.

To move away from relying solely on the one-size-fits-all subscription model, streaming services like Disney+ have opted to offer a lower-cost version of their service that includes ads. The potential rewards of this move are clear: Disney’s own Hulu streaming service has turned commercials into a $1 billion revenue stream. Comcast’s Peacock and AT&T’s HBO Max now both come with ad-supported and ad-free versions. Even Netflix, which stood clearly opposed to integrating ads in the past, will now launch an ad-supported version sometime in the future.

Publishers such as Vox and The Guardian have also moved to a membership model, believing that readers will want to voluntarily support their publication even without the added pressure of a paywall.

Quartz also offers a subscriber-only newsletter that gives paying members exclusive access to additional content and various other benefits. However, it has made content on its main site free to access. Vice News has opted for an even more reader-friendly approach by adding a “tip jar” to its website, in case readers want to voluntarily make a contribution to the publisher.

The demand for incremental revenue streams to reach readers averse to committing to a subscription is why à-la-carte payment solutions emerged for publishers and content creators. These solutions allow users to buy paywalled text, audio, or video content with one-off payments or make voluntary contributions for open content.

Publications understand that having multiple monetization solutions builds engagement from different audience segments. This also feeds the subscription funnel with loyal users. Instead of asking casual visitors to commit to a subscription with discount offers, they are given the chance to engage in incremental steps.

The new era of reader revenue

The shift from relying solely on subscriptions signifies a clear acknowledgment of the need to give consumers flexibility and freedom. For audiences, this is a sure boost to their overall experience.

Digital publishers and content creators will benefit as well. Overall, a growing number of people are willing to pay for content. According to the 2021 Digital News Report from Reuters, 17% of people surveyed stated they were ready to pay for media content — a definite increase from the previous year.

Offering multiple reader-revenue solutions like exclusive memberships, micro-bundles, ad-supported bundles, à-la-carte payments, and even a tip jar makes it easier for publishers and content creators to monetize different audiences segments and capture rich first-party data. Alienating large swaths of audiences with an all-you-can-eat subscription offer will no longer suffice in a world where users are spoiled with choices.

It is also imperative to understand users’ willingness to pay for different types of content. For example, the exact same content bundle might be worth $10 per month to half of your audience and worth $5 per month to the other half. The one-size approach is to offer a $7.50 bundle to everyone. However, the maximum revenue approach entails creating two separate bundles for each of the audience segments. Unbundling content to understand user willingness to pay for each type of content can actually pave the way for publishers to resurrect the appropriately priced recurring payments.

If you’re a subscription-based digital publisher, the message is clear: the time to look for incremental ways to monetize and engage with a wider audience — including the elusive “never subscribers” — is now. Learning from the examples set by the companies above will save you from wasting time forcing one, rigid monetization strategy on an audience that doesn’t want it.

About the author

Dushyant is a Co-Founder & Chief Commercial Officer at Fewcents, a plug-and-play solution that helps digital publishers and creators monetize content with cross-border micropayments in the form of pay-per-content or tips. He spent 13 years at Google where he led strategic partnerships, working closely with some of the biggest digital publishers in Asia. Prior to Google, Dushyant has worked at SAP Ariba, American Express, and two tech startups. He holds an MBA from the ISB, Hyderabad and is an active angel investor & advisor for startups in Southeast Asia.

Lately, there has been much investor handwringing over CTV investments. With Netflix’s latest results, some worry that if Netflix’s growth has stalled, the prospects for everyone else may be diminished as well. This is why the same day that Netflix stock came down 35+%, there were also (albeit much smaller) declines in other broadcast stocks too.

But the concerns may be misplaced. If YouTube can build a $28.8B annual revenue advertising business, without subscriptions, surely there’s hope that Netflix and other media brands with strong content catalogs can build and sustain ad-supported offerings.

The YouTube business

To better understand the YouTube business, MediaRadar took a look at the mix of YouTube’s current advertising. For this analysis we reviewed pre-roll, mid-roll and post-roll ads from the largest 3,000 YouTube channels across 33 content categories through a panel of over 2 million users.

What we found was a robust, growing business, with significant lift in advertising revenue the trailing year, but also the number of advertisers, across most product categories, was up. Alphabet Inc, which owns YouTube, recently released FY 2021 numbers. The economics look strong. The company grew revenue 47% in 2021, up to $28.8B. Almost all of this was from ad revenue, with very little from subscriptions. The implications for all broadcasters and publishers is meaningful.

Some view YouTube as a platform only, not as content creator. But this is not quite right. YouTube is a platform of course. But they also invest aggressively in their influencers and third-party content creators. While they don’t finance scripted shows, they don’t leave content creation to chance. They do this by providing physical space, the latest tech, upfront grants, and even assign a manager to advise creators once they hit a certain number of followers. As reported by the WSJ in October 2021 they note YouTube employs 1,000 full-time managers assigned to the top 12,000 creators. With this in mind, there are takeaways for others on how to build a hybrid approach to content creation.

YouTube advertising findings

The industry verticals with the most concentration of ad spend include entertainment, technology, retail, finance, and pharma. Altogether, these categories accounted for 60% of ad placement, and each segment increased > 30% YoY from 2020 to 2021.

Retail and ecommerce advertising are up significantly year-over-year. We observed an increase in ad spend within this category of 109% from 2020. Unlike in certain categories, in retail we continued to see steady growth throughout the year. The Retail Category increased advertising on YouTube by 60% in Q3 2021 and 91% during the Q4 2021 holiday rush.

YouTube’s music content was the most popular in both 2020 and 2021 with advertisers. YouTube benefits from strong renewal rates, but also from new clients. 52% of advertisers in music YouTube channels were new in 2021.

Everyone knows Travel advertising would be up. YouTube did not disappoint. Advertising investment in the Travel vertical grew by 270% YoY from 2020. Some of the ad spend was from kid-friendly vacation destinations and theme parks like Disney World and Discovery Cove. Ad spend increased 8x year-over-year.

Content is key to advertising growth

Next, we looked into YouTube’s programming channels to see what content categories are helping to drive growth of the platform. Interestingly, the most popular among advertisers were the same in 2020 as 2021 – music, kids, society and culture, and gaming.

YouTube’s music content was the most popular both years among advertisers. Furthermore, 52% of the companies investing among YouTube’s music content were newcomers to the category.

Another trend we uncovered was within “kids” content. Advertising investment among travel vertical grew by 270% YoY from 2020. Most of the ad spend was from kid friendly vacation destinations and theme parks like Disney World and Discovery Cove. Ad spend increased 8x among this group.

What’s next?

As we move through 2022 and into 2023, we expect retail ad spend to continue growing on YouTube. YouTube will continue to be a hot-spot for advertising among retail brands.

While ecommerce has had an increasing presence for years, the pandemic likely accelerated this possess by uncovering new technology to help making digital buying easy. YouTube has had success with shoppable experiences, and we expect to see more of them.

Publishers have long understood the value of affiliate revenue and shoppable content. The opportunity here – as demonstrated through YouTube’s success – is to evolve this into video and CTV offerings as well.

It will be interesting to see how the “new normal” plays out post-pandemic. Obviously, the industry and buying behavior has been forever changed. The online video market is also becoming cluttered with numerous CTV and OTT options. Even Disney+ and Netflix are launching advertising-based models. The constantly evolving market will impact the way video is consumed and the methods advertisers need to use to promote their products.

The combination of content and commerce is a strong one. And, as we are seeing throughout the streaming space, content drives audience interest. And audience interest drives ad sales success. YouTube’s success illustrates the opportunity for ad-supported streaming success.

As the subscriptions race has intensified, media companies are turning their attention to the substantial segments of their audience who aren’t willing — or financially able — to pay for a full subscription. Some are returning to the tried and true tactic of lower-cost ad-supported offerings, while others have doubled down on putting the plus in premium.

News brands have always run the gamut from super-premium to completely ad supported. And some have speculated that the trend of premium digital news offerings – with the notable success of The Washington Post, The New York Times, and Financial Times – bodes poorly for readers in search of quality and value. And the proliferation of low cost or free offerings can often overwhelm, and even under-inform when consumers actually avoid the news.

It’s possible that a new approach is emerging which may address these issues – and offers premium brands a way to expose a broader range of consumers to their content.

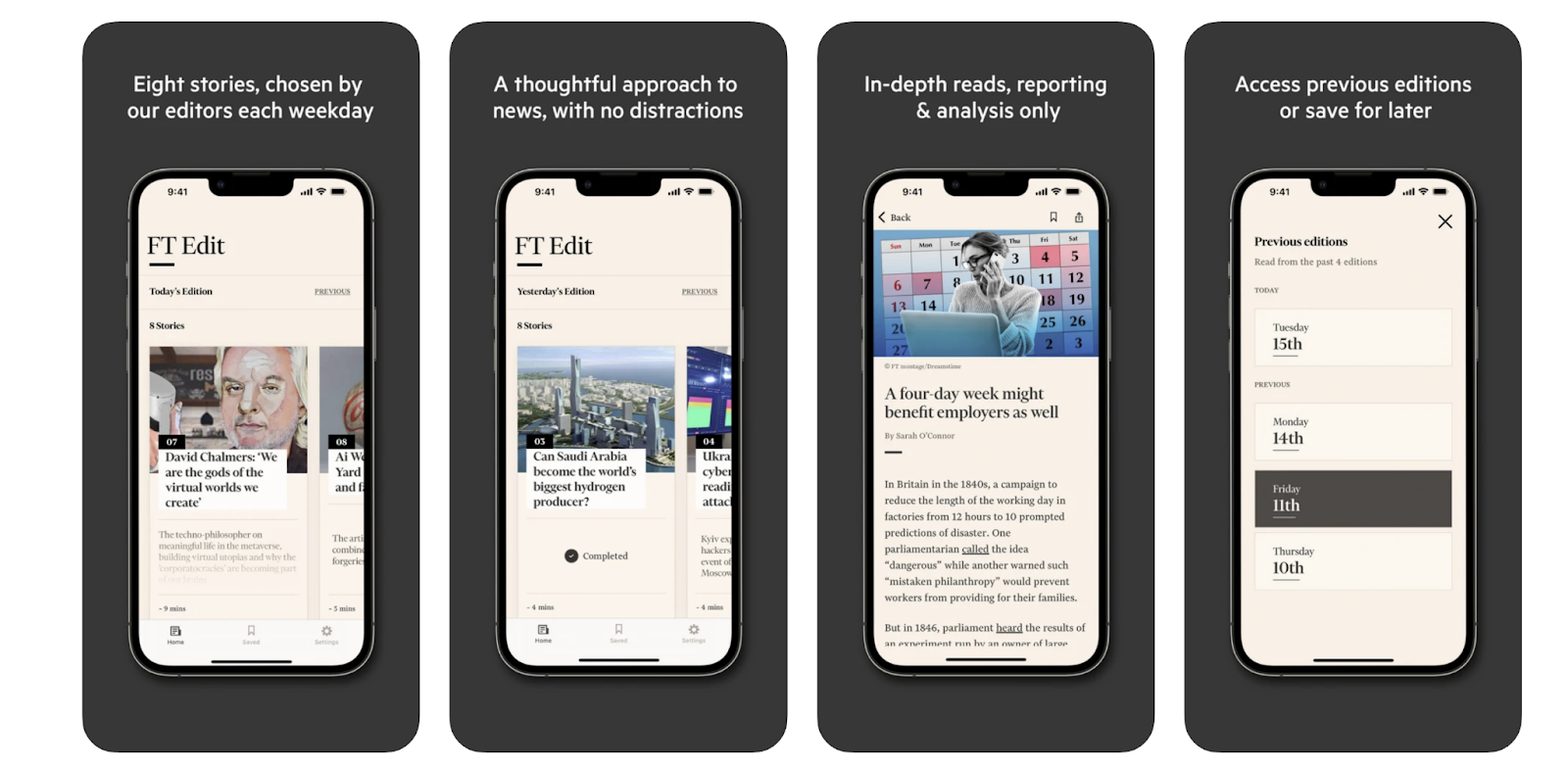

A financial case

Last month, Financial Times launched a new lightweight offering called FT Edit. The app offers readers eight hand-picked stories every weekday for just £0.99 per month.

Though it has amassed 1.2 million subscribers to date, FT has traditionally attracted a certain kind of subscriber due to the high-end financial news it covers. A typical subscriber is of a higher income, with an interest in or working for the financial sector. Its most affordable digital package, which ranges from $40-$69 a month (£35-£55) would be a stretch for those who don’t need specialist financial coverage. If a consumer is after more general news, plenty of other organizations have more affordable subscriptions.

But increasingly, FT is gaining a following outside of its financial journalism. Part of that appears to be the result of making certain facets of its broader scope publicly available. Its coronavirus coverage was the first to be made freely available in March 2020. It currently has a page dedicated to free-to-read coverage of the Ukraine war “to keep everyone informed as events unfold”.

“We are known for financial news, and we’re incredibly strong at our core product. But we produce a wide breadth of news that matters, and I don’t think people really know that about the FT,” Assistant Editor Janine Gibson explained. “We weren’t really sure whether people wanted to read our free stuff more than anyone else’s, but it was very, very, very successful.”

Creating a more affordable product

The team began to see that there was a much wider appetite for their journalism. The conversations started to turn towards what a much lower-cost product would look like for the publisher. Their research about what people wanted came back with a core message: a simple product with a start and end point. Something more reflective, analytical, and deeply reported – but also expertly curated.

“There’s a different thing happening in the world of quality journalism. People understand that paying for quality journalism is vital, but they don’t necessarily have the resources or the appetite for the full, unexpurgated experience,” Gibson said.

Within a matter of months, FT Edit was conceived. Not only is the price point low, the limited offering provides a concise and digestible solution to too much news. The company says “the purpose of FT Edit is to provide an alternative to endless scrolling, allowing readers time to digest eight important stories selected for them each day. It will launch with the strapline: time well read.”

An audience-centric approach

The concern for many publishers considering this option is cannibalization of the existing subscriber audience. But Gibson sees the audience for FT Edit as adjacent to their core subscribers, not competing.

“This app isn’t here to solve a problem for a news organization,” she explained. “So many digital product launches over the last decade have come from a position of weakness, like ‘We need to replace this revenue gap’. This is, is there a wider audience out there at a lower price point for the FT? But we don’t need to offset the cost of what we already do.”

“The price point really reflects the commitment from the board and the chief executive to genuinely saying, ‘I would like to expose a much wider audience of people to some FT journalism.’”

Now, the app will go through some tweaks to find out how many stories each day works best. It is early days, but should the app get a good response in the UK, Gibson said a dedicated US version with content curated for a US audience would follow.

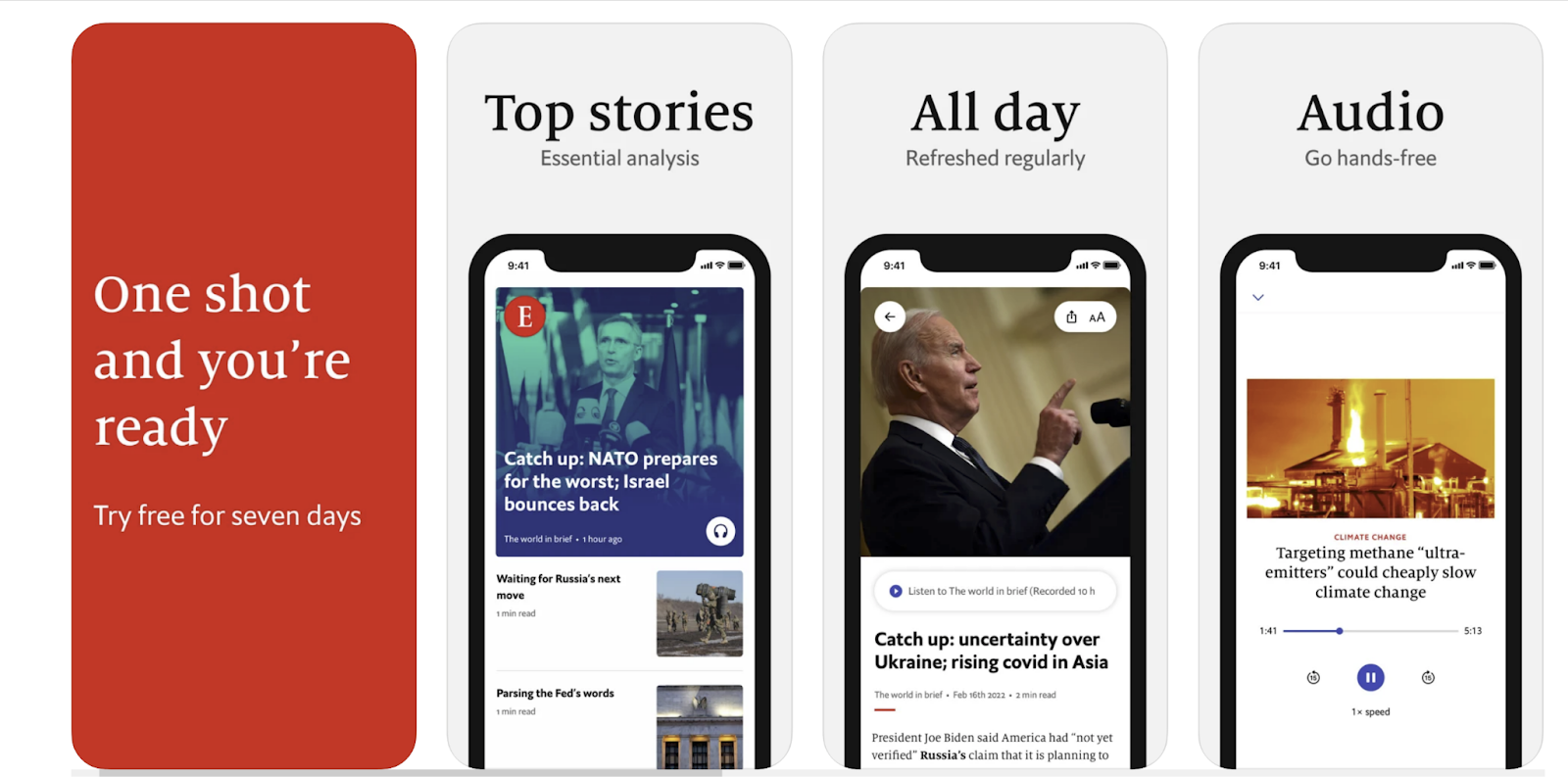

A bracing shot of news

FT is not the first publisher to experiment like this. The Economist’s Espresso app is the most well-known example of a separate, lower cost, lower quantity subscription offering. The recently updated app, launched eight years ago, was introduced as a daily digital briefing to complement the core magazine, with short pieces of news and analysis. It was marketed as a quick ‘shot’ of news to get readers ready for the day.

Espresso is included as part of The Economist’s full digital subscription. It is offered as a standalone app for $7.99 (£7.99) in the UK after a seven day free trial. Those who don’t choose to subscribe can still read one article a day.

The publisher has been working on an upgrade of the app over the past few months. The new version delivers Espresso stories in both written and audio form, alongside charts, facts and quotes each day. It also includes a ‘For You’ tab that lets the user sample four stories a week from the main Economist site, based on their interests.

“The new Espresso is aimed at readers who may not have the time or inclination for the more in-depth Economist experience,” a spokesperson told us. “We see it as introducing a new generation of readers to the Economist brand.”

“We imagine that, over time, some will migrate to an Economist subscription as they come to appreciate the role that our full journalism offerings can play in their lives.”

Is an app the perfect outreach product?

The question of affordable quality journalism is likely to become ever-more pressing as more publishers turn to reader revenue. From the Washington Post to Bloomberg – and even The Smith’s yet unlaunched Semafor – the market is saturated with publications targeting the global elite who barely blink at paying hundreds of dollars a year for news access.

The challenge for publishers looking to attract a wider audience to quality journalism is pricing for access. This is where paid products like apps or even newsletters can be a good way of building a relationship with readers without asking them to pay premium prices.

The longevity of Espresso and the initial success of FT Edit also demonstrate that audiences respond well to content with a start and a finish point. Aside from the obvious parallels to print newspapers, a carefully curated, high-quality set of stories is now seen as a refreshing antidote to the endless scrolling, misinformation, and frantic news cycle. In other words, for a tiny fraction of the cost, you get a tiny fraction of the news: just what you need to know, concisely offered and expertly crafted and delivered.

Now, limited is in demand. A small bundle of stories well-packaged for mobile could be the key for other publishers to unlocking their vast untapped audiences who haven’t yet opened their wallets.

It took The Boston Globe seven years to reach the first 100,000 subscribers. It only took a year to add the next 100,000. They’ve found that the key to accelerating growth is an introductory subscription offer so low, they’re practically giving the news away.

Head to bostonglobe.com and non-subscribers are given the option to read all the content they want for a bargain $1 for the first six months. While the Globe’s generous offer comes with an expiration date, a surprising number of subscribers decide that it’s worth paying more to stick around.

“We’re at the point where 90% of growth and revenue comes from subscriptions,” Tom Brown, vice president of consumer revenue for Boston Globe Media, said of the company’s digital operations.

How The Globe got here

With subscription growth slowing, The Boston Globe decided to try an experiment in 2018. The Globe, which has long believed its product was worth $1 a day, began charging that rate in 2015. It also decided it would try to accelerate subscriber growth with a bargain introductory offer.

In the first few days after making the one dollar introductory offer, Brown said they got thousands of new subscriptions “which was far higher than the 150 or so subscriptions that came in on a normal day.”

Beyond that, though, a higher number of those one dollar introductory offers converted into full-rate subscriptions. The Globe’s 2018 experiment alone led to a tenfold increase in subscriber conversions. “You’re stepping more people to the full rate every week than you ever would have with another other strategy,” Brown said.

“We felt good right away that we had not mortgaged our future in any way to do this test.” In fact, more than 80% of subscribers kept their subscriptions in the first month after prices reset. That fell over time but remained above 60% by the time a subscriber hit their three-month anniversary. And more than 30% of people continue to subscribe to bostonglobe.com after two years.

Attracting young audiences

There’s one almost surefire way to get a new customer to try a product — a discount so good it can’t be refused. That is especially true with younger audiences, which are accustomed to getting news from places like Instagram and TikTok.

“New and younger audiences were willing to give us a shot because it’s almost like a free trial,” Brown said. However, while a free trial might seem an obvious choice, research has found that charging any amount increases the odds audiences will convert from trial to subscriber at the end of the introductory period.

The paper also tried offering a four-week subscription for 99 cents but ultimately found the details of the offer didn’t make a meaningful difference in conversion rates. Audiences are required to enter a credit card to pay their $1 balance and are told their subscription will eventually renew at the weekly rate of $6.93.

Full funnel options

Brown notes that many younger subscribers didn’t grow up with a newspaper subscription so they were unaware of the breadth of the local paper’s offerings. “We’re a general interest news site that has so much and I’m not sure how much everyone knows all that we have,” he said.

Most visitors to bostonglobe.com get at least one free article. This classic move is designed to keep the top of the customer acquisition funnel open and signaling to Google and other platforms that audiences are engaging with the site.

Because an estimated 80% of Boston Globe readers don’t hit a paywall right away, readership – and ad views – don’t suffer because of a strategy aimed at driving long-term revenue growth, according to Brown.

Long-term customer value

It is wise to invest in the lifetime value of a customer. While an offer like this may take cash out of your pocket today, it offers the promise of exponential returns if audiences are happy with their experience.

“We’re making lots of decisions that we know may hurt or may not pay off this year, but will pay off over the long term,” Brown said. “The more subscribers you can acquire now, the better off you’ll be in the future.”

Nowadays, Brown and his team focus on making revenue-maximizing decisions without getting hung up on the small sacrifices it might take to get there. “This strategy is the right one for us,” he said. “The pandemic crystallized that in the sense that we became even more relevant to our readers as advertising became extremely volatile.” Being reader-supported makes the brand less vulnerable to the whims of advertisers.

And while the first few months after a price reset triggers some cancellations, those who stick around tend to be loyal customers. The volume of new subscribers can also make it easier to stomach the churn. “Our model is as tight as it’s ever been, and our audiences are larger,” Brown said.

The pandemic is just the latest thing to show subscription revenue can be much more dependable than ad revenue, Brown said. “It’s certainly not recession proof, but news is very relevant to people in times of crisis.”